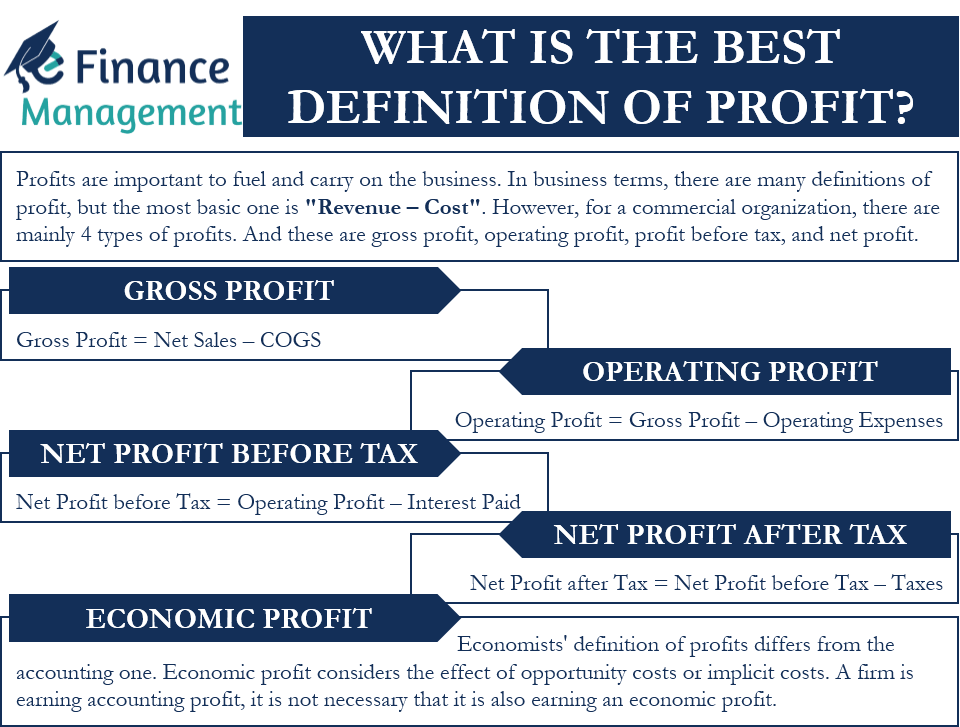

Profits are an integral part of every business. As an entrepreneur, the primary goal is to make the business profitable. Profits are important to fuel and carry on the business. It helps in proving the credibility of the idea and acts as an attractive investment to many retail investors. It is the face of the company and is one of the parameters to assess the organization’s financial health and operational performance. There are many definitions of profits, one being excess gain over the cost incurred, or in simpler terms, profit is equal to an advantage or a benefit. In business terms, there are many definitions of profit, but the most basic one is “Revenue – Cost.”

Types of Profits and their Definitions

When a company is profitable, it creates a lot of opportunities. With profit being an indicator of how well a firm is doing, there are many dimensions through which we can view profits. All that what we call profits or earnings can be accessed or gazed from the entity’s financial statements. There can be different ways of presentations and terminologies. However, there are four types of profits for a commercial organization. And these are gross profit, operating profit, profit before tax, and net profit.

Of course, there are different names and sub-grouping also available. Like net profit after tax and dividend, retained profits, and so on. As these are dependent upon the type of presentations, type of organization, and the purpose of analysis.

Gross Profit

The simple formula for gross profit is Net Sales – COGS. When we deduct the cost of goods sold from the net revenue/net sales, we derive the gross profit. Now, every profit has its own implications. Gross profit, when divided by sales, tells us about the gross margin a firm earns after deducting its direct costs in acquiring and producing the goods.

Read EBIT for more.

Operating Profit

Gross profit minus all other indirect costs, depreciation, and amortization equals operating profit. A firm incurs various additional costs in the course of its operations, like marketing, administration, depreciation on assets, etc. All such costs are classified and termed as indirect costs. Thus, operating profit is the result after deducting all other expenses and provisions. Viewing operating profits in isolation will not contribute much to the analysis. And it should be viewed with respect to past performance, industry standards, and peers. Again, analysts interpret operating profit in various ways and for various purposes. Also, read Net Operating Profit After Tax (NOPAT).

Net Profit before Tax

“Operating Profit – Interest Paid.” In its simplest form, net profit before tax is the profit before paying tax but after paying interest on the debt. A capital structure is a balance between debt and equity. Using debt is an external source of finance and comes attached with a cost known as interest. Net profit before tax minus interest paid equals net profit before tax.

Net Profit after Tax

It is the final amount of earnings the company has made after deducting both direct and indirect costs pertaining to the business, including taxes. On an important note, dividends are not deducted from net profit before or after tax because net profit after tax is the income available to the shareholders. Hence, tax is deducted from net profit before tax to land up at the final amount of earnings of the firm.

What Happens Next?

So one would ask, where do these profits appear next? There are two routes, one is the distribution to the shareholders in the form of dividends. And the remaining goes to retained earnings. Retained earnings or net profit after tax appears in the balance sheet on the liability side as part of ‘shareholder’s equity. It is upon the firm’s discretion to utilize the profit in a meaningful and optimal way. The life cycle stage of a firm is also a critical deciding factor with regard to these routes. That means how much to distribute to the shareholders and how much to retain for entity usage. Generally, a matured firm in a defensive industry will pay out more as dividends to shareholders. Whereas a growing newly found start-up just turned profitable will prefer to re-invest in the growth and prosperity of the firm.

Economic Profit

The above discussions of profits are under the umbrella of accounting profits. Economists’ definition of profits differs from the accounting one. Economic profit considers the effect of opportunity costs or implicit costs. While accounting profit uses only the explicit costs. Opportunity cost is the cost of letting go of another opportunity to act upon the current venture. Or it is the cost of foregoing the alternative earning opportunity. Visit Accounting Profit vs. Economic Profit to learn more.

Example

For example, Sam plans to set up a business that needs capital. So, to obtain the capital, he has to sacrifice his current job, or he could have invested in a fixed deposit. Assume that the decision to invest capital in the new business is made by sacrificing the opportunity of using the capital in some other source that is, investment in fixed deposit. Hence, the interest forgone will be the opportunity cost here. In another scenario, if Sam is leaving his $ 50,000 job to pursue the new venture, then he is incurring an opportunity cost of $ 50,000. If a firm is earning accounting profit, it is not necessary that it is also earning an economic profit.