Working capital is the capital/funds required for day to day operations of the business. It is usually invested in all types of inventories, such as raw materials, spares, finished goods, etc., and credit extension to debtors and cash in hand.

Working capital is classified into different types, and the classification is based on the following views:

- Balance Sheet View

- Operating Cycle View

The balance sheet view divides working capital into gross working capital and net working capital, and the operating cycle view divides the working capital into permanent and temporary working capital. Temporary working capital is divided into seasonal and special working capital, whereas permanent working capital is divided into regular and reserve.

On the basis of Balance Sheet View, types of working capital are as below:

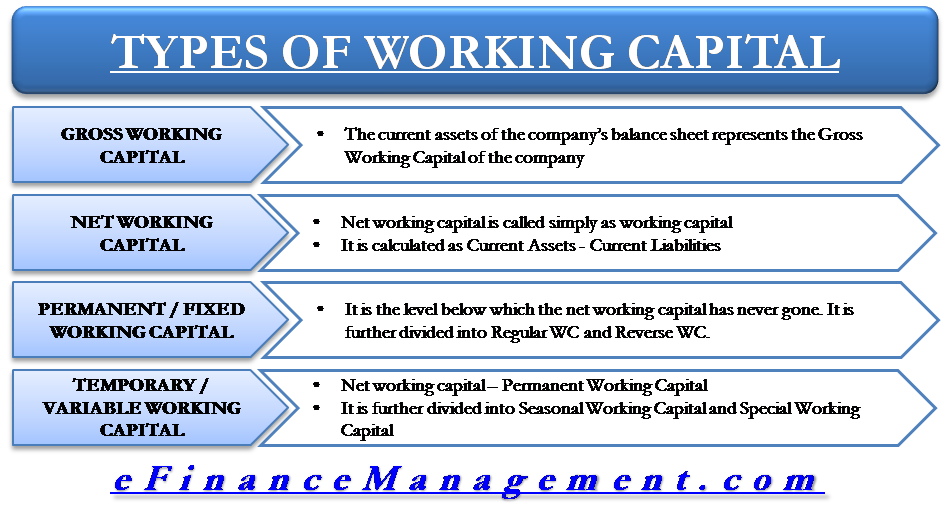

Gross Working Capital (GWC)

Current assets in the balance sheet of a company are gross working capital. Current assets are those short-term assets that can be converted into cash within one year. The grey area in managing current assets or gross working capital is its unpredictability, i.e., it is tough to ascertain the exact time of conversion of such assets.

It is because the liabilities occur at their time and do not wait for our current assets to realize. This mismatch or gap creates a need for arranging working capital financing.

Also Read: Permanent or Fixed Working Capital

Net Working Capital (NWC)

Net working capital is a very frequent term that we use in our life. There are two ways to understand net working capital. First, one says it is simply the difference between current assets and current liabilities on the balance sheet of a business. The other understanding discloses the little deeper or hidden meaning of the term. As per that, NWC is that part of current assets which are indirectly financed by long-term assets. Net working capital is considered more relevant for effective working capital financing and management than gross working capital.

On the basis of the Operating Cycle View, types of working capital are as below:

Permanent / Fixed Working Capital

Dealing with current assets and fixed assets is different. Determining the financing requirement in the case of fixed assets is simply the asset’s cost. The same is not true for current assets because the value of current assets is constantly changing, and it is difficult to forecast that value at any point in time accurately. To simplify the complexity to some extent, on the basis of past trends and experiences, we can find a level below which the current asset has never gone. The current assets below this level are permanent or fixed working capital. See the example below:

| Net Working Capital | Permanent / Fixed Working Capital | Temporary / Variable Working Capital Requirement |

|---|---|---|

| 3000 | 2500 | 500 |

| 2500 | 2500 | 0 |

| 2800 | 2500 | 300 |

| 3200 | 2500 | 700 |

In the example, 2500 is the permanent working capital below which the net working capital has not gone.

Regular Working Capital

It is the permanent working capital that the company normally requires in the normal course of business for the working capital cycle to flow smoothly.

Reserve Working Capital

It is the working capital available over and above the regular working capital. The company keeps it for contingencies that may arise due to unexpected situations.

Also Read: Working Capital

Temporary / Variable WC

Temporary working capital is easy to understand after getting hold of the permanent working capital. In simple terms, it is the difference between net working capital and permanent working capital. The main characteristic which can be made out of the example is “fluctuation.” Therefore, we cannot forecast the temporary working capital. In the interest of measurability, the further bifurcation can be as below, which can create at least some base to forecast.

Seasonal Working Capital

Seasonal working capital is a temporary increase in working capital that is a result of some relevant season for the business. It is applicable to businesses having the impact of seasons, for example, the manufacturer of sweaters for whom the relevant season is the winter. Normally, their working capital requirement would increase in that season due to higher sales in that period and then go down as the collection from debtors is more than sales.

Special Working Capital

Special working capital is that rise in the temporary working capital which occurs due to a special event that otherwise normally does not take place. It has no basis to forecast and has rare occurrences normally. For example, in a country there is an Olympic Games, all the businesses will require extra working capital due to a sudden rise in business activity.

Positive Working Capital

It refers to the excess of current assets over current liabilities. A positive working capital reflects a good liquidity position of the company.

Negative Working Capital

It is exactly the opposite of positive working capital. Negative working capital represents the excess current liabilities in comparison with the current assets.

Net Operating Working Capital

Net operating working capital only takes into account operational current assets and current liabilities.

Zero Working Capital

Zero working capital is the level of working capital where current assets are equal to current liabilities.

It was all about the types of working capital and how one should manage with several working capital techniques so as to have effective working capital management.

Quiz on Types of Working Capital – Gross and Net, Temporary and Permanent

This quiz will help you to take a quick test of what you have read here.

excellent work

Good work

Nice work

Thanks for advancing understanding on financing concepts in easy to understand language

I believe that working capital is very important for business. Thanks for sharing this article. This is very helpful for me to understand the different types of working capital.

Thank you for sharing.