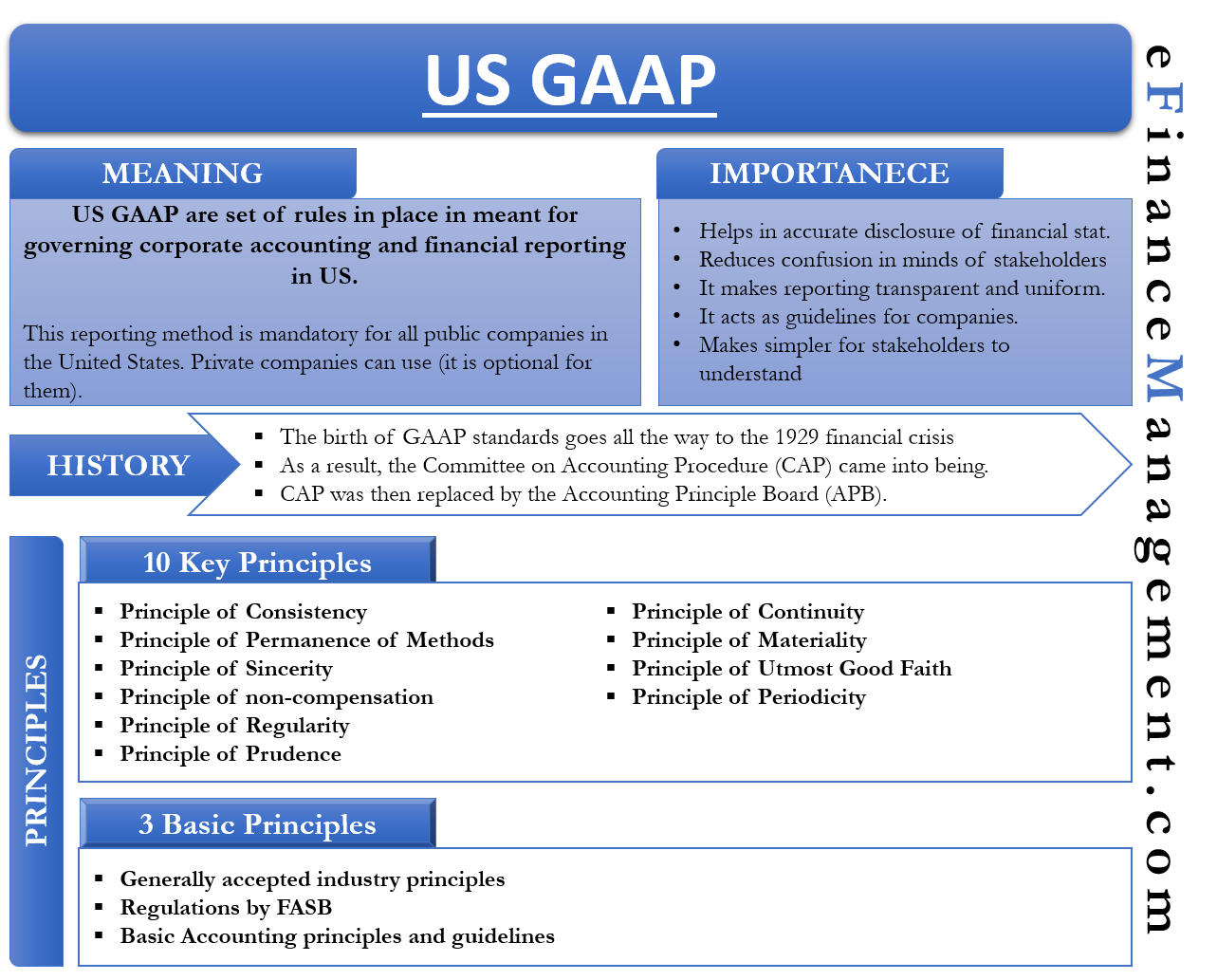

Generally Accepted Accounting Principles or GAAP is also known as US GAAP as it is in use in the US. These are the set of rules in place meant for governing corporate accounting and financial reporting in the United States. The Financial Accounting Standards Board (FASB) laid the foundation of GAAP by designing a comprehensive list of methods and practices that the companies operating in the US must follow.

The companies can also report their financial statements in other formats as per the information they want to disclose to the stakeholders. However, the GAAP way of reporting is mandatory for all public companies in the United States. As per the law, companies that trade on stock exchanges and indices must follow GAAP’s method of accounting.

How US GAAP was Born?

The birth of GAAP standards goes all the way to the 1929 financial crisis (Stock Market Crash and Great Depression). To restore public confidence, the United States government looked for ways to regulate the practices of public companies. The Securities and Exchange Commission (SEC) was given the authority to set accounting standards. SEC, in turn, delegated this responsibility to the private sector auditing company – the American Institute of Accountants.

As a result, the Committee on Accounting Procedure (CAP) came into being. After 20 years, CAP was replaced by the Accounting Principle Board (APB). The very motive of APB was to release the opinion on significant accounting topics that were later converted into law (if deemed fit) for the public companies by the SEC.

Also Read: Importance of GAAP

Who Follows GAAP?

The US GAAP applies throughout the fifty US states. If you are doing business in the US, or plan to do business in the US, or plan to get funds from American sources, then you should follow these standards.

All public companies must follow these standards. Private companies can use any method of their choice. However, since private companies also require loans and funds, it is advisable that they also follow such standards. Banks and other financial institutions have more trust in companies following GAAP.

Importance of US GAAP

Let us see the importance of US-GAAP:

Companies have various stakeholders, both in the form of people and organizations. Also, a major portion of the capital for public companies comes from equity shareholders. Therefore, it is the obligation of the companies to accurately disclose all financial transactions to these stakeholders since they hold ownership in the company.

However, the absence of standards and a uniform set of procedures might confuse the stakeholders. Further, it would open a lot of space for the companies to manipulate the numbers and misguide shareholders about their financial health. Thus, GAAP standards make financial reporting transparent and uniform.

Also Read: GAAP

Also, these guidelines make it easier for companies to report their financial numbers. And make it simpler for the shareholders to understand these financial numbers. Along with the shareholders, a uniform set of standards allow the rating companies, board members, and more parties to comprehend financial statements in a better way.

As per GAAP, Governmental and non-profit entities should also be more accountable and disclose their finances clearly and accurately. To sum up, Generally Accepted Accounting Principles ensure a uniform presentation across industries and let companies disclose all required financial information to the stakeholders without fail.

10 Key Principles of US GAAP

It lays down ten key principles that every public company should follow while releasing its financial statement. These are;

- Principle of Consistency – one of the most important aspects of GAAP is that all companies should follow a consistent standard while reporting.

- Principle of Permanence of Methods – this principle states that a company must use consistent procedures to prepare all financial reports.

- Principle of Sincerity – companies and accountants who follow US GAAP should have the utmost commitment to accuracy. Also, they must be unbiased towards reporting the numbers in the financial statement.

- Principle of non-compensation – a company should report the entire performance of the organization irrespective of whether it is positive or negative.

- Principle of Regularity – US GAAP – compliant accountants should follow the rules and regulations without fail.

- Principle of Prudence – US GAAP following companies should know that speculation does not affect the reporting of financial data.

- Principle of Continuity – while valuing the assets, an accountant should assume that the operations of the organization will continue.

- Principle of Materiality – financial reports should continuously disclose the monetary health of the organization.

- Principle of Utmost Good Faith – all companies and stakeholders are expected to act in good faith with no malicious intent.

- Principle of Periodicity – this standard says that the company must divide revenues by standard accounting time periods, such as fiscal quarters or fiscal years.

Basic Principles of GAAP

Apart from these ten principles, the foundation for the US GAAP rests on three rules that eliminate the use of misleading and deceptive accounting and financial reporting practices. These are;

Generally accepted industry principles – there is no universal GAAP model fit for all industries. Instead, there are industry-specific standards that different industries follow as per their reporting and disclosure requirements.

Regulations by FASB – FASB regularly updates and issues a set of principles known as FASB Accounting Standards Codification. These updates ensure that GAAP remains relevant with changing times.

Basic Accounting principles and guidelines – this rule covers the above ten concepts. These guidelines are the key to separating the organization’s transactions from personal transactions, standardizing currency units, disclosing time periods, etc.

Alternatives to GAAP

Most countries outside the US follow the International Financial Reporting Standards (IFRS). The IASB (International Accounting Standards Board) oversees IFRS. Though US GAAP and IFRS have a few differences in principles, rules, and guidelines, work is ongoing in merging the two systems.

What About UK GAAP?

You might have heard the word UK-GAAP as well. This might make you believe that the UK has its own Generally Accepted Accounting Principles. However, it is not true as there is no such thing as UK-GAAP. The UK follows IFRS for accounting, and it is often referred to as UK GAAP.