Financial statement analysis is the process of scrutiny, evaluation, and interpretation of the financial statements of an organization. It involves building up a relationship between the various components of the financial statements. While all three financial statements are important and interconnected, the most commonly reviewed financial statement for assessing a company’s health would be the combination of the Income Statement and the Balance Sheet. The Income Statement provides information about a company’s profitability and performance, while the Balance Sheet gives a broader perspective on its financial position and stability. The Cash Flow Statement is also valuable in understanding a company’s cash generation and liquidity.

Analysts try to obtain a clear picture of the organization’s financial position and performance by doing a thorough financial statement analysis. The analysis is always done with respect to the industry and the economic environment in which the company is operating. It helps to identify a company’s strengths and weaknesses. This can be very useful to the company’s stakeholders, present and potential investors as well as the regulatory authorities. However, there are numerous other objectives of financial statement analysis that we will see further in this article.

Financial statement analysis helps to decipher the data that the companies report financially. It helps to understand the company’s earnings quality and capacity by understanding the earning trend and the future earning potential of the company. Analysts can identify and analyze the debt component, the repayment schedule, and the cash flow associated with it. Also, it throws light on the amount of interest expenditure required to service the debt. Moreover, financial statement analysis helps to understand the income and expenditure components, the dividend policy, and some other aspects that can impact the company’s financial standing and operations.

8 Vital Objectives of Financial Statement Analysis

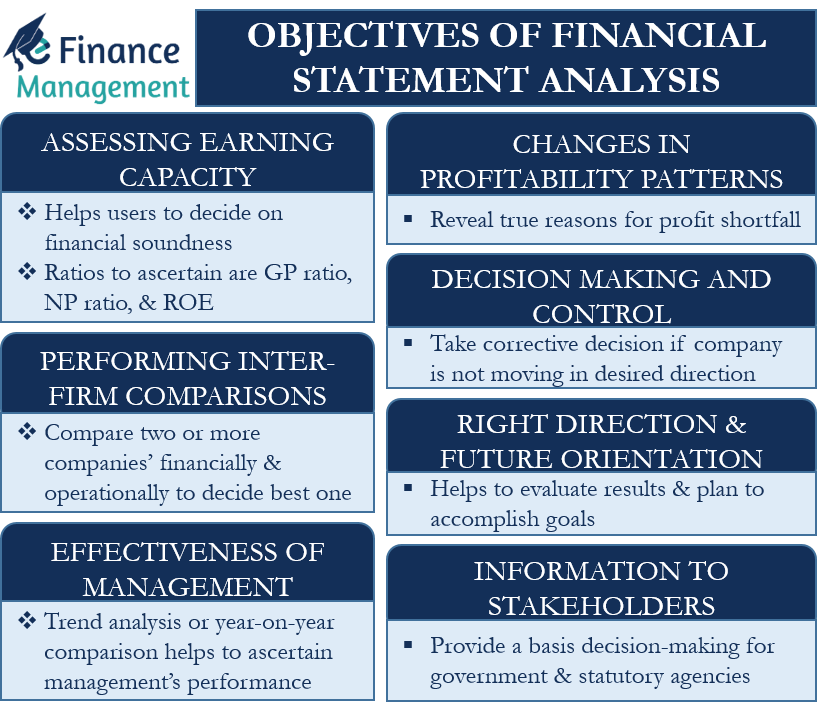

Assessing the Earning Capacity

One of the prime objectives of financial statement analysis is to assess the earning capacity of the company. This helps the users to decide on the financial soundness of the firm by doing a thorough evaluation of the financial reports on the basis of past performance. Moreover, it gives an insight into the performance capability and earning capacity in the future. There are several profitability ratios that help to ascertain the earning capacity of a company. Gross profit margin, operating profit margin, net profit margin, return on assets (ROA), and return on equity (ROE) are commonly considered as part of the profitability ratios.

Also Read: Importance of Ratio Analysis

Interested parties get assurance that the company can generate substantial earnings to cover its cost of capital, meet its working capital and other operational expenditures and still be able to generate profits. Profits are important for survival, growth, and for the assessment of opportunities for expansion.

Assessing Effectiveness of the Management

Financial statement analysis aims to give an insight into the effectiveness of the management. A trend analysis or year-on-year comparison of the results helps the analysts to ascertain how well or poorly the management has performed over the years. It throws light on the auditing policy and the effectiveness of the internal control placed in the organization. Also, an objective of financial statement analysis is to assess the operational efficiency of the company and its management.

Changes in Profitability Patterns

Financial statement analysis is extremely important in case the financial results of the company are below expectations and not up to the mark. An analysis will reveal the true reasons for the shortfall in profits. It might be due to the rise in input costs, unplanned capital expenditure, the occurrence of a natural disaster or a calamity, etc. Stakeholders and other interested parties should not jump to conclusions. Rather, they should carefully examine the analysis report and try to understand the correct reason behind the shortfall in performance before taking any important financial decisions.

Performing Inter-Firm Comparisons

Financial statement analysis aims to facilitate inter-firm comparisons. Analysts and stakeholders can compare two or more companies financially and operationally. Any company can give poor results in a few quarters. So, the analysis helps to assess the true reasons behind the underperformance and answers whether this is short-term or long-term. Also, a company can be highly leveraged and can give good results in comparison to peers but still have a high-interest expenditure component. The analysis aims to disclose such essential information and helps stakeholders to decide which one among them is the best fundamentally.

Decision-Making and Control

One of the key objectives of financial statement analysis is to help in decision-making and control. From the point of view of the management of a company, its financial statements are a sort of report card for its performance over a period of time. Analysis helps the management to make the right decisions for the better future of the company. They also help the management to take corrective decisions if the company is not moving in the desired direction. Also, a thorough analysis is pivotal at times for taking important decisions with regard to mergers and acquisitions.

Financial statement analysis helps identify a company’s strengths and weaknesses. By examining financial ratios, trends, and other key indicators, stakeholders can pinpoint areas where the company excels and areas that need improvement. This analysis can guide strategic decision-making, highlighting opportunities for growth and areas for operational or financial efficiency enhancement.

Information to Stakeholders

Financial statement analysis also aims to provide a basis for crucial decision-making on the part of the government and statutory agencies. For example, if a company’s financial statements indicate a significant increase in expenses or losses while reporting minimal revenues, it may raise concerns for tax authorities. They may decide to conduct a detailed examination of the company’s financial records, verify the legitimacy of expenses, and assess the accuracy of reported financial information.

The key decision areas that are affected by such analysis are licensing and controls, implementing price and profit ceilings, providing concessions and subsidies to the needy sectors, etc. The analysis also helps the banks and financial institutions to take the important decision of providing finance to a company or not.

Right Direction and Future Orientation

Financial statement analysis aims to provide a direction to any company and guide it on the right path to success. It makes use of multiple tools such as comparative statements, trend analysis, ratio analysis, and cash-flow analysis. These tools help the management to thoroughly evaluate the financial results and plan accordingly. The analysis is constantly evolving and dynamic in nature. It keeps reminding the management about any deviation from the direction they might have chosen for the company. This helps in accomplishing the goals of the company and assures its bright future.

Assess Investment Potential

Financial statement analysis is vital for assessing the investment potential of a company. It helps investors evaluate the company’s financial health, growth prospects, and overall performance. By analyzing financial statements, investors can make informed decisions regarding investing in the company’s stocks, bonds, or other securities.

Conclusion

The objectives of financial statement analysis are manifold. It aims to benefit the management as well as outsiders such as creditors, lenders, investors, labor unions, and financial analysts. The analysis helps in achieving excellence in managerial performance and corporate efficiency. Also, it sheds light on the solvency position and earnings potential of the company.

However, such analysis has several limitations as well. The basis for financial statement analysis is the financial statement itself. The statements are prone to window dressing by the management to present a rosy picture. Also, the statements fail to take into account inflation, price-change effects as well as non-monetary aspects that affect the performance of the company. Hence, there is a possibility that all the objectives of the financial statement analysis may not be met.