Cash flow and fund flow are two different statements calculated for various purposes. Investors, financial analysts, and management use these statements to make important investment decisions regarding the company or the stock.

Difference between Cash Flow and Fund Flow Statements

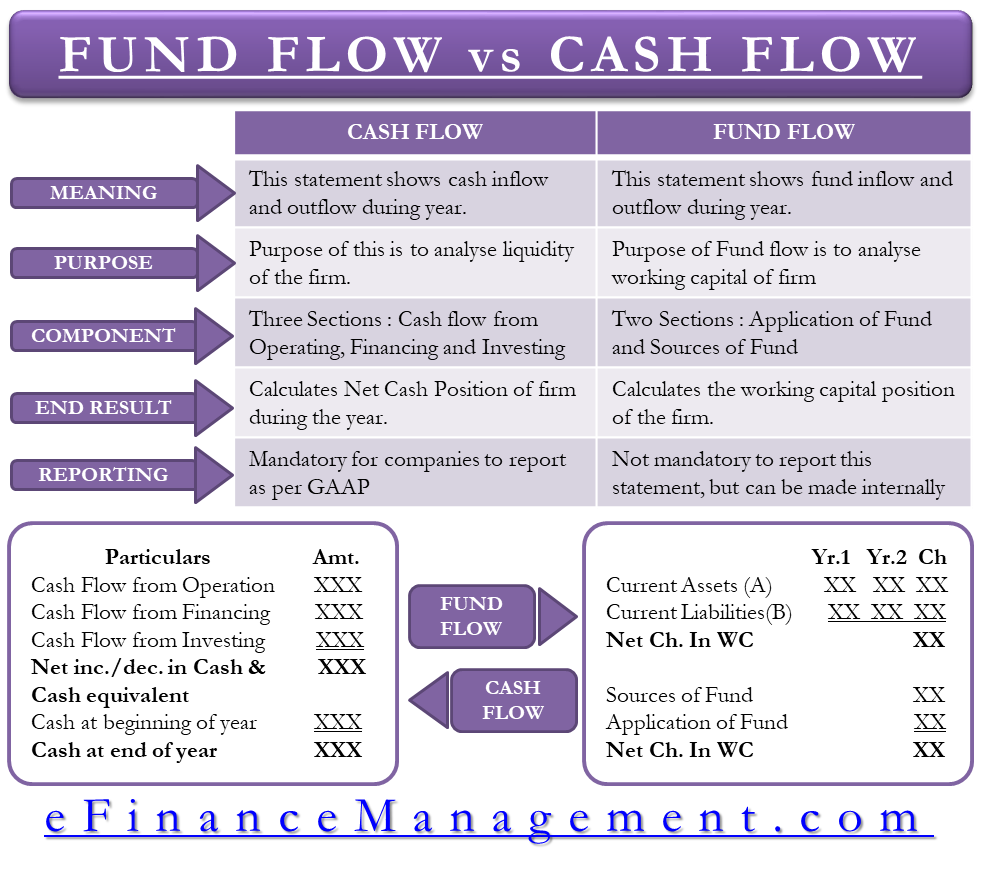

Meaning

Cash flow is a financial statement that details the cash inflows and outflows that happened during that particular accounting period. It describes how each transaction has resulted in a change in the company’s cash position and calculates the company’s net cash flows at the end of the accounting period.

The fund flow statement details the inflows and outflows of funds during a particular accounting period. It analyses the changes in the source of funds and the application of funds during an accounting period. It calculates the financial position of a company at the end of the period.

Purpose

The main purpose of a cash flow statement is to analyze a firm’s liquidity. Each section of a cash flow statement shows how the cash moved during that particular accounting period. The end result is the total cash present with the company during that period. Investors are keen on this figure as this is the amount available for making investments, repaying debt, etc.

Also Read: Cash Flow Statement – Definition and Meaning

A fund flow statement is built to analyze the working capital of a firm. This statement closely observes how efficiently its funds are utilized in carrying out day-to-day operating activities. The end result of a fund flow statement is the change in the working capital from the previous year to the current year.

Components

A cash flow statement comprises of three sections – cash flow from operations (calculates the amount of cash generated from regular business activities like revenues from sales, expenses, working capital, etc.), cash flow from investing (details the amount of cash invested by the company in capital expenditure like buying a plant, machinery, etc. and any other long-term investments like marketable securities and acquisitions) and cash flow from financing activities (calculates the amount generated or spent by the company through the issuance of debt and equity).

A fund flow statement consists of two main components – changes in working capital and a statement reflecting the sources and application of funds. The working capital schedule captures the increase and decreases in the current assets and current liabilities during two accounting years. The statement of sources lists down the amount realized by the company through issuing shares, debt, sale of fixed assets, etc. The application of funds section captures the information on where the funds were utilized, like repayment of loans, purchase of fixed assets, increase in working capital expenditures, and other expenses.

Structure

Cash Flow

| Particulars | ($) | ($) |

| Operating Activities | ||

| – | XX | |

| – | XX | |

| – | XX | |

| Net cash provided by operations (A) | XXX | XXX |

| Investing Activities | ||

| – | XX | |

| – | XX | |

| – | XX | |

| Net cash provided by investing activities (B) | XXX | XXX |

| Financing Activities | ||

| – | XX | |

| – | XX | |

| – | XX | |

| Net cash provided by financing activities (C) | XXX | XXX |

| Net increase or decrease in cash and cash equivalents (A+B+C) = (D) | XXX | |

| Cash and cash equivalents at the beginning of the year (E) | XX | |

| Cash and cash equivalents at the beginning of the year (D+E) | XXX | |

Fund Flow

Working Capital Schedule

| Year 1 | Year 2 | Increase | Decrease | |

| Current Assets | ||||

| – | ||||

| – | ||||

| – | ||||

| Total Current Assets (A) | ||||

| Current Liabilities | ||||

| – | ||||

| – | ||||

| – | ||||

| Total Current Liabilities (B) | ||||

| Change in Working Capital (A-B) | ||||

| Net Increase/Decrease in Working Capital | ||||

| Total |

Statement of Sources and Uses of Funds

| Particulars | ($) | ($) |

| Sources of Funds | ||

| – | XX | |

| – | XX | |

| – | XX | |

| Total Sources of Funds (A) | XXX | XXX |

| Uses of Funds | ||

| – | XX | |

| – | XX | |

| – | XX | |

| Total Uses of Funds (B) | XXX | XXX |

| Changes in Working Capital (A-B) | XXX | |

Read Sources and Uses of Funds for more details.

Summary

| Basis | Cash Flow | Fund Flow |

| Purpose | Analyses the inflows and outflows of cash in a particular accounting period | Analyses the sources and applications of funds generated by the company in a particular period |

| Objective | Shows the company’s liquidity – whether it has enough cash to carry out its day-to-day activities or not. | Analyses the company’s financial position – whether it is managing its working capital efficiently or not. |

| End result | Calculates the net cash position of the company at the end of the accounting period | Calculates the changes in working capital during the period |

| Reporting | Mandatory for companies to report this statement for each period in their earnings releases, according to GAAP principles | Not mandatory for companies to report fund flow statements, but it can be calculated from the balance sheet |