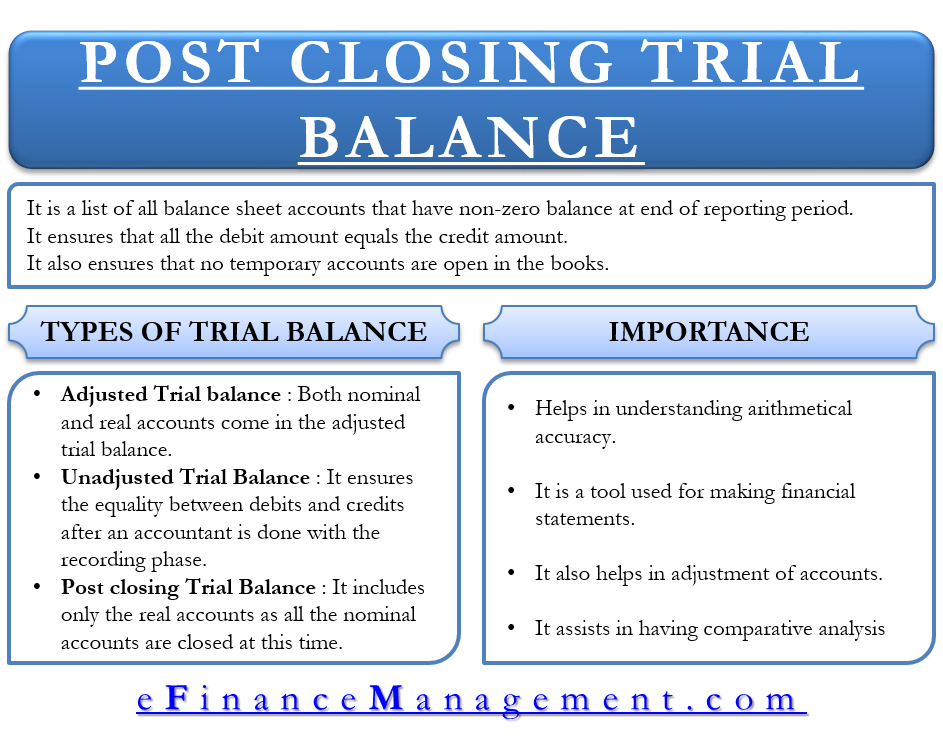

A Post-closing Trial Balance lists all the balance sheet accounts with a non-zero balance at the end of a reporting period. Hence, Companies use this tool to ensure that all debit balances are equal to the total of all credit balances after an accountant passes closing entries. So, It is the last step in the accounting cycle.

The post-closing trial balance ensures there are no temporary accounts remaining open, and all debit balance is equal to all credit balances. Also, it determines if there are any balances in the permanent accounts after passing the closing entries. As closing entries close all the temporary ledger accounts, the trial balance (post-closing) includes permanent ledger accounts, or we can say balance sheet accounts.

This trial balance does not include any gain, loss, or summary accounts balance as these are temporary accounts, and the balances in these accounts move to the retained earnings account.

Types of Trial Balance

There are three types of trial balance – Post-closing, Unadjusted, and Adjusted Trial Balance. Then, let’s understand the difference between them.

Adjusted Trial Balance

Both nominal and real accounts come in the adjusted trial balance. For instance, Nominal accounts are the ones that have entries from the income statement, and real accounts consist of entries from the balance sheet. An accountant prepares this trial balance after passing the adjusting entries. Its purpose is to test the equality of debits and credits after the adjusting entries. It also serves as the basis for preparing the financial statement.

Unadjusted Trial Balance

Accountants in the company prepare the unadjusted trial balance after entries are made in the journal and ledger. It ensures the equality between debits and credits after an accountant is done with the recording phase.

A simple difference between adjusted and unadjusted trial balances is the amounts in the adjusting entries. Few entries that are marked as the major cause of difference between adjusted and unadjusted trial balance entries are – accrual expenses; payment deferral in the balance sheet until the company recognizes it as an expense in the future accounting period; accrued revenues; deferred receipt to the balance sheet until the company earns it in the future accounting period; adjustments made in the previous deferrals that are now available in the income statement.

Post-closing Trial Balance

The purpose of the post-closing trial balance is to check the debits and the credits once the accountant passes the closing entries for the transaction. It includes only the real accounts, as all the nominal accounts are closed at this time.

In all three types of trial balance, the net balance is zero, i.e., all the debit balances are equal to all credit balances. Once an accountant determines the zero balance test (debit less credit equals zero), it means there are no further transactions for the old accounting period. Therefore, any new transaction must be for the next accounting period.

Also Read: Trial Balance

Example and Format of Post-closing Trial Balance

The format for the post-closing trial balance is similar to other trial balances. It includes account number, account description, debits, and credits.

XYZ Company Trial Balance as on June 30, 20xx

| Account Number | Description | Debit | Credit |

| 100 | Cash | $105,500 | |

| 150 | Account Receivables | 320,000 | |

| 200 | Inventory | 500,500 | |

| 250 | Fixed Assets | 2,000,000 | |

| 300 | Account depreciated | (480,000) | |

| 350 |

Accounts Payable | $195,000 | |

| 400 | Accrued Expense | $108,500 | |

| 450 | Retained earnings | 642,500 | |

| 500 | Common Stock | 1,500 | |

| Totals | $2,446,000 | $2,446,000 |

Balance Sheet vs. Post-closing Trial Balance

It is known that the total on the balance sheet is not the same as the post-closing trial balance. So, This difference is primarily because of contra accounts. For instance, the account Accumulated Depreciation will have a credit balance and would come in the credit column of the trial balance. Hence, an accountant adds the credit balance in this to other credit balances, the majority of which are liability accounts and owner or stockholder equity accounts.

On the balance sheet, the credit balance in the Accumulated Depreciation does not come with the other credit balances. Instead, the credit balance in accumulated depreciation will be a deduction from the debit balance in the asset section (property, plant, and equipment).

Significance of Post-closing Trial Balance

- A trial balance helps in understanding and verifying arithmetical accuracy. As soon as the numbers of records are transferred across accounts, checking the figures becomes extremely important.

- A trial balance also comes in handy to preparing the financial statement. A company needs to prepare a Profit & Loss, Balance Sheet, and Cash Flow statement at the end of each accounting period. Since the balances of all the ledger accounts are there in the trial balance. So, it makes it easier to prepare the financial statements.

- Having an up-to-date post-closing trial balance also helps in the adjustment of the accounts. Some examples are outstanding liabilities, prepaid expenses, closing stocks, etc.

- Another important aspect of the post-closing trial balance is that it assists in having comparative analysis, such as the current year with the past year or peer analysis. In addition, this helps the organizations have an important understanding of the decisions they need to make regarding various metrics such as income, expenses, production costs, and so on.