Cost accounting and financial accounting are the branches of accounting. Both these deal with recording and presentation of financial information, but their objective is different. To better understand these accounting branches, we need to understand the difference between cost accounting vs. financial accounting.

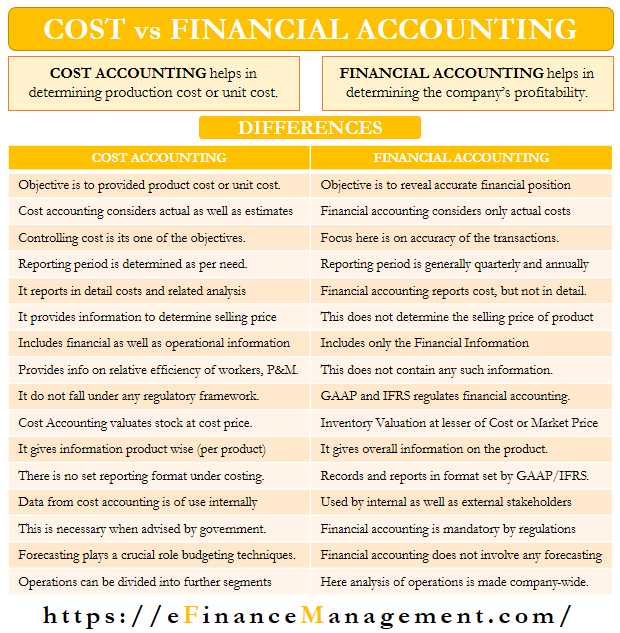

As the name suggests, cost accounting helps determine the cost of production or cost per unit. The information from cost accounting helps to keep a check on operations and maximize profit and efficiency.

On the other hand, financial accounting includes recording all financial transactions to determine the profitability of the company. It identifies the financial numbers for an accounting period and the position of assets and liabilities on the last day of that period.

Cost Accounting vs. Financial Accounting – Differences

Following are the differences between cost accounting vs. financial accounting:

Meaning

Financial accounting involves the recording of company-wide transactions. Accountants use these transactions to prepare the financial statements, which, in turn, assist in determining the profitability and financial position of a business.

Also Read: Cost Accounting and Management Accounting

On the other hand, cost accounting helps in determining the cost of the production or cost per product. It also assists in controlling the cost.

Objective

The objective of financial accounting is to reveal the accurate financial position of the company. Cost accounting aims to provide details on the cost and the cost of each unit. Management uses this information to determine the selling price of the product or service. Other objectives of cost accounting are projecting plans, making budgets, etc.

Type of Costs Used

Financial accounting considers only actual costs, i.e., actual costs and figures. Cost accounting considers actual expenses and estimates.

Recording

Financial accounting does not involve estimation but rather actual transactions. On the other hand, cost accounting includes both – recording of actual transactions and estimation of cost. To arrive at the final cost, the cost team records actual transactions and compares the cost so reached with the estimates.

Controlling

Controlling cost is one of the objectives of cost accounting. It does this with the help of costing tools such as standard costing and budgetary control. The focus of financial accounting is on the accuracy of the transactions.

Period

The period of reporting under financial accounting is usually quarterly and annually. In cost accounting, there is no period as such, and instead, it is done as per the requirement.

Reporting

Financial accounting reports cost, but not in detail. Cost accounting includes all the features of cost, including per-unit wise.

Fixing Selling Price

Cost accounting provides information that assists in determining the selling price. Financial accounting does not help in setting the selling price. Instead, it determines if the company is earning profit with the set selling price.

Report Content

A financial report includes all financial information through the accounting system. On the other hand, a cost accounting report may consist of both financial and operational data. The operational information could come from sources outside the accounting department.

Relative Efficiency

Cost accounting provides crucial information on the relative efficiency of workers, plants, and machinery. Financial accounting does not contain any such information.

Regulatory Framework

Either GAAP (generally accepted accounting principles) or IFRS (international financial reporting standards) strictly govern the structure of financial accounting reports. Cost accounting reports do not fall under any regulatory framework.

Valuation of Inventory

The financial accounting values inventory at cost or market price, whichever is lower. Under cost accounting, accountants value stock at the cost price.

Process or Tools/Statements

The financial accounting process includes journal entries, ledger, trial balance, and financial statements. Financial statements include the income statement, balance sheet, shareholders’ equity statement, and cash flow statement.

Cost accounting primarily provides for the determination of the cost of sale of product(s), the margin that the company would add, and then the selling price. It also assists in variance and break-even analysis and marginal cost calculation.

Example

If a company deals in 5 products, then financial accounting provides information on all the products in totality. Further, it puts this information under various categories, such as cost of material, direct expenses, indirect expenses, and more.

Cost accounting gives the cost information product-wise, such as cost of material, direct expenses, indirect expenses, and more for each unit. This information then helps in setting the selling price.

Format

Financial accounting records and reports the transactions in a set format to ensure uniformity in the industry/economy. They follow the format set either by GAAP (generally accepted accounting principles) or IFRS (international financial reporting standards). There is no such set format in cost accounting; companies can customize the form as per their requirement.

Users

All stakeholders, including management, owners, investors, creditors, government, and analysts, use financial statements. Data from cost accounting is of use internally, such as to the management and employees.

Mandatory

Financial accounting is mandatory, and every public company has to maintain a record of its financial transactions. Cost accounting is necessary wherever advised by the government. Manufacturing firms usually keep cost records.

Forecasting

Financial accounting does not involve any forecasting as accountants use actual figures to prepare financial statements. Forecasting plays a crucial role in some of the budgeting techniques under cost accounting.

Coverage

In cost accounting, accountants can divide operations into segments (such as geographical), division, contracts, and more. Financial accounting analyses operations company-wide.

Final Words

Both cost and financial accounting record business transactions systematically to help the management in formulating policies. Both approaches are part of the double-entry system and complement each other. Data from cost accounting helps the management to make cost control decisions. But, it lacks comparability. On the other hand, information from financial accounting is comparable but requires relevant information to make future forecasting. Thus, both are important, and we can say that financial accounting is incomplete without cost accounting data.

Also, read – Cost Accounting and Management Accounting.

I am satisfied by using this website on my studies through learning and I understand a lot of this concerning my studies.