Cash Flow and Cash Flow Statements

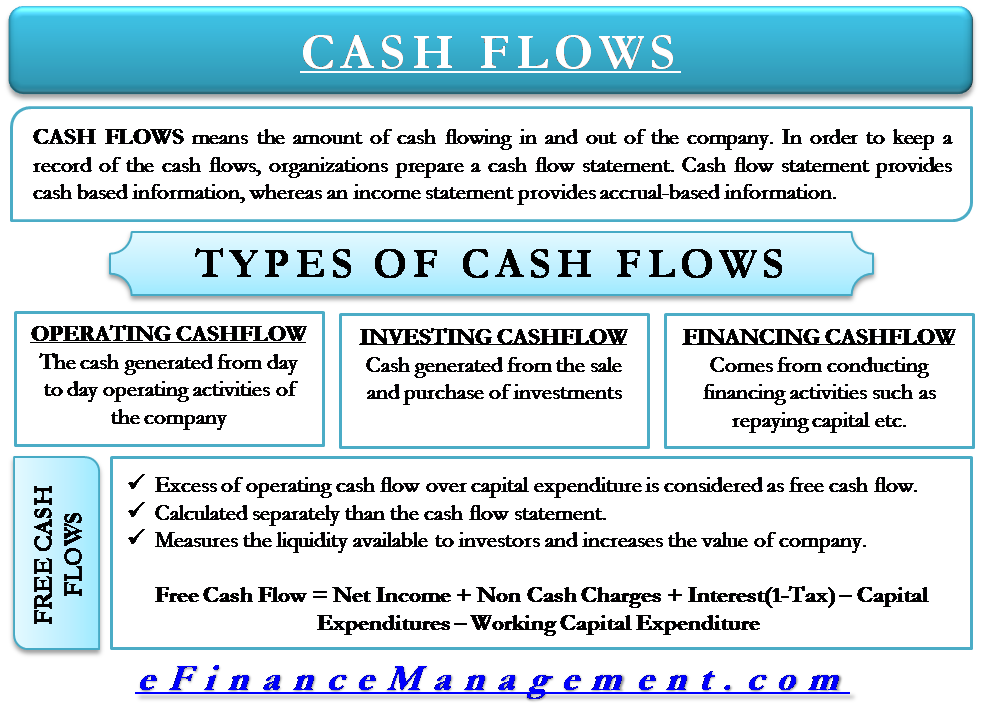

As the name suggests, cash flow means the amount of cash flowing in and out of the company. To keep a record of the cash flows, organizations prepare a cash flow statement. Hence we can say that a cash flow statement provides information about a company’s cash receipts and cash payments during an accounting period. Let us see the types of cash flows in detail.

Importance of Cash Flow Statement

In sophisticated terms, a cash flow statement provides cash-based information, whereas an income statement provides accrual-based information. What does that mean? Let’s understand it with a comparison. For example, the income statement shows revenues when earned rather than when cash is collected. Suppose Company X did a sale transaction of USD 500.00 on January 1, 2019, with a credit period of 30 days. The income statement will reflect the sale as on January 1, 2019; however, the cash flow statement will reflect this transaction after the company receives payment for the goods, i.e., on or after January 30, 2019.

So one may ask – how is this useful for me? As an investor, a cash flow statement is an extremely important tool to diagnose the financial health of a company. Let’s take a hypothetical example of a company making extremely good sales at a very good margin, never collecting any payment for its sales. The company’s income statement will show how good the revenue and earnings are. However, when we look at its cash flow, we will realize that the cash flow is negative, and negative cash flow is not sustainable. To survive, companies need cash, even better when companies are cash rich, and the indicator of cash is a cash flow statement.

Types of Cash Flows

Now that we understand the importance of cash flows, let’s see the types of cash flows that are in use:

Operating Cash Flow

The cash flow generated from operating activities is termed operating cash flow. Operating activities include a company’s day-to-day activities, for example, purchasing raw materials or making sales. Cash inflows result from cash sales and collection of accounts receivable. This is basically the revenue generation from the main activity of the business. For example, Apple Inc.’s revenue comes from sales of its electronics. To generate these revenues, companies have to undertake operations such as purchasing raw materials, manufacturing inventory, paying employees, etc. Thus cash outflows result from cash payments for raw materials, salaries, taxes, etc.

Also Read: Cash Flow Statement – Definition and Meaning

Finally, the cash outflows are subtracted from cash inflows, and the resultant amount is operating cash flow or net cash flow from operating activities.

The formula can be derived as –

Operating Cash Flow = Cash inflow from operating activities – Cash outflow from operating activities

Investing Cash Flow

The cash flow generated from investing activities is termed investing cash flow. Investing activities include the purchase and sale of long-term assets and other investments. Cash outflows are generated from investments in long-term assets, and other investments include property, plant, and equipment; intangible assets; both long-term and short-term investments in equity and debt issued by other organizations; etc. The cash flow generated from the purchase of securities or assets solely for the trading purpose or for the primary business activity of the company is not included in investing cash flow. For example, suppose an Indian exporter hedges US dollars to minimize the effect of USD-INR price fluctuation in his current orders. In that case, the cash flow from this hedging will go to operating cash flows and not investing cash flows.

Cash inflows include the sale of non-trading securities, property, plant, and equipment; intangibles; and other long-term assets. After that, the cash outflows are subtracted from cash inflows, and the resultant amount is investing cash flow or net cash flow from investing activities. The formula is –

Investing Cash Flow = Cash inflow from investing activities – Cash outflow from investing activities

Financing Cash Flow

Financing cash flow comes from conducting financing activities for the business. In other words, financing cash flow includes obtaining or repaying capital, be it equity or long-term debt. Cash inflows in this category include cash receipts from issuing stock or bonds and from borrowing through long-term loans. Cash outflows include cash payments to repurchase stock and repay bonds and other borrowings.

Subsequently, the cash outflows are subtracted from cash inflows, and the resultant amount is financing cash flow or net cash flow from financing activities. The formula is –

Also Read: Cash Flow from Operating Activities

Financing Cash Flow = Cash inflow from financing activities – Cash outflow from financing activities

These are the basic three cash flows. However, the term free cash flow confuses many people. So we are going to understand free cash flow as we proceed.

Free Cash Flow

Free cash flow is not a different type of cash flow, but it is more like a measure of performance. It is not specifically mentioned in any cash flow statement, so it has to be calculated separately while analyzing a company’s cash flow statement.

Free Cash Flow – Definition

So what exactly is free cash flow? Generically, the excess of operating cash flow over capital expenditure is considered free cash flow. In layman’s terms, after all the operating expenses are paid, the amount of cash available to debt providers and equity holders of the company is termed free cash flow.

Importance of Free Cash Flow

Free cash flow is a very important tool for investors. It measures the liquidity available to investors. The higher the free cash flow, the more cash-rich the company is. All this cash can be further invested in the growth of the company or can be paid as a dividend. Eventually, it will increase the value of the company, and that will lead to a growing investor portfolio.

Calculating free cash flow to the firm can get a little tricky as the formula is a little lengthy and requires strong analytical skills. Following is the formula:

A formula for Free Cash Flow to the Firm

Free Cash Flow to the Firm = Net Income

+ Non-cash Charges (example – depreciation and amortization)

+ Interest (1-Tax Rate)

– Capital Expenditures (fixed capital such as equipment)

– Working Capital Expenditures

The resultant amount is the free cash flow available to equity and debt holders in the company.