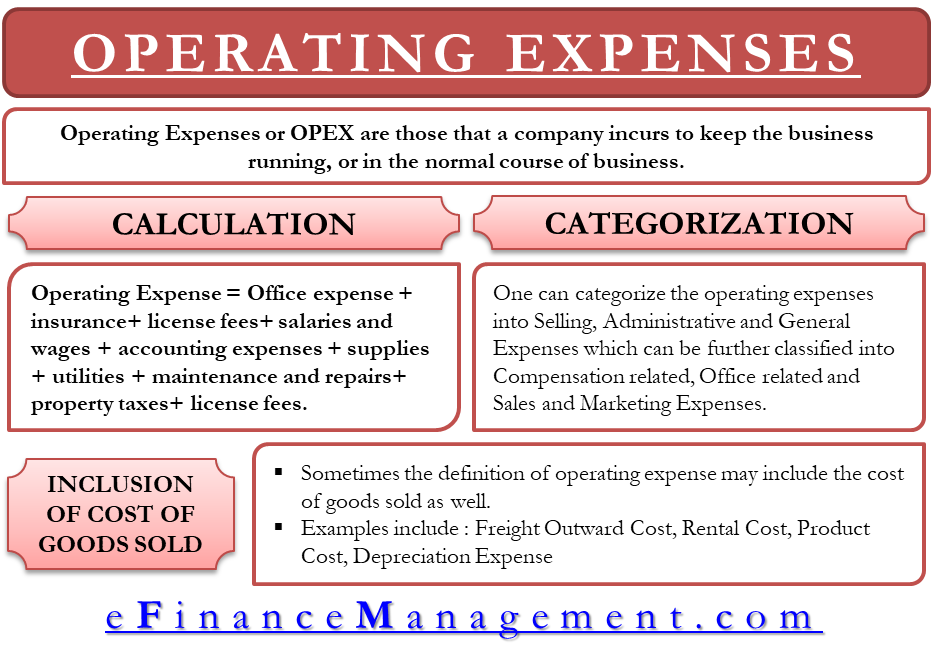

Operating Expenses or OPEX are those that a company incurs to keep the business running or in the normal course of business. A company usually incurs these to meet the regular expenses to run a firm. Expenses such as payroll, travel expenses, amortization, rent, taxes, repairs, and so on come under operating expenses.

Importance

Such expenses are crucial for calculating operating income, which is an important financial measure. Operating expense depends on several things, such as pricing strategy and the company’s overall management. Therefore, a careful study of operating expenses gives a good idea of a company’s managerial flexibility and competency.

Also, comparing operating expenses between companies gives a fair idea on which is more efficient of the two. A point to note is that some industries have more operating expenses than others. So, comparing operating expenses is more meaningful when we take companies within the same industry.

Formula

Operating expenses may be different for different companies. So, there is no one formula that fits all companies. However, the basic formula of an operating expenses formula is –

Also Read: CAPEX vs OPEX – All You Need To Know

Operating Expense = Office expense + insurance+ license fees+ salaries and wages + accounting expenses + supplies + utilities + maintenance and repairs+ property taxes+ license fees.

This is not a comprehensive list of the operating expenses. Every company may have its own unique structure on the basis of its business. These expenses would be shown on the income statement and calculated along with other costs.

Categories of Operating Expenses

One can categorize operating expenses into Selling, Administrative, and General Expenses (SG&A). One can sub-categorize SG&A into compensation-related expenses, office-related expenses, and sales and marketing-related expenses.

Some common compensation-related operating expenses are – sales commissions, benefits and pension plan contributions for non-production employees, and compensation for non-production employees.

Examples of office-related operating expenses include insurance costs, legal fees, office supplies, property taxes, utility costs, accounting expenditures, and rent and repair costs for non-production facilities.

Also Read: What is Expense? – Definition and Meaning

Examples of sales and marketing-related expenses – include sales material costs, travel costs, and advertising costs.

All these costs together constitute Selling, Administrative, and General Expenses (SG&A). Some of these are discussed in detail below;

Traveling Expense – Employees of the company might go on official visits for meetings and conferences. The company bears these expenses. A company puts these expenses in the Profit and Loss statement as travel expenses.

Office Equipment & Supplies – To carry its day-to-day activities, a company regularly needs office supplies and equipment such as desktops, laptops, printers, stationery supplies, etc. These expenses also form a part of the operating expense.

Property Tax – A company might be paying rent for the office. Such an expense also forms the part of operating expense.

Utility Expense –These payments relate to the office utilities that the company pays, such as water, electricity, etc.

Bank Charges – Fees that a bank charge for its services, such as a debit card fee and more, also comes under operating expense.

Does it Includes Cost of Goods Sold (COGS)

Sometimes the definition of operating expense may include the cost of goods sold as well. In such a case, it would include expenses attributable to the production of goods. A point in favor of taking COGS as an operating expense is that considering it gives an accurate operating income.

Some examples of the cost of goods sold are –

Freight out Cost –The cost of transportation for the delivery of the goods from supplier to customers comes under the cost of the goods sold. Thus, it comes in the income statement.

Rental Cost – The companies pay rent for the production facilities. Moreover, wages, salaries, and various employee benefits are also part of the cost of goods sold.

Product Cost – The cost that a company incurs to manufacture a product to sell it to a customer is a product cost. The product cost includes direct labor, direct material, and direct overheads.

Depreciation Expense – Drop in the value of an asset due to wear and tear during the production time is known as depreciation expense. It is also a part of the cost of goods sold.

Operating expenses does not include finance cost as it does relate to day to day operations of the business.

Operating Expense vs. Capital Expense vs. Non-operating Expense

As you now know, operating expenses are the expenses that a company incurs to run a business on a daily basis. On the other hand, a company incurs capital expenses or capital expenditure when it spends money, raises money via debt or some other source to invest in an asset, or expands the value of an existing asset.

A capital expenditure helps a company to reap the benefits in the long run, typically beyond a year. On the other hand, operating expenses are for a certain period, such as rent for a year.

A company records an operating expense in the income statement. Capital expenditure comes as an asset on the balance sheet. A point to note is that depreciation on assets comes in the income statement as an expense. After that, the accumulated depreciation comes into the balance sheet as the sum total of all the depreciation expenses.

Non-operating expenses are those that are not related to the core operations of a business. For example, depreciation, interest charges, amortization, or other costs of borrowing.

Read CAPEX vs. OPEX for more details.

Final Words

Every company must try to lower the burden of operating expenses as much as it can. Such expenses have a direct impact on profitability. It also affects’ the ability of a company to compete with others in the industry. However, these expenses are necessary and unavoidable. And there are examples when reducing such expenses compromises the integrity and quality of operations. Therefore, it is important for a company to strike the right balance with operating expenses.