Economic value added is a concept defined to measure the performance of a firm’s management in creating value or wealth for the shareholders. We can calculate it using a simple formula. Here the cost of capital is deducted from NOPAT. This is also known as economic profit or residual profit. It also has various advantages and disadvantages of EVA as a performance metric.

Economic value added (EVA) is a theory developed and trademarked by Stern Steward and Co. According to the model of EVA, a firm should also deduct the cost of equity capital from the accounting profits to arrive at a value which is the actual wealth for the investors.

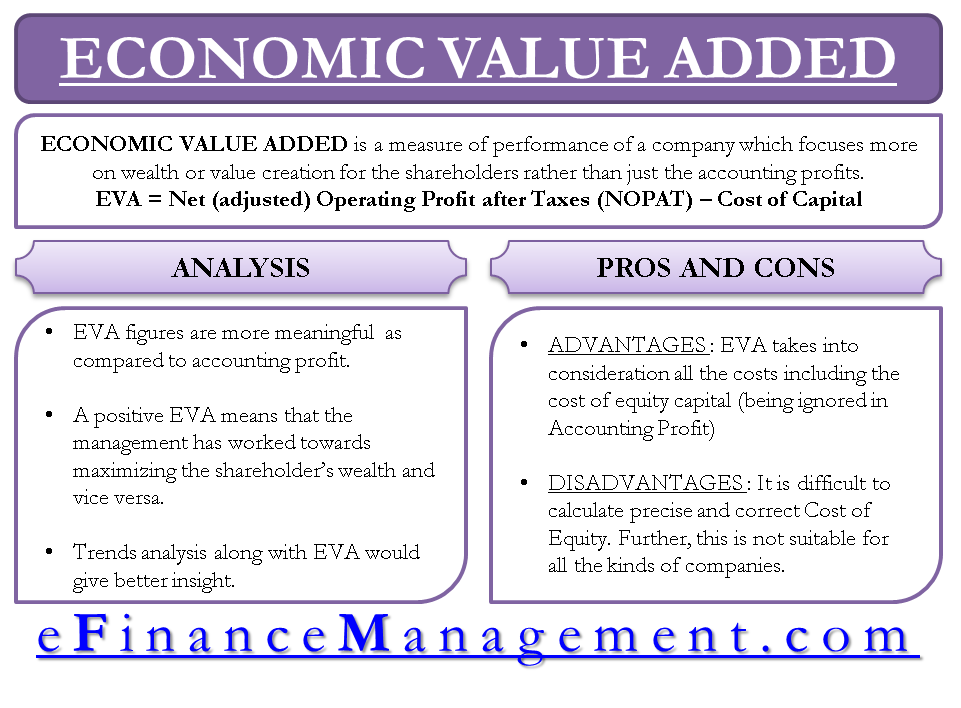

Economic Value Added Definition

It can be defined as a measure of a company’s performance that focuses more on wealth or value creation for the shareholders rather than just the accounting profits. For finding real profits that a firm has earned, all the costs are deducted from the revenues made, and similarly, the cost of using capital should also be deducted, whether it is debt or equity.

– The Measure of Real Wealth Creation")

An accountant explicitly deducts the cost of debt, i.e., interest from the revenues but does not consider the cost of equity. So, positive accounting profit does not mean wealth/value creation, but positive EVA would mean that the company’s management has done well and has created wealth for their shareholders. In that perspective, it gives tough competition to metrics like ROCE and ROI.

Also Read: MVA vs EVA

Calculation of Economic Value Added with its Formula:

One can use the formula/equation of EVA for calculating the EVA of a firm:

EVA = Net (adjusted) Operating Profit after Taxes (NOPAT) – Cost of Capital

NOPAT: It stands for net operating profit after taxes. NOPAT is the profit before charging any cost for the capital employed. It also does not include the cost of debt. An explanation of calculations is below with an example.

NOPAT Calculations:

| Revenues | 2000 |

| Less: Cost of Goods Sold | 900 |

| Less: Selling, Distribution, and Administrative Expenses | 300 |

| Less: Depreciation | 200 |

| Less: Other Operating Expenses | 200 |

| Operating Income | 400 |

| Income Taxes | 160 |

| NOPAT | 240 |

The cost of Capital: Here, the cost of capital is the weighted average cost of capital (WACC).

Economic Value Added Analysis

In comparison to the net profits calculated in normal accounting, EVA figures are more meaningful. An investor can easily understand by looking at the EVA whether he has earned more than his opportunity cost of capital or not and conclude about his investment decision is good or bad. A positive EVA means that the management has worked towards maximizing the shareholder’s wealth and vice versa.

Not only the positive EVA is enough, but the trend must also be visible. If the EVA of a firm is declining over a while, it may even go negative in the coming future. Such trends would give better insight and not stand alone EVA figures.

Economic Value Added Advantages and Disadvantages

The main advantage of using EVA as a metric for performance appraisal is that it considers all the costs, including the cost of equity capital which we ignore in normal accounting. This EVA Model helps in determining economic profit.

Also Read: EBITDA

The disadvantage is the practicability of the calculations. The first difficulty is in finding the correct cost of equity. It is not suitable for all kinds of companies. It may not correctly understand efficiency as the EVA of a giant plant will always be more than a smaller plant even when they are more efficient and maintain a better ROI comparatively.

Refer to the article MVA vs EVA for understanding the difference between market value-added and economic value-added.

To know more, you can visit our article Accounting Profit vs Economic Profit.