What is Operating Cash Flow?

Cash Flow is an essential part of any company’s financial statement. Operating Cash Flow shows the quantum of cash movement and the net positive cash flow generation by the company from its operating activities. Moreover, it is a measure of whether the company is self-sufficient and can generate positive cash flows from its operating / business activities. And whether the quantum of positive cash flow can help the company to grow its operations.

This statement illustrates and describes the sources of cash generated and cash used in ongoing business activities for a given period. It allows the business managers to monitor where the money is coming from and where it has gone. It further helps them maintain the minimum cash required for business exigencies and assists in making business decisions. This statement primarily has Net income coming from the Income Statement, adjustments to the Net Income, and movement in items of Working Capital.

Operating Cash Flow Movement – Example

Every entity has its own way of working, different sources, and manner of earning and spending money. To have a positive cash generation continuously, the entity has to generate profits regularly from its operational activities. To generate a net profit, earnings must be more than the expenditures or outflow of funds. Continuity of profits or positive cash flow only makes a company stable and healthy and provides for funds to make new investments, take up new opportunities, and expand operations. Moreover, it makes available funds for the up-gradation of infrastructure, up-gradation of equipment/machinery, installation of software, etc.

But such types of spending are occasional in nature. The company’s spending in terms of salaries, rent, utilities, and materials procurement should be lower than the income company derives by selling its products/services. This is important to maintain a positive cash flow for the company. If not, the company will have to resort to the taking of loans/borrowings for survival. When the company uses such loans/borrowings for bridging the gap, this adds to the assets and liabilities in the cash flow statements.

Also Read: Cash Flow Statement – Definition and Meaning

Operating Cash Flow Movement – Example

Operating cash flows are a benchmark to estimate the success and liquidity status of any company. As in the annual accounts, the cash flow statement consists of the total cash flow movement of the business during the year. However, if we observe, these movements are related to three types of transactions. The first one is from the business operations, and the other two types of flow belong to investing and financing activities. The first part describes the link between what the business earns and spends from its operating activities, i.e., revenue earned from the sale of products/services and expenditures incurred.

When the company buys raw materials and pays salaries to employees and wages to workers, it is incurring operating expenses. Operating Income is when the company receives money from customers as a result of the sale of products and services. If the business model is healthy, the operating revenue will be more than the operating expenses. This will result in positive cash flows for business operations.

Suppose a company has a policy to stock inventory on higher levels due to the seasonal nature of products or sales. This will give rise to more raw materials purchases, additional wages to workers, and correspondingly low operating revenue. This excessive spending may give rise to negative cash flow from operations. Also, if the customer delays the payment, or the business model is such that the customers have enhanced credit cycles. This delay could reduce the inflow and may thus result in negative cash flow. In that case, the company has to develop and rely on alternate sources of funds/borrowings for survival.

How is Operating Cash Flow Calculated

The basic formula for calculating the operating cash flow is

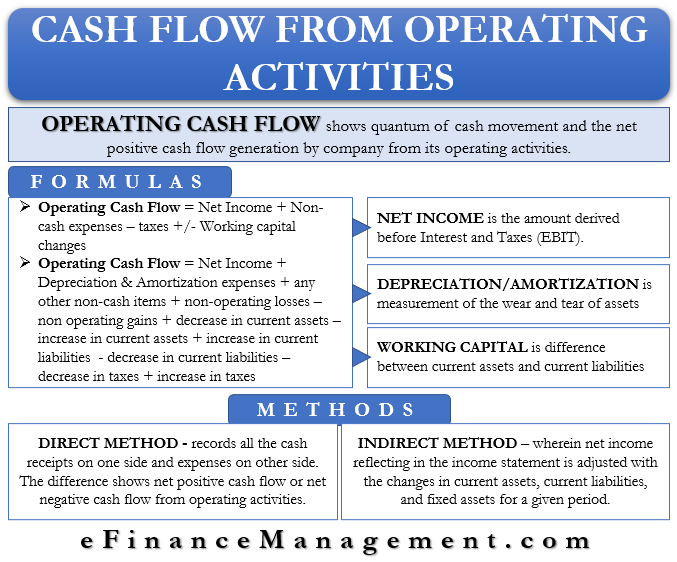

Operating Cash Flow = Net Income + Non-cash expenses – taxes +/- Working capital changes

The detailed formula is as given below

Operating Cash Flow = Net Income + Depreciation & Amortization expenses + any other non-cash items + non-operating losses – non operating gains + decrease in current assets – increase in current assets + increase in current liabilities – decrease in current liabilities – decrease in taxes + increase in taxes

Also Read: Cash Flow Vs. Fund flow

Net Income

Net Income is the amount derived before Interest and Taxes (EBIT). It comes from the Income statement and is the leftover amount after deducting all the expenses from sales revenue.

Depreciation & Amortization Expenses

Depreciation is a measurement of the wear and tear of the assets due to its use over a period of time. On the other hand, amortization is the spreading of the initial costs of the assets over the life of the asset. These expenses are taken to the profit and loss account and deducted from the income every year.

Working Capital

Working capital is basically the difference between the current assets held by the business vis-a-vis the current liabilities it has on the day of preparation/presentation. It provides detailed information on the use of capital in day-by-day business activities.

Current assets consist of assets of the business that fluctuate regularly. We can also say it as the operating assets. It mainly consists of inventory, cash, and bank balances, sundry debtors, etc. And all these assets balance undergo changes every day.

Similar to the current assets, Current Liabilities are again fluctuating daily with each and every business transaction. It mainly consists of various regular outstanding payments and sundry debtors.

Methods of Operating Cash Flow

There are two methods for calculating the OCF:

Direct Method

This method records all the cash receipts on one side, like cash received from customers, interest & dividends received from the sale of scrape, etc. On the other side, it records all the cash expenses in salaries to employees, cash paid to creditors, interest obligations on loans, taxes, etc. Thus, one side shows all the cash inflow sources. And the other side shows all the outflow of cash during the period. The difference between the two sides is either net positive cash flow or net negative cash flow from operating activities. It is positive when the income is more and vice versa.

Indirect Method

In this method, the cash flow from operating activities is arrived at after making the necessary adjustment to the net income. The net income reflecting in the income statement is adjusted with the changes in current assets, current liabilities, and fixed assets for a given period. This gives the business managers a picture about the uses of cash in the business and details of cash generation from operations.

The Indirect method of cash flow preparation is the most popular because the information required for preparing the cash flow statement is readily available from the company’s financials.

Read more on why is the indirect method of cash flow better.

Importance of Operating Cash Flow

Cash flow from operating activities is an immediate health indicator and reveals the sound financial position for any company. Investors, analysts, and creditors look towards the working capital ratio or current assets to current liabilities ratio as a first step to understand the operating status of the company. They all prefer a higher ratio of more than 1 for this ratio. This ratio of more than one demonstrates that the company can fully pay off its current short-term liabilities. Moreover, it still has some earnings left over. And this money can be used by the company for investing and financing schemes. The ultimate objective is to increase revenue and profit-generating capacity. For instance, going for the expansion plans, investment in equipment/machinery, repayment of long-term borrowings to reduce the interest outgo, to stock inventory to take advantage of seasonal pricing, etc.

Guidelines on Preparation of Cash Flow Statement

As with the other financial statements like Balance Sheet and Profit & Loss Account, guidelines on preparing cash flow statements are governed by Generally Accepted Accounting Principles (GAAP) and IFRS. These guidelines provide how a company should prepare and report its cash flow statements and how it manages cash. These guidelines are uniform in nature across various industries and countries. And thus, statements made as per the guidelines provide its users consistency in understanding and comparing them.

Excellent way of explaining the financial jargon and its importance in very simple way that even non finance people / investors will understand the meaning and importance of Operating Cash Flow and to know the strength of the Company