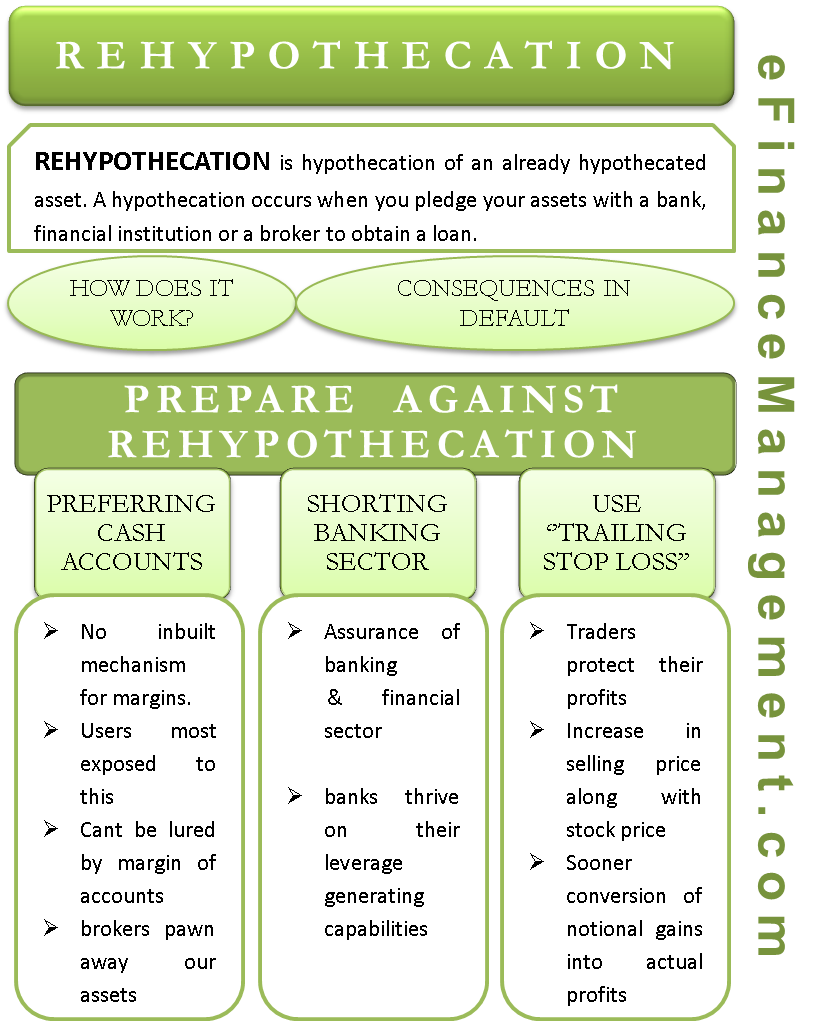

What is Rehypothecation?

Rehypothecation, most simply put, occurs when your assets are pledged with the “creditor of your creditor.” It is not as complex as it sounds.

To understand the concept of rehypothecation, it is necessary to refresh the definition of hypothecation. Hypothecation occurs when you pledge your assets to a bank, financial institution, or a broker to obtain a loan. Collateral is this pledged asset. The collateral remains free to be disposed of by the bank in case you do not repay the borrowed amount. In effect, the “property” or “ownership” in that asset passes from you to the bank.

Rehypothecation is the hypothecation of an already hypothecated asset. In other words, when your creditor bank or financial institution borrows money from another bank by pledging the asset you originally submitted as collateral, your creditor bank is said to have indulged in rehypothecation.

How does it Work?

In the US, Federal Reserve Regulation T and SEC Rule 15c3-3 allow the brokers to rehypothecation of collaterals submitted by the clients to the extent of 140% of the loan amount extended.

For example, you hold a margin account with a broker. You own shares of Co ABC worth $500. You come across another share of Co XYZ promising a handsome churn out. However, not having the liquidity to make the purchase of Co XYZ shares, you decided to make use of the margin facility available. You thus borrow $500 against your shares in Co ABC as collateral.

Also Read: Advantages & Disadvantages of Hypothecation

Your balance sheet will look like this:

| Equity (used to purchase ABC shares.) | $500 | Shares in Co ABC (Pledged) | $500 |

| Debt (with margin offered by the broker by pledging) | $500 | Shares in Co XYZ | $500 |

| $1000 | $1000 |

Thus, the broker can rehypothecate client assets to the tune of $700 (140% of the loan amount extended).

The frightening part is that such rehypothecation can occur without even as much as an intimation to us. Yes, the brokers and financial institutions are authorized to rehypothecate our assets without notifying us. Apparently, such clauses are part of the fine print of the agreement we sign while opening an account with them. In effect, we ourselves give consent to our own doom when we sign those papers.

Consequences of Rehypothecation – Default

As it is established, doubly pledging the collateral of the clients allows the banks to borrow additional funds. Now the same collateral bears the burden of multiple debts. First, the debt is extended by the financial institution to the original borrower. Second, the debt is extended by a third-party lender to the financial institution. Therefore, the property in the collateral ultimately passes from the original borrower to the financial institution to the third lender.

The worst thing that could happen in this cycle would be for the intermediary party, i.e., the financial institution, to default. The third-party lender would take over the assets that originally belonged to the first borrower. Therefore, the borrower could log into his account one day only to find it had been wiped out. An honest borrower with all intentions to pay back the loan in time could find his valuable asset gone. And all this only because his creditor decided to borrow money by pledging his asset. Sadly, this whole arrangement is very much legal. The borrower, who are ordinary, hardworking people like you and me, will have to rely on the mercy of the judiciary court to recover the funds lost. Not to mention, this would be a ride in itself, involving a lot of time and money.

How to Prepare Against Rehypothecation?

Preferring Cash Accounts

Users of margin accounts with brokers are most exposed to the perils of rehypothecation. Though margin accounts may seem to offer tremendous benefits of leverage and instant liquidity, don’t be lured by them. Cash accounts require the trader to pay up the full cost of securities purchased upfront. Cash accounts have no inbuilt mechanism for margins. Therefore, the brokers’ right to pawn away our assets and borrow on their accounts is eliminated. Though a cash account requires ready liquidity at all times, this responsibility will seem very sweet when you see the money vanishing from your peer’s margin accounts.

Also Read: Hypothecation

Shorting the banking sector

Though it may seem farfetched and unnecessary, being bearish on the banking and financial sector will ensure you that when all goes wrong, you shall remain fine. The chances of the 2008 history repeating itself cannot be blown away. After all, the banks thrive on their leverage generating capabilities. And when the doom day does arrive, and the credit bubble pops, you will at least be assured of recouping your money.

Use the “Trailing Stop Loss”

The phenomenon of rehypothecation may spread a scare among the regular traders and users of brokerage accounts. This would especially be true in the case of margin account holders. However, the traders may protect their profits using a trailing stop loss. The trailing stop loss automatically keeps on upping the selling price with an upward movement in the price of the stock. Therefore, a trader will be able to convert his notional gains into actual profits sooner. The profits keep the margin requirements maintained. Also, the trader will not be required to shell out much cash each time the margin call is made.