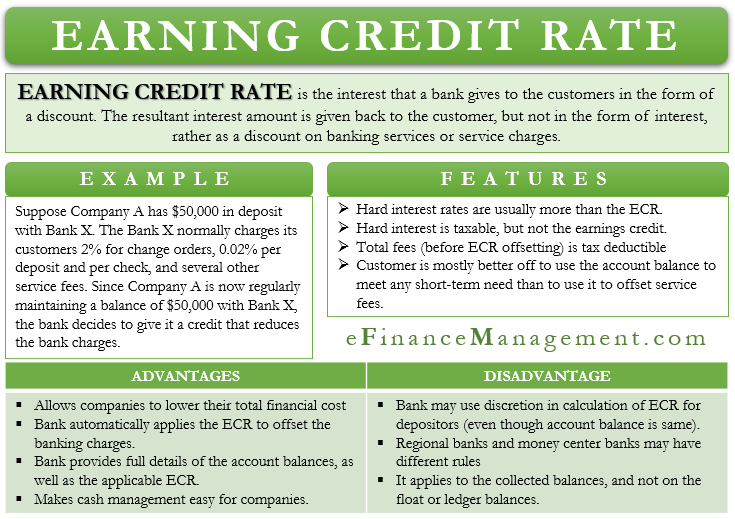

Earnings Credit Rate or ECR is the interest that a bank gives to the customers in the form of a discount. Banks calculate ECR on the money that customers leave in non-interest-yielding accounts. The bank calculates the ECR on the account balance. And the resultant interest amount is given back to the customer, but not in the form of interest, instead of as a discount on banking services or service charges.

It is a common term on a U.S. commercial account analysis and billing statement. Usually, banks peg ECR to the U.S. Treasury bill.

Earnings Credit Rate – Explained?

ECR benefits both the bank and the depositors. A customer with many banking transactions can save a noteworthy sum of cash or bank charges and service fees with ECR. On the other hand, it encourages customers to maintain a bigger balance with the bank, which helps the bank.

Banks may use ECR to lower the fees that customers pay for banking services. Such as debit card fees, draft fees, loan processing fees, etc. Thus, it benefits customers who regularly maintain more than the reserve balance in their account(s).

Banks, however, exercise discretion when it comes to giving the benefits of ECR to the customers. To ensure that they get the full benefit of the ECR, the depositors must note the charges they pay to the bank.

Also Read: Discount Rate – Meaning, Importance And More

Suppose Company A has $50,000 in deposit with Bank X. Bank X normally charges its customers 2% for change orders, 0.02% per deposit and per check, and several other service fees. Since Company A is now regularly maintaining a balance of $50,000 with Bank X, the bank decides to give it a credit that reduces the bank charges.

Let’s take another example. Suppose the ECR of Bank X is 2%, and Company A maintains a balance of $50,000. In this case, Company A will get $1,000 as a credit to offer bank charges. This means that if Bank X has a total monthly service charge of $1,500, then Company A will have to pay just $500.

History of Earnings Credit Rate

At the time of the Great Depression, the government came up with a Regulation Q. This regulation made it illegal for a bank to give interest to commercial DDAs (demand deposit accounts). The objective was to discourage commercial accounts from depositing money in the banks rather than encourage them to invest in other investment avenues, such as the money market.

On the other hand, to prevent such an outflow of funds, banks started offering earnings credit. This credit applied to bank fees for the commercial demand deposit account. Later, the Dodd-Frank Act did away with the Regulation Q part that blocked “hard interest” on the DDA account.

Features of Earnings Credit Rate

Following are some of the features of Earnings Credit Rate:

- The hard interest rates are usually more than the ECR.

- Hard interest is taxable, but not the earnings credit.

- The bank service fees that ECR offsets are not deductible. Instead, the fees without offsetting are deductible on the tax return.

- A customer is mostly better off using the account balance to meet any short-term need than to use it to offset service fees.

Advantages

The following are the benefits of Earnings Credit Rate to both depositors and banks:

- It allows companies to lower their total financial cost or boost their operating margin and profit. This, in turn, boosts the shareholders’ value.

- A bank automatically applies the ECR to offset the banking charges. Thus, a depositor does not have to waste time and resources to convince the bank for ECR.

- Bank provides full details of the account balances, as well as the applicable ECR. This ensures transparency.

- ECR makes cash management easy for companies. This is because there is no lock-in, and depositors can access their funds immediately.

- For banks, ECR means they get more funds from the depositors, which they can use to generate more returns or meet other needs.

Disadvantages

The following are the drawbacks of ECR:

- Since banks have discretion over ECR, we may see a variation in the ECR that a bank may offer to depositors, even if they have the same amount of funds in the account.

- Regional banks and money center banks may have different rules for Earnings Credit Rate.

- One big drawback of ECR is that it applies to the collected balances. It is money that is on hand to invest or transfer. This means ECR does not apply to float or ledger balances.

Do You Need ECR?

To determine whether or not you need ECR, you should ask yourself three questions:

- Do you want to earn a profit or reduce your cost? If your answer is reducing the cost, then you should go for the ECR.

- Do you do enough banking transactions, or do you have enough banking fees to offset? You should calculate the average banking fees that you pay. If you feel it is significant enough, you can go for ECR to offset it.

- Is ECR in-line with your investment and accounting policies? Before you go for the ECR, it is prudent to make sure it aligns with your investment objectives.

Once you are certain that you want to go for the ECR, you need to consider the following points to optimize its benefits:

- Determine your cash needs and the amount of cash that should be available to you at any time.

- Analyze the counterparty risk or operating risk metric to ensure ECR is within your risk appetite.

- Regularly review your deposit portfolio so that you don’t miss any profitable opportunities.

- Don’t leave things entirely to the bank. Instead, work with the bank, ask questions about the calculation, and always negotiate terms to your advantage.

Earnings Credit Rate is an attractive option when the market interest rates are zero or near zero. In case of an increasing interest rate scenario, the depositors may be better off investing their money in an interest-bearing account.

Final Words

The concept of ECR is gaining popularity outside of the U.S. as well. The benefit it brings makes it appealing to companies that usually keep large balances with the bank. Moreover, companies that pay a large service fee regularly to the banks. Banks, on their end, are also working to make ECR more attractive to the depositors. They are trying to add more banking services that ECR can offset. Because of higher deposits, the banks can also increase their volume and gain from deployment in profitable opportunities.

Quiz on Earnings Credit Rate (ECR)