Revaluation of long-lived assets is an important technique in finance that is used to figure out the true value of the assets owned by the firm. Long-lived assets are divided into three categories viz. tangible assets like property, equipment, plant, etc.; identifiable intangible assets like license, trademark, or patent and non-identifiable intangible assets like goodwill of the company.

Definition of Revaluation

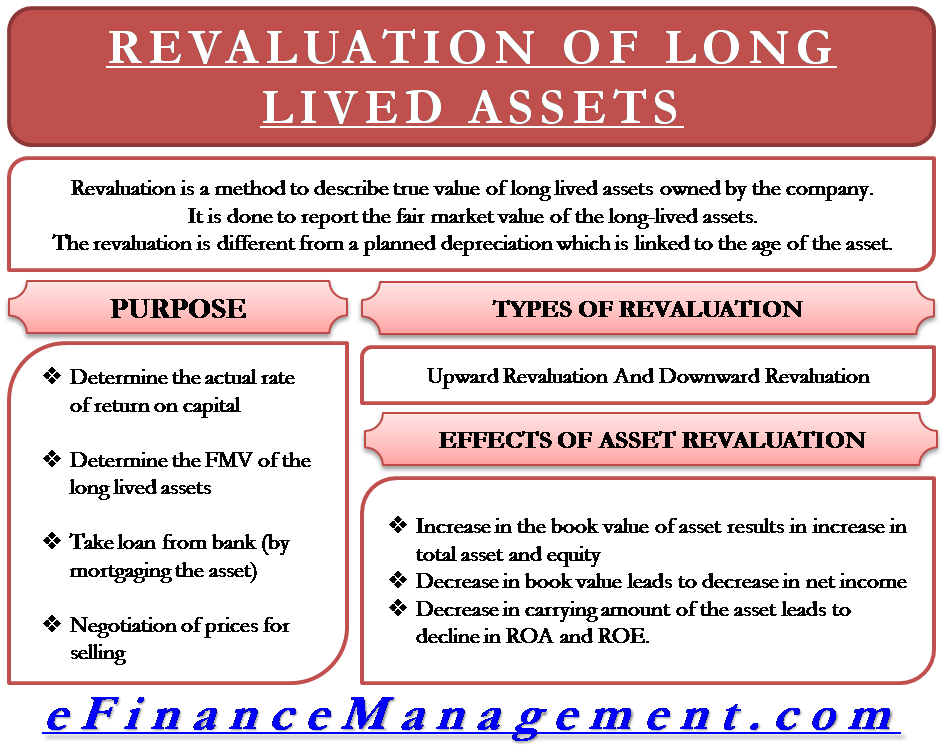

Revaluation is a method to describe the true value of assets owned by the company. The revaluation of long-lived assets is allowed only in IFRS and not in GAAP. It is done to report the fair market value of the long-lived assets. The revaluation is different from a planned depreciation which is linked to the age of the asset. Even if a firm is looking at reselling its asset, the asset is revalued for the negotiation.

Under U.S. GAAP, the historical cost model reports long-lived assets. Accumulated depreciation and an impairment loss are deducted from historical costs to figure out the value of the assets. Under IFRS, both the historical cost model and revaluation model are used. Under the revaluation model, accumulated depreciation and impairment are deducted from the fair value to report the value of the assets.

Purpose for Revaluation

Any company going for the revaluation of its long-lived assets may have one of the following reasons:

- To determine the actual rate of return on capital.

- For determination of the fair market value of long-lived assets after a huge appreciation since their initial purchase.

- To take a loan from a bank by mortgaging the asset. A correct revaluation may lead to a higher loan amount.

- To negotiate the proper price for the asset in case of any merger or acquisition by another company.

Downward Revaluation

A downward revaluation of asset results in a decrease in the book value of an asset. This decrease or loss is reported in the income statement initially. Subsequently, suppose the carrying amount of the asset increases due to an increase in the fair market value. In that case, the increase is reported as profit in the income statement, but only to the extent of the amount of loss reported previously for the asset. The remaining amount of gain due to revaluation bypasses the income statement and is reported in shareholder’s equity as other comprehensive income.

Also Read: Revaluation of Fixed Assets

Upward Revaluation

An upward revaluation of assets increases the carrying amount of the asset. Unlike the treatment in the downward revaluation, this initial profit is not recognized in the income statement. It is reported in the shareholder’s equity under other comprehensive income as a revaluation surplus. Thus, this upward revaluation increases shareholder equity and decreases net income due to higher depreciation. As a result, there is a decrease in ROE, ROA, and debt/capital ratio. Subsequently, suppose there is a decrease in the fair value of the asset, and it results in a decrease in the book value of the asset. In that case, this loss due to revaluation will be first reported in other comprehensive income, but only to the extent of the amount of previous gain. The remaining loss is recognized in the income statement.

If an asset is disposed off or retired, the surplus amount is recognized directly under retained earnings.

Effects of Asset Revaluation

The revaluation of long-lived assets affects all the financial statements in the following ways:

- An increase in the book value of the asset results in an increase in total assets and equity and, in turn, reduces leverage.

- The decrease in the book value of the asset reduces net income.

- The decrease in the carrying amount results in a decline in ROA and ROE in the particular year.

- However, in the downward revaluation scenario, the profitability appears to increase in future years because of lower total assets and equity.

- Similarly, any reversal of downward revaluation of assets also experiences an increase in earnings.

Conclusion

The revaluation of fixed assets is an important accounting decision in the firm as it impacts various financial statements. Though it is not allowed under U.S. GAAP, the companies following IFRS should undergo the revaluation diligently.