Material Cost Variance

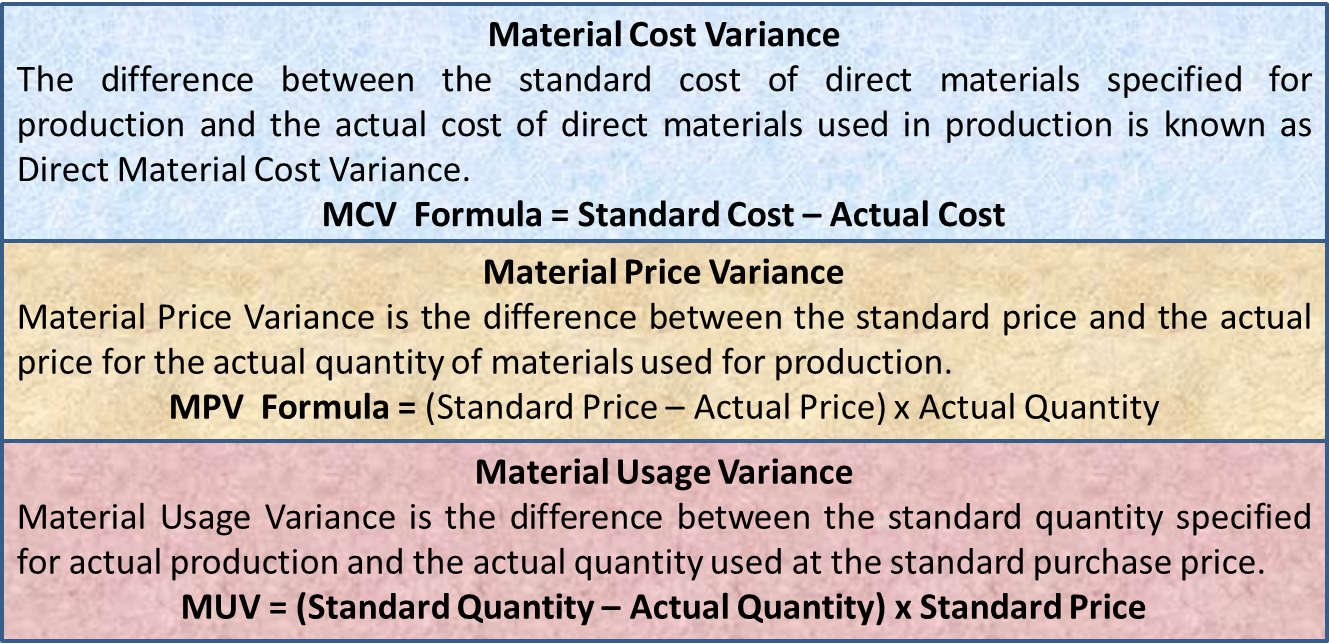

The difference between the standard cost of direct materials specified for production and the actual cost of direct materials used in production is known as direct material cost variance. Material cost variance gives an idea of how much more or less cost has been incurred when compared with the standard cost. Thus, Variance Analysis is an important tool to keep a tab on the deviations from the standard set by a company.

Material Cost Variance Formula

Formula for Material Cost Variance = Standard Cost – Actual Cost

The reason for material cost variance can be procuring material at a different price than the standard or because of a change in the quantity of material. Thus, Material Cost Variance consists of two components: Material Price Variance and Material Usage Variance.

Material Cost Variance Formula

Standard Cost – Actual Cost

In other words, (Standard Quantity x Standard Price) – (Actual Quantity x Actual Price)

= (200 x 10) – (150 x 8)

= 800 (F)

Favorable, since the actual cost is less than the standard cost. If the actual cost is more than the standard cost, the result is Adverse (A).

MCV= MPV + MUV

= 300 (F) +500 (F)

= 800 (F)

Let us first understand the meaning of Material Price Variance.

Material Price Variance

Material Price Variance is the difference between the standard price and the actual price for the actual quantity of materials used for production. The cause for material price variance can be many, including changes in prices, poor purchasing procedures, deficiencies in price negotiation, etc.

Also Read: Material Price Variance Calculator

Material Price Variance Formula

The calculation of Material Price Variance using the following formula is as follows:

MPV = (Standard Price – Actual Price) x Actual Quantity

Let us understand this formula with the help of an example.

| Standard | Actual | |

| Price | $ 10 per kg. | $ 8 per kg. |

| Quantity | 200 kgs. | 150 kgs. |

Here, the Material Price Variance can be calculated as follows:

MPV = (10 – 8) x 150

= 300 (F)

Interpretation of Material Price Variance

(F) denotes a favorable variance and (A) denotes unfavorable or adverse variance. Material price variance determines the performance of the purchasing department in procuring materials.

A favorable variance is treated as good. But there could be the other side of the coin too. It could be favorable if the material is of low quality, whereby the actual consumption may go up substantially. The lower quality material can be procured at a cheaper price which will lead to favorable price variance. But, an improvement in price variance will lead to a downfall in material usage variance if the material quality is low.

Similarly, unfavorable variance could be the result of:

- Purchasing at short notice

- Frequent purchases of small quantities and thereby losing on volume discounts

- Not being able to negotiate proper pricing, etc.

For a quick calculation, refer to Material Price Variance Calculator

Let us now understand the meaning of Material Usage Variance.

Material Usage Variance

Material Usage Variance is the difference between the standard quantity specified for actual production and the actual quantity used at the standard purchase price. There can be many reasons for material usage variance, including the use of sub-standard or defective products, pilferage, wastage, differences in material quality, etc.

Material Usage Variance Formula

MUV = (Standard Quantity – Actual Quantity) x Standard Price

With the help of the above example, let us now calculate Material Usage Variance.

MUV = (200 – 150) x 10

= 500 (F)

The result is Favorable since the standard quantity is more than the actual quantity. In cases where the actual quantity is more than the standard quantity, the result is in (A), which means Adverse.

Keep reading Direct Materials Quantity / Usage / Volume Variance

Conclusion

Material Cost Variance is composed of Material Price Variance and Material Usage Variance. This means Material Cost Variance = Material Price Variance + Material Usage Variance. We can confirm and cross-check this equation with the help of our example.

Refer to Material Yield Variance and Material Mix Variance.

Frequently Asked Questions (FAQs)

Material cost variance is the difference between the standard cost of direct material and the actual cost of direct material used in production.

MPV = (Standard Price – Actual Price) x Actual Quantity

The formula for calculating the material usage variance is:

MUV = (Standard Quantity – Actual Quantity) x Standard Price.

RELATED POSTS

- Direct Materials Quantity / Usage / Volume Variance

- Material Yield Variance – Meaning, Formula, Example, and More

- Material Mix Variance – Meaning, Example, and More

- Variance Analysis Formula with Example

- Cost Variance – Meaning, Importance, Calculation and More

- Production Volume Variance: Meaning, Formula, Limitations, and More

very good explanation

Good explanation…It is very helpful. Thank you.

Nice one

Perfercto

Here is the information given standard material for 70 kg finished product :100kg

Price of material :Re, 1per kg

Actual output 2,10,000

Material used,2,80,00

Cost of materia:Rs. 2,52,00

What is the actual quantity and standard quantity in the above information?

Every 100 Kg is giving an output of 70Kg ie. 70% is the output ratio. So standard qty should be 210000*100/70 = 300000 Kg.

Therefore, Standard Qty is 3 L Kg, whereas actual qty is 2.80 L Kgs. Hope this clarifies and meets your expectations.

it is so much good god bless you