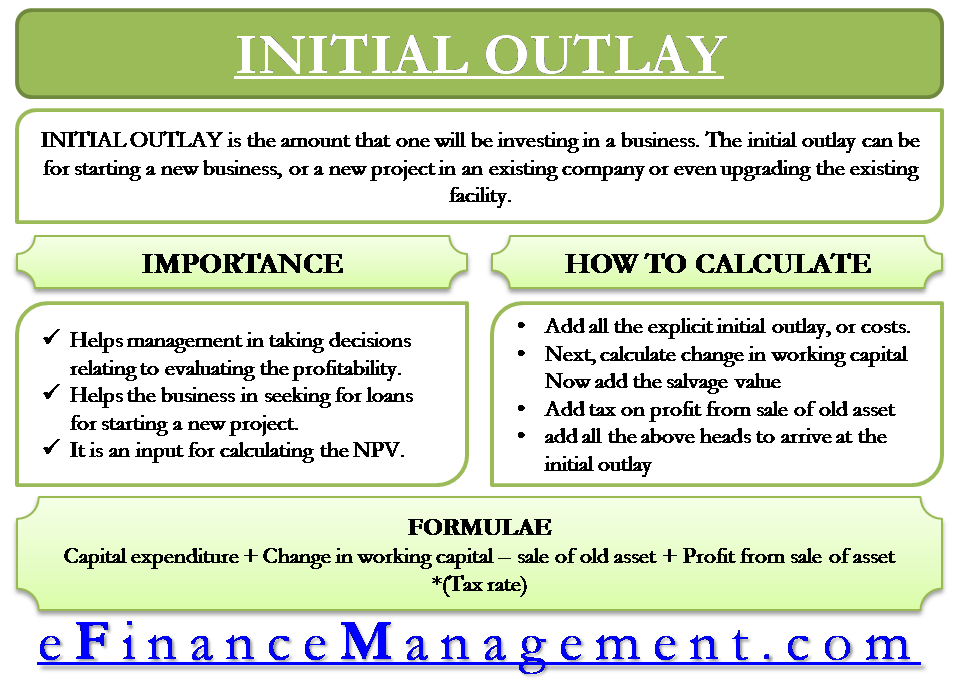

What is Initial Outlay?

Before one starts a business, it is important to know the amount that one will be investing in it. This initial amount is the initial outlay or initial investment outlay or just initial investment. The initial outlay can be for starting a new business, a new project in an existing company, or even upgrading the existing facility.

Though it is virtually impossible to estimate all the costs of starting a business, one can easily estimate some basic costs, such as equipment, materials, labor, and insurance. These costs together constitute an initial outlay.

Importance

- Management usually makes a decision to proceed with a particular project after evaluating its profitability. For this, the company needs to consider the initial outlay of the project along with its revenue stream.

- If a business is seeking a loan for starting a new project, then lenders would want an estimate of initial investment along with the business plan.

- An initial outlay is also an input for calculating NPV (net present value) and IRR (internal rate of return).

How to Calculate Initial Outlay?

In order to calculate initial outlay or initial cash outflows, consider the following steps:

Steps to Calculate Initial Outlay

- Add all the explicit initial outlay or costs. Such items directly relate to the investment or expansion of a project—for example, the cost of equipment, its shipping cost, fees, and installation costs.

- Next, calculate the change in the working capital due to the project. For instance, a business may have to adjust accounts receivable and payable because of undertaking the project. Also, a business may need to adjust inventory for raw materials depending on the project.

- Now add the salvage value (if any) for the old equipment.

- Tax on profit from the sale of the old asset must be added back.

- Now add all the above heads to arrive at the initial outlay.

Formula

Initial investment equals capital expenditures or fixed capital investment (such as machinery, tools, shipment and installation, more). A change in working capital is adjusted with this capital expenditure. Proceed from the sale of old assets is deducted, plus tax adjusted profit or loss from the sale of assets.

Thus, initial outlay = Capital expenditure + Change in working capital – sale of old asset+ Profit from sale of asset *(Tax rate)

Before moving on to the calculation, let’s understand each of these items in detail:

Total Capital Expenditure

Enter the amount required for creating or purchasing those capital assets. Such investment is the need by the company to execute the planned projects. Continuing with the above example, to begin the manufacturing of new product X, the company would require two new machines, Y and Z. The amount to be spent by the company on both the machines to bring them into working status will constitute its capital expenditure.

Also Read: Initial Outlay Calculator

Change in Working Capital

Any increase in working capital means more funds to be invested in it. Hence, the initial outlay increases. While any decrease in working capital means the company can free up such decreased cash resources from working capital. And this is already available with the company. Hence the same needs to be deducted in order to calculate the amount required for the initial investment. For a new company, it is the quantum of working capital margin that needs to be added to know the total initial outlay.

Realization from Sale of Old Asset

Any amount realized from selling an old asset reduces the amount of initial investment. Assume that machine Z required by the company is already there with the company. But it might have depreciated to its full capacity due to continuous wear and tear. In this case, the company will sell the old machine and buy a new one. Hence, such an amount from selling the old machine will get invested back in buying a new machine, and its cost gets reduced by such amount for the company.

Tax on Profit from Sale of Old Asset

If the company earns any profit by selling such an old asset, then the company usually needs to pay taxes on capital gains so earned. This amount increases the requirement of investment, as the cash flow from sales will stand reduced to that extent. Hence the amount of tax payable is added to the calculation. And, if the company incurs a loss by selling such an asset, the tax amount on such loss will get deducted from the calculation as the company will get tax relief of that much amount. For this, we simply have to enter the book value and tax rate. The initial outlay calculator will itself calculate the tax payment and will adjust the final amount accordingly.

Example

Suppose a company Alpha is planning to set up its two new outlets in two different cities – Say, City A & City B. The company will require investment in furniture worth $80,000 in each City. And the remaining capital expenditure (excluding investment in furniture) is $450,000 in city A and $270,000 in city B. Further, the company is planning to sell one of its old buildings for $220,000 (book value of $210,000). The requirement of working capital will increase by $40,000. And the tax rate on capital gain is 30%.

Also Read: Incremental Cash Flows

Initial Outlay = 880,000 + 40,000 -220,000 + 3000 = 703,000

Where total capital expenditure will be:

| Particulars | Amount |

|---|---|

| Investment in furniture | 160,000 (i.e., 80,000*2) |

| In city A | 450,000 |

| In city B | 270,000 |

| Total | 880,000 |

Tax on profit of sale of building:

Profit = 220,000 – 210,000 = 10,000

Tax = 10,000*30% = 3,000

You can also use our calculator for a quick calculation – Initial Outlay Calculator.

One can use this initial outlay for calculating the NPV (net present value) or even the IRR (internal rate of return for a project). Calculating these two will give management a better view of whether or not to undertake the project.

Quiz on Initial Outlay