What is SOFR?

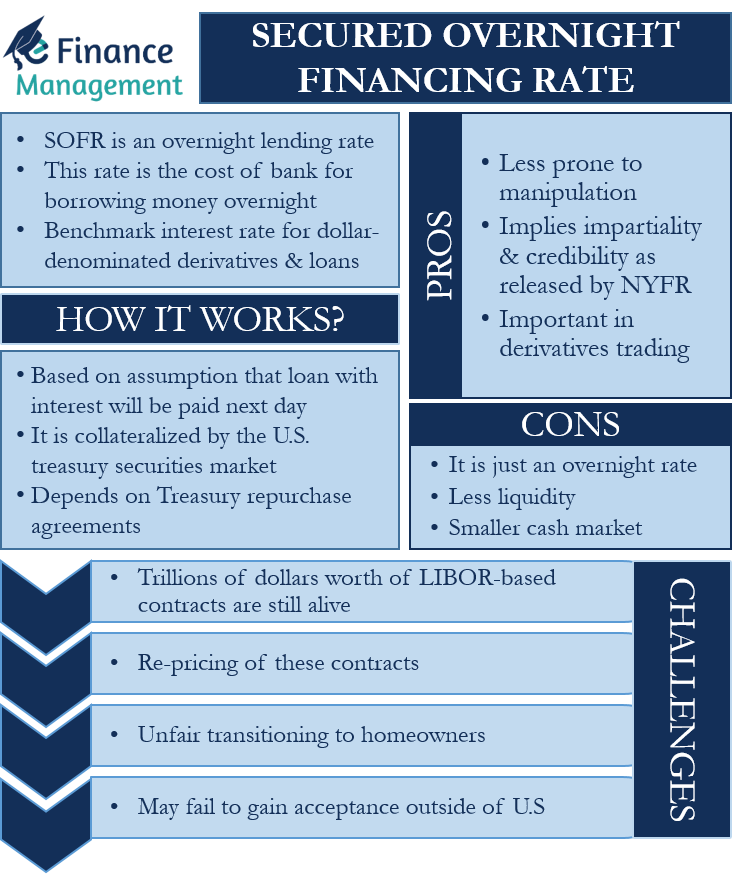

The commonly used abbreviation for Secured Overnight Financing Rate is SOFR. As the word implies, it is an overnight lending rate. In simple words, this rate is the cost of a bank for borrowing money overnight. So, it is the interest expense that the bank needs to pay to the lender. Initially, the name of this rate was the Treasuries financing rate.

Thus, SOFR is basically a benchmark interest rate for dollar-denominated derivatives and loans. Earlier, the benchmark rate was LIBOR. But following the unfair manipulation of LIBOR, banks worldwide are searching for a replacement. And these SOFR rates came into being in the year 2017. And finally, it is replacing LIBOR.

What is the Difference between SOFR and LIBOR?

So, this SOFR is a U.S. version of LIBOR or a U.S. replacement for LIBOR. The primary difference between the SOFR and LIBOR is the underlying data that they use to come up with the final rate. LIBOR is based on the estimates (borrowing rates) that banks give, while SOFR depends on the actual transactional data in the U.S. treasuries market.

SOFR calculation is based on averages of actual transaction rates. And these rates are taken from :

1. the GCF repo rate from the Depository Trust & Clearing Corporation,

2. the rate used in bilateral Treasury repo transactions cleared at the Fixed Income Clearing Corporation, and

3. the tri-party general collateral rate collected by the Bank of New York Mellon. basuca

Another key differentiation between SOFR and LIBOR is that the first one is the secured one. In contrast, the second one was the rate for unsecured borrowings, as no collateral is pledged/provided.

One more difference is that SOFR is only an overnight rate. In contrast, LIBOR is a rate available for different time frames, from overnight to up to 12 months.

How Secured Overnight Financing Rate Works?

SOFR is the rate at which a bank can get funds from other banks or individuals overnight. These loans are on the assumption that the borrowing bank would repay the loan and the SOFR interest the next day.

The U.S. Treasury securities market collateralizes the SOFR rate. These are basically the bonds that the U.S. government issues. So, to get an overnight loan, a bank pledges these securities as collateral.

SOFR depends on the Treasury repurchase agreements, which are short-term lending agreements involving collateral. The Federal Reserve Bank of New York publishes this rate daily. In practice, however, financial institutions use a rolling average of the rate so as to smooth daily volatility.

Pros and Cons of Secured Overnight Financing Rate

The benefits of a Secured Overnight Financing Rate are as below:

- SOFR is less prone to manipulation as it depends on the actual transactional data.

- The New York Federal Reserve releases the SOFR, so it implies impartiality and credibility. This is because the New York Federal Reserve is the de facto first-among-equals in the U.S. banking system.

- Such a rate is needed for derivatives trading, especially for interest rate swaps transactions.

Following are the Cons of SOFR:

- The biggest drawback of SOFR is that it is just an overnight rate. On the other hand, LIBOR serves as a benchmark to calculate the rates for different timeframes, ranging from overnight to up to twelve months.

- Presently, the liquidity in the SOFR market is less than in the LIBOR system.

- Similarly, the cash market under SOFR is also relatively smaller.

SOFR and Mortgage Rate

A SOFR is basically the rate that banks use to get overnight loans. But since it is a benchmark rate, it may impact your mortgage rate. However, whether or not it impacts your current mortgage rate depends on whether your mortgage is a fixed rate or an ARM (adjustable-rate mortgage).

In case your current mortgage is fixed-rate, then the SOFR will not have any impact on the mortgage rate of these changes. Because in a fixed-rate mortgage, these changes are ignored as the interest rate, once decided, remains fixed for the entire duration of the loan.

And, if you have an ARM, then the SOFR may impact the mortgage rate, but only if the loan term is beyond 2021. If your current debt is pegged to LIBOR and the lender searches for a replacement, then it is possible that SOFR impacts the mortgage rate (if the lender uses SOFR as the replacement).

So, if your current mortgage is on the basis of LIBOR, then it is possible that your lender will inform you soon of your new benchmark interest rate.

In addition to the current mortgage, the SOFR may also impact the debt that you may take in the future. Going ahead, as the SOFR gains more acceptance, more lenders will use it as the base rate to determine their lending rates.

So, going ahead, lenders could use it as a benchmark for ARM adjustments, as well as a base rate to set a fixed rate on the mortgages. For example, 30 day average of SOFR is already being used by Rocket Mortgage for deciding and adjusting the interest rates on their loans.

SOFR – Transition Challenges

In November 2020, the Federal Reserve noted that they would phase out LIBOR and replace it by June 2023. Also, the Federal Reserve asked banks not to use LIBOR for writing contracts after 2021. Moreover, all the contracts involving LIBOR need to be completed by June 2023.

Despite the roadmap and instructions from the Federal Reserve, it is very challenging for the financial system to migrate from LIBOR. And there are quite a few reasons for that. These reasons are:

- Trillions of dollars worth of LIBOR-based contracts are still live. And many of these contracts would mature around the LIBOR’s retirement, i.e., by 2023. For instance, about $200 trillion of debt and contracts are connected to the 3-month U.S. dollar LIBOR.

- Another challenge is to re-price these contracts. This is because of the differences between LIBOR and SOFR.

- Transitioning to SOFR could get unfair to the homeowners. For instance, in the case of an adjustable-rate mortgage, if the lenders adopt the SOFR at a time when the rate is high, it could increase the loan cost for the homeowners.

- One more challenge to the SOFR transition is that it may fail to gain acceptance outside of the U.S. This is because many major countries are evaluating their own alternative to LIBOR. For instance, the UK is using the SONIA (sterling overnight index average), ECB (European Central Bank) is opting for the EONIA (euro overnight index average), and Japan is considering the TONAR (Tokyo overnight average rate).

Final Words

SOFR, or the Secured Overnight Financing Rate, is a rate that primarily depends on the U.S. Treasury repurchases between banks. It also serves as a benchmark and is among the top contender to replace LIBOR. Since it depends on actual data, it is not susceptible to manipulation like LIBOR. However, different countries are considering their own alternative to replace LIBOR. So, only time will tell if SOFR would be able to gain acceptance outside the U.S. or not like LIBOR.