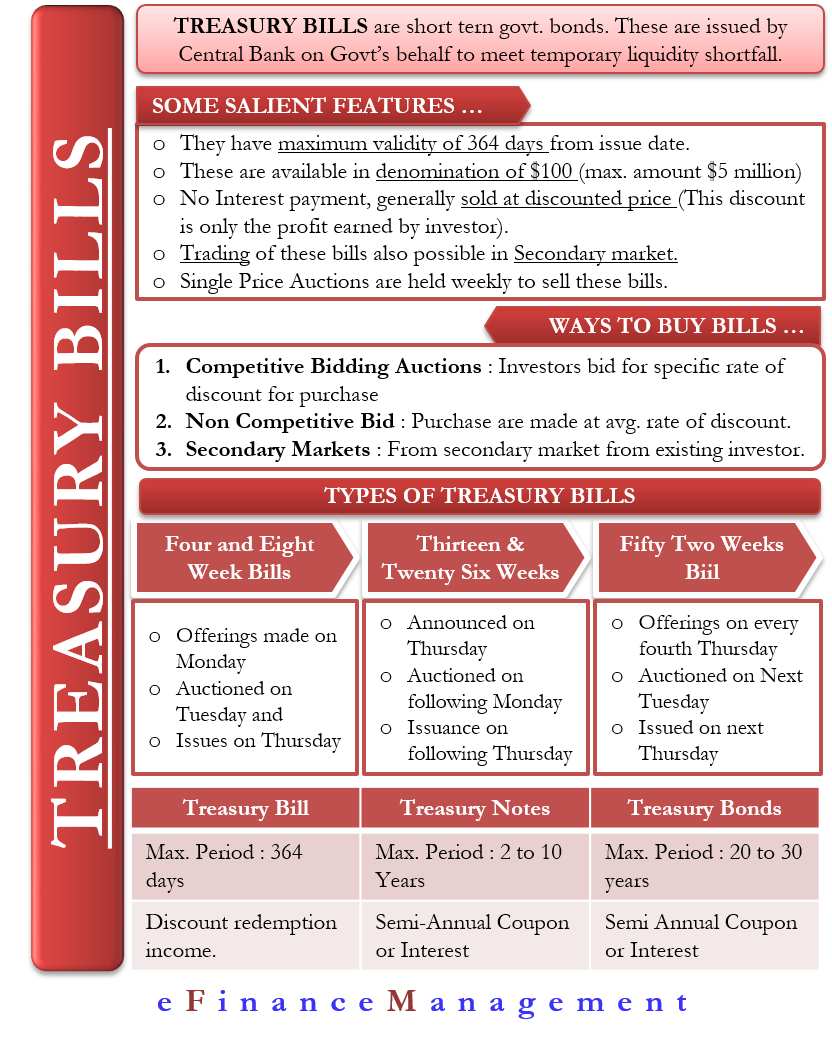

What are Treasury Bills?

Treasury Bills or T-Bills are short-term government bonds that the Central Bank issues on behalf of the government. They are risk-free because of the backing of the government. In the US, the Department of Treasury issues such Bills on behalf of the US Government. Their main purpose is to meet the temporary liquidity shortfalls of the government. They have a maximum maturity period of 364 days from the issue date. Therefore they are money market instruments and offer liquidity to the investors. There are majorly five types of Treasury Bills, categorized on the basis of their maturity periods.

Treasury Bills: How it Works with Example?

Treasury Bills are available in denominations of 100$, with a maximum amount of $5 million. They do not pay any interest and are sold at a discounted price from their par value. The longer the maturity period, the higher the discount. The difference between the purchase and sale price is the interest or profit of the investors. For example, a 1000$ T-Bill can have an issue price of 925$ for fifty-two weeks. The investor will buy it for $925 and will get back $1000 at year-end or maturity. Thus, he will make a profit of $75. This is the interest income from the Treasury Bill. In this case, $1000 is the face value of the T-Bill, and the discount rate is 7.5% of the face value.

Banks and financial institutions are the biggest customers of various types of Treasury bills. Before maturity, trading of these Bills can be done in the secondary market. Investors can thereby make short-term interest gains. Continuing with the above example of a T-Bill purchased at 925$, if the T-Bill is trading at 975$ in the secondary market after 7 months, the investor can exit the position at the prevailing rate. He will not have to wait for the entire year to sell off his investment. Also, he gets an opportunity to earn interest gain too.

Treasury Bills have a maturity period of less than a year. Hence they offer lower yields or returns than most of the other types of bonds and securities. Single-price auctions are weekly held to sell these Bills. Thus every purchaser gets to buy at the same price.

Types of Treasury Bills

The following are five types of Treasury Bills.

Four-week and Eight-week T-Bill

Four-week and eight-week Treasury bills offering amounts are announced on Monday. They are then auctioned the next day- Tuesday and issued on Thursday. The auction of both these bills takes place once a week.

Thirteen-weeks and Twenty-Six weeks T-Bill

91 days and 182 days T-Bills offerings are announced every Thursday and are auctioned on the following Monday. Settlement or issuance is made on the following Thursday. Auction of both these bills also takes place once a week.

Fifty-two weeks Treasury Bills

Auction of Fifty-two weeks or 364 days T-Bills happens every four weeks, unlike the other types of T-Bills. Their offering amounts are announced every fourth Thursday, are auctioned on the next Tuesday, and issued on the following Thursday.

Ways of Buying Treasury Bills

Competitive Bidding Auctions

Like any other auction, investors bid for a specific rate of discount at which they want to buy the Treasury bill in these auctions. Licensed Brokers or a Bank accept such bids. Bids with the lowest rates of discount are first accepted. Bids at the next lowest discount rate are accepted if the subscription is not full. This goes on until the full subscription of the issue.

Also Read: Bonds and their Types

Non-Competitive Bid

In such a bid, investors buy the T-Bill at an average discount rate determined at the auction from all the bids. Individuals can make such bids via the TreasuryDirect website in the US.

Secondary Market

Treasury bills are bought or sold in the secondary market, too, i.e., from other investors already holding the T-Bill.

Difference between Treasury Bills, Treasury Notes, and Bonds

T-Bills, T-Notes, and Bonds are all issued by the US Department of Treasury on behalf of the government to fund its debt. However, the three differ with regard to their maturity period and their interest payments.

- T-Bills have a maximum maturity period of 364 days from the date of issue. Their prices don’t fluctuate much because they mature in a very short time.

- Treasury Notes have a maturity period of two years to ten years. They make a semi-annual coupon or interest payment.

- Treasury Bonds or Long Bonds have the longest maturity period of twenty to thirty years. They also make a semi-annual coupon payment. But they have a quarterly issue. Bonds are the basis for banks’ calculation of mortgage rates. Because of their maturity period, they are riskier for the investors and hence offer the highest yield among the three.

Prices of T-Notes and T-Bonds fluctuate much more than the T-Bill because of the longer maturity period, and hence their yield remains linked to market prices. For example, a 10-year T-Note might have been issued with a yield of 10% when rates of interest were high. In the next few years, interest rates may fall, and new T-Notes may be issued with a yield of 5%. At current rates, investors will be able to buy the higher-priced T-Notes with a lower yield to maturity. In other words, their interest income will fall.

Factors affecting Treasury Bill Prices

The following factors affect T-Bill prices:

Inflation

T-Bill prices fall in times of high inflation rates and vice-versa. If the inflation rate is higher than the T-Bill return rate, the prices of the T-Bill will fall. For example, if the inflation rate is 5% and the T-Bill yield rate is 3%, an investor will have a net return loss of 2% in real terms at the time of maturity. In such times, investors will tend to go for other instruments providing higher returns, and hence, the price of T-Bills will go down.

Monetary Policy

The Prices of T-Bills go up with a fall in federal funds rates set by the monetary policy of the Federal Reserve. For example, when the Fed cuts interest rates, demand for T-Bills will go up as they become a more attractive investment avenue for the investors than other options. Hence the prices will go up with the rising demand. With a rise in the federal funds rate, the situation becomes vice-versa, and prices of T-Bills will fall.

Recession

US Treasury Department issues the T-bills, and the government fully backs them. Hence they are the safest investment option in times of recession or economic slowdown. These bills are risk-free, and therefore investors pull out money from other options and tend to invest in more of T-Bills in such times. Thus, with increased demand, prices of T-Bills go up and vice-versa.

Summary

Treasury Bills have the backing of the US Government, and hence there is no default risk. They can be bought for as low as $100 and hence are affordable. Also, in the secondary markets, they can be traded easily. But they have their own share of limitations too.

T-Bills have interest rate risk, i.e., in times of high-interest rates, they become less attractive for investors who can earn more by investing in other higher return options. They do not pay any regular interest and are not suitable for investors looking for steady cash flow and income.

They offer low rates of return but are also risk-free. Hence they are good for investors looking for a low-risk, low-return investment option.

RELATED POSTS

- Brady Bonds – Meaning, History, How it Works? and More

- Treasury STRIPS – How do they Work, Advantages & Disadvantages

- Medium Term Note: Meaning, Risk, Types, Participants, Advantages, and More

- Commercial Paper – Meaning, Features, Types and More

- Debt Market: Meaning, Issuers, Instruments, Advantages, Disadvantages, and More

- Bond Market: Meaning, Types, Strategies, Bond Indices and More

great work! thanks to the author, most of the educative information here has helped me in my MBA Finance class.

keep up the good work. ??

Sanjay Borad is the founder & CEO of eFinanceManagement. He is passionate about keeping and making things simple and easy. Running this blog since 2009 and trying to explain “Financial Management Concepts in Layman’s Terms”.