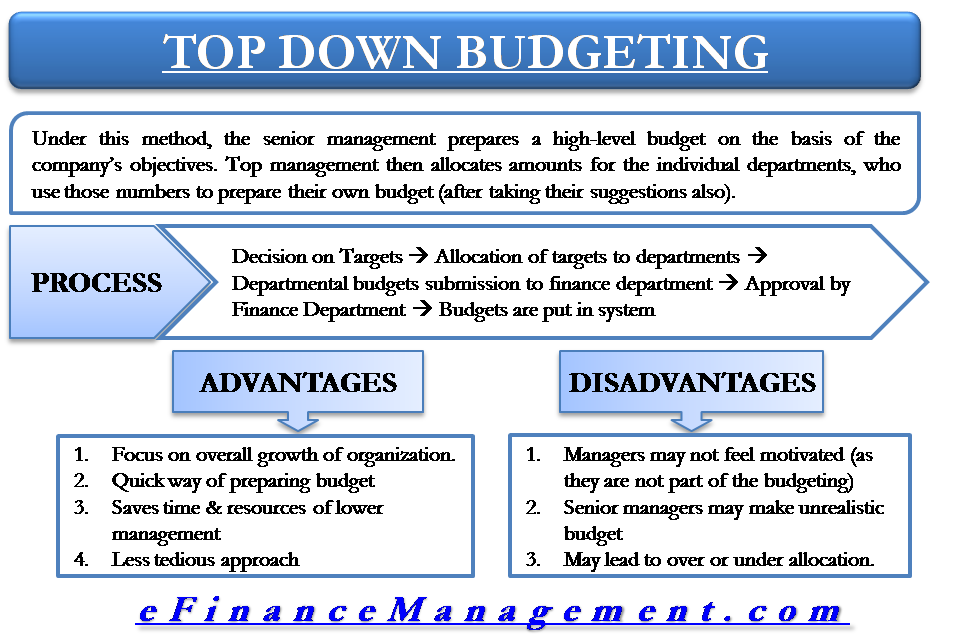

Top-down budgeting is a crucial method of preparing a budget for an organization or a company. Under this method, the senior management prepares a high-level budget on the basis of the company’s objectives. The top management then allocates the amounts for the individual departments, who use those numbers to prepare their budget.

Managers of the individual departments may give suggestions to the top management before preparing the budget. But, it is up to the top management to include those suggestions in the budget or not.

How is a Top-down Budget Prepared?

The top management uses past experiences and the current market scenario for the top-down budget, including margin pressure, competition, tax legislation, macroeconomic conditions, and more.

Also, the management uses past years’ budgets and financial statements as a reference for allocating to various departments. Additionally, senior management may also use input from lower-level managers. For instance, if any department accounted for 20% of the overall expenditure last year, then this year it would be allocated 20% of the funds. Any adjustments to these numbers will be based on the input from the managers or the current market scenario.

Process of Top-down Budgeting

The top-level management will meet to decide on the targets for sales, expenses, and profits. Next, the finance department will allocate these targets to other business departments. After this, each department prepares its budget.

Each department will then come up with a detailed budget, indicating how it will hit the revenue target and at what cost. For instance, the number of products they will sell, how much staff they will need, and more.

All such detailed budgets from the individual departments are then sent back to the finance department. The finance department then approves them if they are in line with the overall objectives of the company. The finance department may also ask for some revisions if they believe the department’s budget is deviating from the set goals.

After the finance department finalizes all the things, the budgets are put in the system. Going forward, monthly reports are generated to compare the actual results from the planned ones.

Also Read: Why are Budgets Useful in Planning Process?

Advantages

- Such type of budget focuses on the overall growth of the organization.

- It makes departments aware of what the top management expects from them.

- It is a quick way of preparing a budget and helps to overcome interdepartmental issues.

- Saves time for lower management as well. Rather than preparing the budget from scratch, each department gets a set goal. This saves both time and resources.

- Under top-down budgeting, management creates only one budget, rather than allowing the department to create their budget and combine them later. Hence, it is a less tedious approach.

Disadvantages

- Since managers are not part of the budget-making process, they may not feel much motivation to ensure their success.

- Since senior managers are not much aware of the day-to-day operations of the departments, they may set unrealistic targets. This results in lower-level managers finding it difficult to meet the set numbers.

- Such a type of budgeting may often lead to over or under-allocation of resources.

Bottom-up Budgeting

Bottom-up budgeting is also a type of budgeting, but it’s the exact opposite of top-down budgeting. The bottom-up budgeting starts at the department level and then moves up to the top management.

Under this, the departmental heads or managers create their budget and then submit it to the top management. They prepare the budget on the basis of present information and past experiences. Also, it manages to give a proper explanation for each item in the budget. The top management approves, revises, or sends it back for modifications. After top management approves all the department budgets, it comes up with a master budget.

Conclusion

Whether you should go for top-down budgeting depends on the size and structure of your business. For a smaller business with not many departments, a top-down approach is preferable as there won’t be a large disconnect between the upper and the lower-level managers. But, as your company starts to grow, it will be better to get more input from the managers of the departments.

Very helpful ❤️