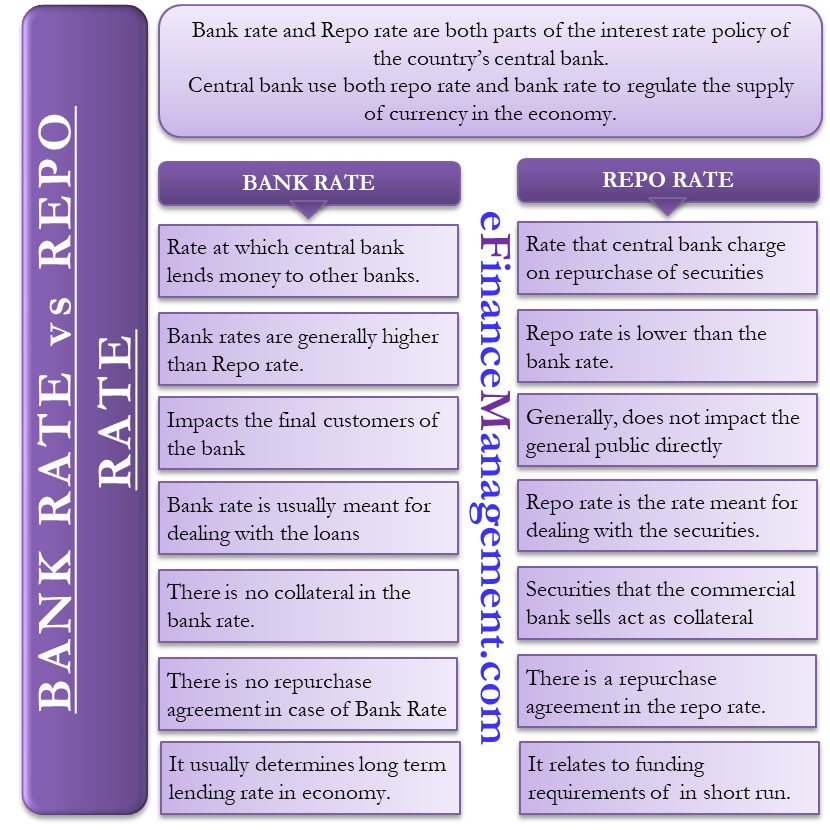

The bank rate and Repo rate are both parts of the interest rate policy of the country’s central bank. Both these rates come into use during transactions between a country’s central bank and commercial banks. The central bank uses both the repo rate and the bank rate to regulate the supply of currency in the economy. However, central banks use the repo rate more frequently in comparison to the bank rate. Though both terms serve a similar purpose and involve the same parties, they are very different from each other. To better understand the meaning, importance, and usage of both these terms, we need to see the differences between bank rate vs repo rate.

Bank Rate vs Repo Rate – What They Are

Simply put, the bank rate or sometimes known as the discount rate, is the rate at which the central bank lends money to the commercial banks. Whenever a commercial bank needs short-term money, it can borrow from the central bank at the bank rate.

The Repo rate, although slightly similar to the bank rate, comes in handy during various banking transactions such as repurchase agreements. Commercial banks sell securities to the central banks with the agreement to repurchase them after a certain period of time at a specific price. Interest that the central bank charge on the repurchase of such securities is the repo rate. The central bank usually uses repo rates to control inflation.

Bank Rate vs Repo Rate – Differences

Following are the differences between bank rate vs repo rate:

Used For

Bank rate is charged on the loan that commercial banks take from the central bank. Repo rate, on the other hand, is the rate charged on the repurchase of the securities that commercial sell to the central bank.

Interest Rate

Usually, the repo rate is lower than the bank rate. This is a conscious decision by the central bank. It is because if the bank rate is equal to the repo rate or the policy rate, the banks might simply borrow at the same rate in case the central bank penalizes them. Therefore, a meaningful spread between bank rate and repo rate is important.

Impact on Public

Since the bank rate is the interest rate at which the central bank lends money to the commercial banks, it is one of the underlying factors in deciding the interest rate at which the loan is offered to the public. On the other hand, the repo rate does not impact the consumers directly as it is handled by the banks.

Loan vs. Securities

The bank rate is usually meant to deal with the loans, whereas the repo rate is the rate for dealing with the securities.

Collateral

In the case of the repo rate, the underlying security is government security. Moreover, the securities that the commercial bank sells act as collateral as these remain with the central bank until the commercial bank repurchases them. On the other hand, there is no collateral in the bank rate.

Repurchase Agreement

There is a repurchase agreement in the repo rate. No such agreement is in the bank rate.

Impact on the Economy

Repo rate relates to the funding requirements of the commercial banks in the short run. Therefore, an increase in the repo rate generally helps in reducing the liquidity in the economy. It has no direct bearing on the customers who are looking to avail of the loan from the commercial banks. However, an increase or decrease in the bank rate directly affects the general public. The bank rate usually determines the long-term lending rate in an economy.

Long or Short Term

The bank rate deals with the long-term needs of commercial banks. Repo rate, on the other hand, addresses the short-term needs of commercial banks. The time frame in the bank rate is usually more than 28 days, while the repo rate is an overnight loan, usually for a day.

Final Words

Despite the differences between bank rate vs repo rate, the central bank, on paper, use both to control the money supply and inflation in an economy. However, the bank rate is not much in use now as banks hardly borrow from the central bank. They only approach the central bank when they are in dire need of funds.

RELATED POSTS

- Discount Rate – Meaning, Importance And More

- Monetary Policy: Meaning, Objectives, Types, Tools, and FAQs

- How is the Interest Rate related to the Required Rate of Return, Discount Rates, and Opportunity Cost?

- Types of Interest Rates

- London Interbank Offered Rate (LIBOR) – All You Need to Know

- Interest Rate is a Sum of Real Risk-Free Rate and Compensation for 4 Types of Risks