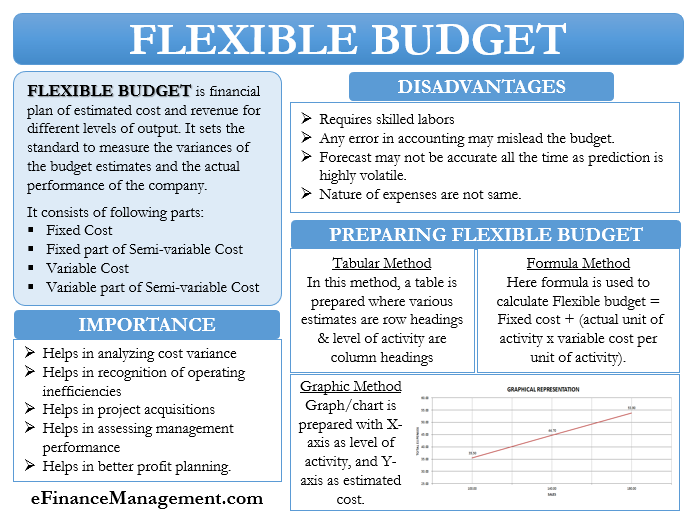

What are Flexible Budgets?

A flexible budget is a budget or financial plan of estimated cost and revenue for different output levels. The variation happens due to the change in the volume or level of activity.

It sets the standard to measure the variances of the budget estimates and the actual performance of the company for control purposes. Further, it can be prepared either for the whole company or a specific department or unit.

In brief, a flexible budget is a budget that distinguishes the behavior of fixed and variable cost that changes. And changes that happen with the level of activity attained, or change in the revenue or other variable factors.

It consists of two parts – the first is the fixed cost and the fixed cost portion of the semi-variable cost. And the second is the variable cost and variable cost portion of the semi-variable cost. A flexible budget provides cost estimates at different levels of activity. Also, a vivid classification of the expenses into different categories of fixed cost, semi-variable cost, and variable cost is necessary before preparing a budget.

Also Read: Flexible Budget Variance

Example

Let us consider firm M wants to determine the cost of electricity and supplies cost for its factory. The cost per machine hour is $10.

And its fixed cost amounts to $35,000.

Fixed cost, for example, rent, insurance premium, etc., remains the same every month, irrespective of the actual machine hour used.

The factory equipment operates on an average of 3,000 to 6000 hours per month.

Based on the above information,

Monthly flexible Budget = $35,000 + $10 per MH (Machine hour).

| Months | Machine hour |

| April | 4000 |

| May | 3500 |

Suppose the factory operates for 4,000 machine hours in April.

Therefore for the month of April — flexible Budget = $35,000 + ($10 x 4000) = $75,000

And if the factory operates for 3,500 machine hours in May.

Hence, the new flexible Budget for the month of May = $35,000 + ($10 x 3500) = $ 70,000

Therefore, we can conclude that with the change in the machine hours of the factory, the flexible budgets also change. And it helps in better financial planning and controlling.

Situations for Preferring a Flexible Budget

- If a company is labor-intensive and where labor is a crucial factor in production. For example, the jute industry, handloom industries, etc., where a worker performs a significant portion of work. Here, a flexible budget helps management determine the productivity of the labor.

- Initially, a new venture can’t predict demand for its product accurately; hence, a flexible budget can be of great help. So, it can prepare flexible budgets with different levels of output based on the analysis of the demand for a similar product.

- A company producing seasonal products can opt for a flexible budget. Here, the activity level varies from time to time, either due to its nature or variation in demand. Therefore, It makes sense to make a flexible budget.

- In the fashion industry, fashion trend changes frequently. And a flexible budget that accommodates the difference in the various components of the cost to accommodate changing trends is always preferable.

- For some ventures, the factor of production is not available all the time. Here, the level of activity varies according to their availability. In such a situation, a flexible budget is of great help in determining the level of production and budget therefor.

Importance

- Flexible budgets act as a benchmark by setting expenditures at various levels of activity. And the estimates of expenses developed via a flexible budget helps in comparing the actual cost incurred for that level of activity. Hence any variance identified helps in better planning and controlling.

- It helps establish the variability of cost factors at different levels of activity. Hence it helps in analyzing the cost variances.

- It helps in recognition of operational inefficiencies and errors. And thus, better correction and control can happen.

- It helps to set the prices and quotations for a business contract. Therefore helpful in project acquisition.

- It helps in assessing the performance of the management and key production personnel. Thus, it increases the efficiency of the employees.

- Better cost control leads to better profit planning.

Disadvantages

The flexible budget has immense importance, but it has certain disadvantages also, as listed below:

- The preparation of a flexible budget requires skilled workers. And their availability is a crucial factor in opting for a flexible budget.

- It is dependent on proper accounting disclosure. Hence, any error in books of accounts can mislead the budget preparation, and chances of flexible budget variance may increase. It is because the base of the budget starts from the past performance of the company.

- Prediction can be highly volatile as it depends upon factors of production which are beyond managerial controls. Therefore, the forecast may not be accurate all the time.

- It may be tricky to analyze the variances of cost, as the nature of all the expenses may not be the same.

- Fixed and variable cost determination happens on an arbitrary basis. Hence flexible costs are less relatable to the correct budget cost of the level of activity.

How to Prepare a Flexible Budget

There are three ways to prepare a flexible budget:

- Tabular method

- Graphic method

- The Ratio or Formula Method

Tabular Method

In this method, the budget takes a tablet form, where horizontal columns represent the different levels of activity or capacity. And the vertical rows represent the budgeted estimates against the different levels of activity or output. The expenses are categorized into fixed, variable, and semi-variable costs.

Specimen:

| Capacity | 50% | 60% | 90% |

| Sales | 100.00 | 120.00 | 180.00 |

| Fixed Expenses: | |||

| Wages | 9.00 | 9.00 | 9.00 |

| Rent, Rates, and Taxes | 6.50 | 6.50 | 6.50 |

| Depreciation | 7.50 | 7.50 | 7.50 |

| Total Fixed Costs (A) | 23.00 | 23.00 | 23.00 |

| Semi-Variable Expenses | |||

| Maintenance and Repairs | 3.00 | 3.00 | 4.20 |

| Indirect Labour | 7.20 | 7.20 | 9.44 |

| Sales Department Salaries etc. | 3.80 | 3.80 | 4.36 |

| Total Semi-Variable Expenses (B) | 14.00 | 14.00 | 18.00 |

| Profit | 63.00 | 83.00 | 139.00 |

| Total Expenses | 35.50 | 44.70 | 53.90 |

Graphic method

Graphically, X-axis represents the level of activity, and Y-axis represents the estimated cost. The chart reads out the budgeted expenses at different levels of activity and helps in performance management.

Also Read: Types of Budget

Specimen:

Formula or Ratio method

In this method, the following formula is used for calculation:

Flexible budget= Fixed cost + (actual unit of activity x variable cost per unit of activity).

We can use any of these three methods to prepare the budget. But, the method selected must serve the purpose of developing such a budget.

Read more about other Types of Budgets.