What is the Incremental Cash Flow?

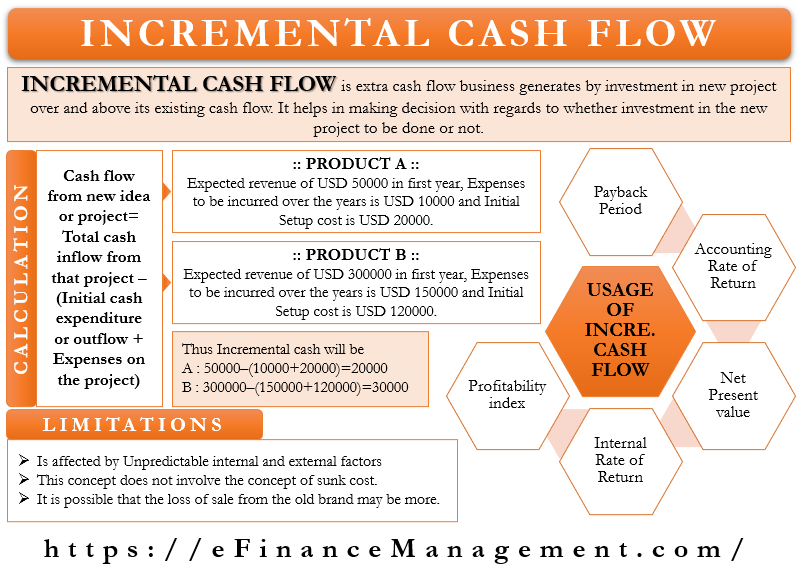

Incremental cash flow is the extra cash flow a business will generate by investment in a new project over and above its existing cash flow. It helps the company’s management to decide whether to go for the new investment or not. Calculation of the difference between the current cash flow of the company and the future cash flow of the company after investing in the new project is done. If the difference is positive and considerable, the management shall go ahead with the project. If not, they should shelve the new idea.

One thing to note is that the company cash flow to use for comparison is the net cash flow. Thus, it means that adjustments shall be made for all the additional expenditures the company will have to bear for implementing the new project. Positive cash flow is important to enable the company to meet its day-to-day cash expenses, interest expenses, taxes, buy essential assets for work, and pay for regular repairs and maintenance.

How to Calculate the Incremental Cash Flow?

Calculation of incremental cash flow is done by adding the total cash inflow from the new project under consideration. And then deducting all the initial expenditure for setting up the facilities and further operational expenses on that project.

Cash flow from the new idea or project= Total cash inflow from that project – (Initial cash expenditure or outflow + Expenses on the project)

Also Read: Net Cash Flow

This is the net cash flow the company may get by investing in this new idea or project, or facility. The decision to go ahead and make the investment or not hinges upon the quantum and time period of this cash flow.

Example of Incremental Cash Flow

Let us suppose that a company XYZ Pvt. Ltd. plans to launch a new product, “A.” The expected revenue from the product in the first year of launch is US$50000. The estimation of the expenses the company will incur on the new product over the year is US$10000. Also, the initial set-up cost for the production of the product is US$20000.

Calculation of the incremental cash flow from this new product A is:

US$50000 – (US$10000 + US$20000)

= US$20000 in the first year of launch.

Now let us assume that the company has the option of launching another product, “B.” The expectation of revenue from the product in the first year of launch is US$300000. The estimation of the expenses the company will incur on the new product over the year is US$150000. Also, the initial set-up cost for the production of the product is US$120000.

Therefore, the calculation for the incremental cash flow from this new product B will be:

US$300000 – (US$150000+ US$120000)

= US$ 30000 in the first year of launch.

Interpretation and Analysis of the Result

The incremental cash flow or net cash flow from product B is higher by US$10000, and hence, the company should opt for it according to the concept, prima facie. However, if we observe closely and in detail, we notice that product “A” is giving an incremental cash flow of US$20000 on total revenue of just US$ 50000. These figures are US$30000 on total cash inflows of US$300000 for product B. It means the ratio or percentage of net positive cash inflow for Product A is way higher than that of Product B.

Also Read: Net Cash Flow Calculator

Moreover, this net cash inflow is again on investment or cash outflow of just US$ 20000 for Product A, whereas for Product B, the net cash flow is on the investment of US$ 120000. It is again quite disproportionate. Therefore, in such situations, incremental cash flow only may not give the correct picture and may lead to wrong decisions.

Hence, it is important to use other capital budgeting techniques, too, along with incremental cash flow, to ascertain the viability of any investment or project. These techniques can be payback period, accounting rate of return, net present value, internal rate of return, a profitability index, etc.

Uses of Incremental Cash Flow

Payback Period

The payback period is the time period that a company will take to recover its investment from a particular project. The net positive cash inflow every operating year can differ and generally increases as the year goes by. Under this method, we go on adding the yearly cash flows till it becomes equal to the initial investment. And therefore, the point of this equality or the stretch of that period, expressed in terms of years, becomes the payback period.

The standard principle generally followed is the shorter the payback period of a project between the competing projects, the better and preferable it would be. Because the company will get back the initial investment at the earliest possible and to that extent probability and riskiness of the project will reduce.

Accounting Rate of Return

The accounting rate of return calculates the percentage of return a company receives from an investment or a project. Also, it does not take into account the time factor. Calculation of net income is done by subtracting various expenses from the total revenue generated from the project. This income is used to calculate the percentage return from the project.

Again, the standard principle is to prefer and go for a project with a higher return rate.

Net Present Value

Calculation of the net present value involves using the present value of cash outflows and cash inflows over a period of time. Subtraction of the present values of cash outflows is done from that of the cash inflows, and it should be positive. This method is used along with incremental cash flow to ascertain the profitability of any investment or project. This concept is an advancement over the payback period methodology.

The payback period method ignores the time value of money. This technique takes care of that. It could happen that two projects may have a similar payback period. However, the quantum of cash flow in the initial years is more say in Project A. Whereas Project B has more or less equal cash flows all the years, or Project B may have large inflows in the later years.

Therefore it is obvious and prudent to prefer Project A over Project B. However, the payback period is the same for both projects.

Internal Rate of Return

Companies use the internal rate of return to determine the feasibility of investment. It is a form of a discount rate. The net present value of all the cash flows is discounted to zero at this rate. Also, it does not include external factors like inflation, cost of capital, etc. After that, the comparison takes place between this discount rate at which the Present Values become zero with the cost of capital of the company.

And if the discount rate so obtained from the project analysis is higher than the cost of capital of the company, then the project seems acceptable.

Profitability Index

The profitability index is a financial ratio of payoff to investment amount in the case of a new project. It compares the present value of the incremental cash flow arising from a project with the investment amount. Thus, a proposed investment will be more lucrative with a high profitability index and vice-versa.

Limitations of Incremental Cash Flow

Unpredictable Internal and External Factors

The internal and external factors that can affect the incremental cash flow from a project are unpredictable. Change in internal policies and priorities of the management. And external factors like government rules and regulations, inflation, market conditions, interest rates, etc., can change anytime. These can directly affect the future cash flow calculations and hence, make the concept unreliable.

Sunk Costs and Opportunity Costs

The concept is based on future cash flows and expenditures. But it does not include sunk costs that may have already been incurred before the new project is virtually taken up. Also, it does not take into account the concept of opportunity cost. While it calculates the incremental cash flow from a new project, it does not account for the cost of the missed opportunity of investing in some other project and benefitting from it.

Cannibalization

Cannibalization is the concept of a new project or investment eating into the future cash flows of other existing projects of the same company. For example, let us take the case of the launch of a new brand of clothes by a clothing company. It may eat into the market share of its already existing brands of clothing. The incremental cash flow from the new brand may be positive. But it is possible that the loss of sales from the older brands may be more. Hence, the new project may prove to be loss-making rather than being profitable for the company.

Difficult to Identify

A company may not be able to calculate the incremental cash flows from a new product correctly in the case of companies having a wide range of product mixes. The future cash flow may be from a mix of items that will make it difficult to correctly attribute the sale to a particular product or project.

Summary

Incremental Cash Flow is an important tool for ranking or deciding between the two competing and mutually exclusive projects. The net positive cash flow from the new project is worked out and added to the existing cash flow of the company as marginal cost is the extra expense incurred for producing that extra unit. Similar way, the incremental cash flow is the additional and extra cash flow generation from the new project or investment. However, all indicators need to be interpreted and concluded upon together with other indicators and ratios. It may not give the correct picture or lead to the right decision in isolation.

Quiz on Incremental Cash Flows