Initially, many countries developed their own accounting standards. All these standards were different from others in a way that each had a different approach, such as tax-oriented, principle-based, business-oriented, rules-based, and more. However, the need was felt with globalization to unify all different standards. Or to harmonize different accounting standards. After the ’90s, there were two dominant standards – the GAAP and IFRS. Although similar in most areas, there are a few differences between GAAP vs IFRS.

GAAP vs IFRS: Importance

Generally Accepted Accounting Principles (GAAP) and International Financial Reporting System (IFRS) are currently the two primary accounting frameworks in the world. Both the accounting frameworks set ethical standards and accepted guidelines for financial accounting. Also, they lay down rules, procedures, and conventions for accepted accounting practice.

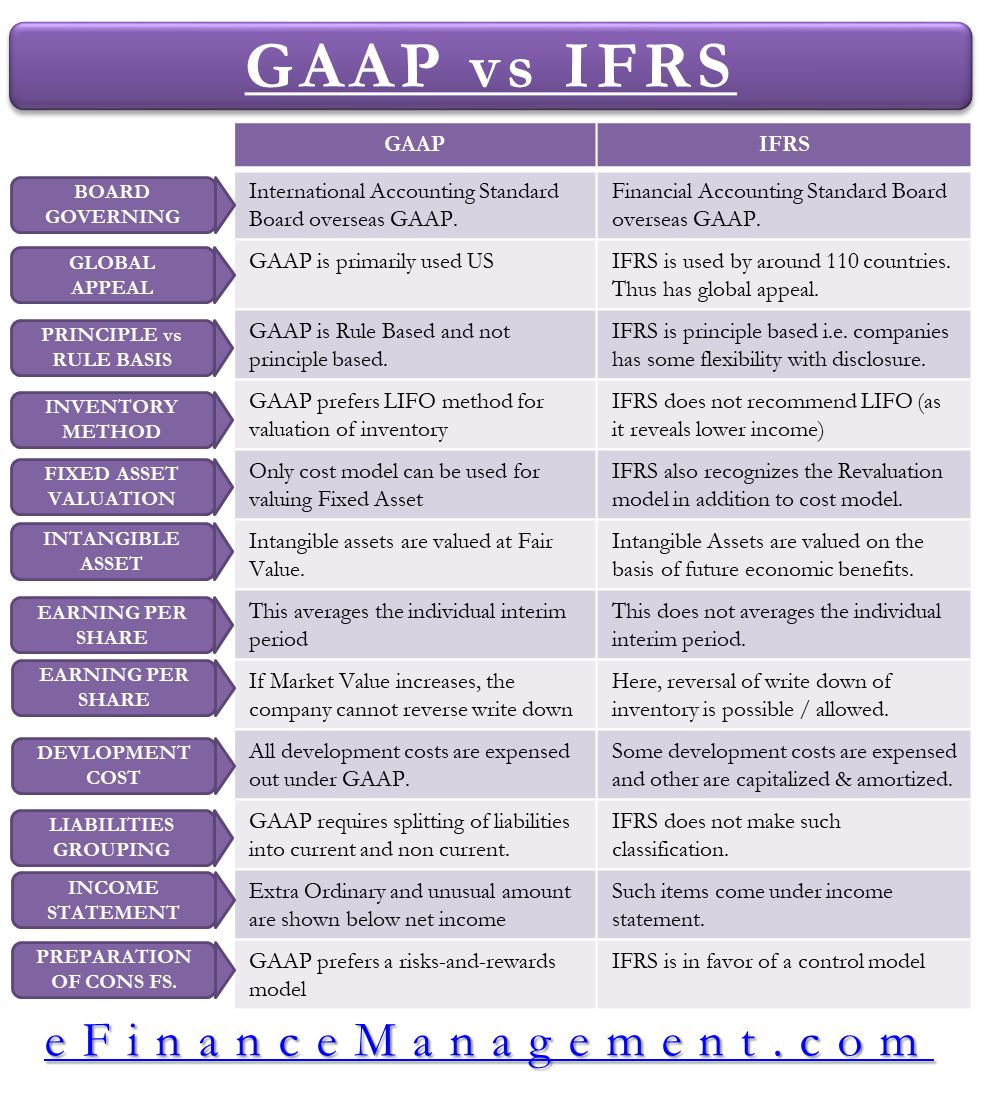

Any company that wants to do business globally, including in the US, must understand the differences between the two. IASB (International Accounting Standards Board) oversees the IFRS, while the FASB (Financial Accounting Standards Board) is responsible for the GAAP.

Though the organizations overseeing both GAAP and IFRS are working to minimize the differences between the two frameworks, there are still a few differences between the GAAP vs. IFRS. To better understand the two standards, it is important to understand the differences between GAAP vs. IFRS.

Also Read: Importance of GAAP

GAAP vs. IFRS: Differences

There are hundreds of differences between the two accounting systems that are constantly being adjusted to make the two same. Some of the major differences between GAAP and IFRS are as below:

Global Appeal

GAAP is primarily in use in the United States and has a different set of rules and regulations than IFRS. On the other hand, over 110 countries follow International Financial Reporting Standard and, thus, have a global appeal. Companies that expand internationally prefer to keep their books as per IFRS. This makes it easier for the organization and the stakeholders to understand and compare the financial statements.

Principle-based vs. Rule-based

A major difference between GAAP vs. IFRS is that the latter is principle-based, whereas GAAP is rule-based. The principle-based approach opens the window for different interpretations of similar transactions. This gives the organizations some leeway but requires extensive disclosure. IFRS, however, also has guidelines that can be considered more like a set of rules rather than a set of principles.

Further, both GAAP and IFRS differ in methodology for the treatment of accounting items. GAAP is more inclined towards the literature, whereas in IFRS, reviewing facts and pattern is more thorough.

Also Read: GAAS vs GAAP

Inventory Methods

GAAP prefers using the LIFO (Last In First Out) as an inventory method for estimating inventory. IFRS, however, does not approve this method as LIFO does not reveal the actual flow of inventory in most cases, resulting in unusually low-income levels.

Valuing Fixed Asset

As per the GAAP, a company should show fixed assets at its cost, net of any accumulated depreciation. Under IFRS, a company can revalue fixed assets. Therefore, the value on the balance sheet increases. Although the IFRS approach makes more sense in theoretical terms, it also requires more accounting efforts to calculate.

Intangible Assets

Under GAAP, intangible assets – such as research and development or advertising costs – are recognized at fair market value. However, IFRS considers the future economic benefit of the intangible asset when assessing its value.

Earning-per-Share

While calculating EPS (earnings per share) under IFRS, the company does not average the individual interim period calculations. Under GAAP, however, the calculation considers averages of the individual interim period.

Inventory Reversal

One major difference between GAAP vs. IFRS is the inventory write-down reversal treatment. Under GAAP, if the market value of an asset increases, the company can’t reverse the amount of write-down. On the other hand, under IFRS, a company can reverse the amount of write-down. We can say that GAAP is conservative when it comes to the inventory reversal and refrains from reflecting any positive changes in the marketplace.

Development Cost

Under GAAP, the company charges all the development costs to expenses as and when the company incurs them. IFRS, however, allows capitalization and amortization of some of these costs over multiple periods. GAAP’s treatment might be conservative, while IFRS treatment might be too aggressive in allowing deferment of costs that should have been charged to the expenses at the time when they are incurred.

Classification of Liabilities

GAAP requires splitting the current liabilities into two categories – Current and Non-Current liabilities. Current liabilities are those that the company can settle within 12 months. Non-current liabilities are long-term debt with a time period of more than 12 months. IFRS does not make any such classification of liabilities, and a company considers all debts as non-current on the balance sheet.

Income Statements

A company shows extraordinary or unusual items in GAAP below the net income section of the income statement. Under IFRS, such items come in the income statement.

Consolidation

GAAP prefers a risks-and-rewards model, while IFRS favors a control model. Therefore, business entities that may be consolidated under GAAP may be shown separately under IFRS.

Final Words

Both GAAP and IFRS have been running for decades. Therefore, it is no surprise that experts are in discussion to converge the guidelines and principles of the two, making it simpler for the world to understand and follow the basic set of guidelines. This work towards convergence has been ongoing for the past many years and still requires a lot of effort, as is evident from the differences above.

Some experts, however, are not in favor of the convergence to make a universal rule. They believe that both GAAP and IFRS should focus on improving their own standards rather than worrying about convergence.

Quiz on GAAP vs IFRS

This quiz will help you to take a quick test of what you have read here.

i need to know more about IFRS,so this app.is good for me

Thanks for the compilation of the differences. it was easy to understand.

Thanks for sharing your experience

Happy reading

This is a very necessary point. Thank you for sharing

I would really like to thank you because this topic made me understood the difference between IFRS and GAAP and their similarity as well as disclosure.