What is Simple Interest?

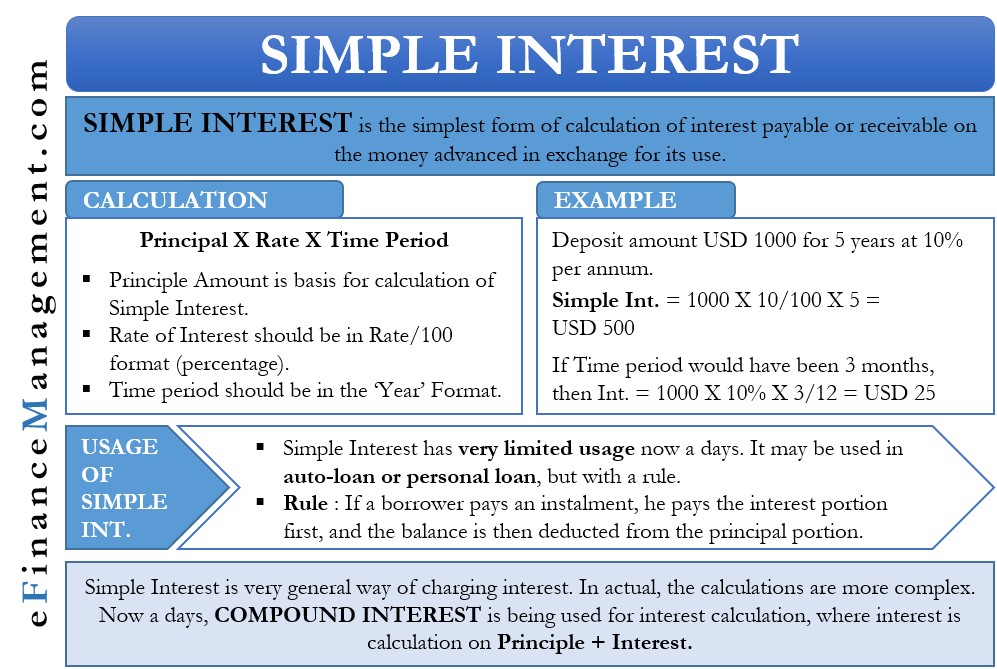

Simple interest is the simplest form of calculation of interest payable or receivable on the money advanced in exchange for its use. In simple terms, it is an amount that the borrower of money pays for its usage. It is different from a fee or a charge that may be incurred at the time of disbursal of a loan. Also, it is different from a dividend, which a company pays to its shareholders out of its profits or reserves.

A bank, financial institution, or even an individual may lend out money to someone- an individual or a firm. In such a case, it will want an additional payment over and above the actual amount or the principal that it is lending out. Interest is chargeable instead of money is given for use. Also, it acts as a motivator for lending out money and taking the risk of repayment.

A person or a firm may also earn interest by depositing money with a bank or a financial institution. In this case, he provides money to a third- party for use. Therefore, he will want to earn an interest amount on his sum invested or the principal.

Calculation of Simple Interest

The formula for calculating it is:

Principal x Rate x Time

- The principal amount is the basis for calculating simple interest and not the interest portion. Unlike compound interest, it does not add any interest portion to the principal amount for calculating interest for the next period.

- The rate of interest is to be in the format of x/100. For example, if the rate of interest is 10% per annum, we shall use 10/100= .10 for the rate of interest in the formula above. Funds are scarce in the economy. Therefore, the interest rate is charged for its usage or as a cost of capital.

- The time period in the above formula is in the “year” format. For example, we will use “5” in the formula if interest calculation for a period of 5 years. If the time period is monthly, we will have to divide the result by 12 (denoting the number of months in a year).

Example

Suppose an individual deposits US$1000 with a bank for five years at a ten %per annum rate of interest. His simple interest earnings from the deposit will be:

S.I. = 1000 x 0.10 x 5

= US$ 500.

Now let us assume that the time period in the above case is only three months. Now, the interest calculation will be as:

1000 x 0.10x 3/12

= US$ 25

Usage of Simple Interest

Simple interest has very limited usage in modern-day banking and financial activities. It may sometimes be of use in auto loans or personal loans with a very short maturity period, generally only a few months.

In instances where such interest is applicable, there is a rule. If a borrower pays an installment, he pays the interest portion first, and the balance is then deducted from the principal portion. If an installment is paid late, the interest portion gets higher as it is calculated on the number of days. The payment towards the principal amount gets lesser.

For example, suppose a person has borrowed US$1200 for one year at 10 % per annum. His interest amount will be: 1200 x .10 x 1 = US$ 120. Therefore his monthly interest amount will be 120/12= US$10. Suppose he repays US$ 110 at the end of every month to the lender. When he makes the payment of US$110 at the end of the 1st month, he is paying US$ 10 towards interest and the balance of US$100 towards Principal repayment. In case he delays his installment by 15 days, he will have to pay additional interest for 15 days which will be US$5. So next time he pays US$110, US$95 will be the principal portion, and US$ 15 will be the interest portion.

Limitations

Simple interest is a very general way of charging interest. Actual interest calculation is done using much more complex methods in the real world. Also, the most common approach is using compound interest. Where interest is calculated on due interest and the principal added together. As a result, the total interest payable or receivable is actually a lot more than in the case of simple interest. Therefore, simple interest is only a tool for the general understanding of interest calculations and has very limited application.

Read Simple and Compound Interest and Add-on Interest vs Simple Interest for a more detailed approach.