Capitalizing versus expensing different costs during the accounting of long-lived assets will have an effect on the company’s profitability, financial ratios, and trends. Both IFRS and U.S.GAAP have several rules to determine whether an expenditure is an asset or an expense. Although operationally, both are similar, a minor difference can create an everlasting impact on various financial parameters of the company.

Capitalizing Versus Expensing Costs

Expenditure is either capitalized as a cost of the asset on the company’s balance sheet, or it is expensed in the income statement of the incurred period. Under IFRS, the following rules govern the categorization of the expenditure as an asset:

- If the expenditure is expected to give economic benefits in the future over several accounting periods.

- If one can measure the cost reliably.

U.S.GAAP also follows similar rules.

Effect of Capitalizing Costs

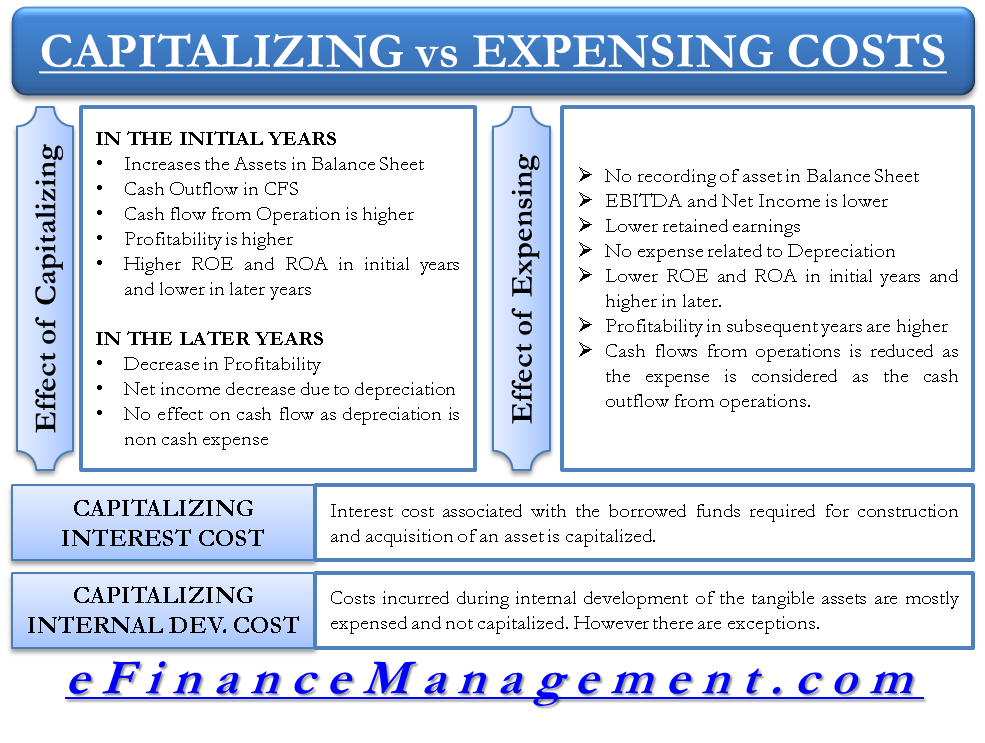

When an expenditure is capitalized, it affects the financial statements in the following ways in the period incurred:

- Increases the assets on the company’s balance sheet.

- Recorded on the cash flow statement as a cash outflow for investing.

- Cash flow from operations is higher.

- The profitability is higher in this case than expensing the expenditure in the first year.

- The shareholder’s equity is also higher as compared to expensing initially.

- Higher ROE and ROA for initial years.

- Lower ROE and ROA in later years as depreciation expense reduces net income.

- This effect of an increase in the profitability due to capitalizing continues till the capital expenditure is more than the depreciation expense.

In the later periods, the effect is as follows:

- The capitalized amount is distributed over the asset’s useful life as a depreciation/ amortization expense.

- Net income and the asset’s value are reduced due to the depreciation expense.

- There is no effect on the statement of cash flows as depreciation is a non-cash expense.

- Decrease in profitability.

Effect of Expensing Costs

When any expenditure is categorized as an expense, it affects the financial statements in the following ways in the period incurred:

- No recording of the asset on the balance sheet.

- EBITDA and Net Income (NI) are lower.

- The lower net income translates into lower retained earnings.

- Cash flows from operations are reduced as the expense is considered the cash outflow from operations.

- No expense related to depreciation/amortization in later periods.

- The profitability in the first year is lower than capitalizing the expense.

- Lower ROE and ROA initially but increases in later years.

- The profitability in subsequent periods is higher than the capitalizing of expenses.

- Results in increased market multiples which might make the company’s share look overvalued.

- This calls for adjusting the market-based multiples for capitalizing on having better comparisons.

Capitalizing Interest Costs

Interest cost is the cost associated with borrowed funds required for constructing and acquiring an asset that requires a very long duration of time to be ready for its planned use. Generally, the interest costs are capitalized. One can take the existing rate on borrowings or the rate that is actually incurred for the interest rate that needs to be capitalized. The recording of capitalized interest varies depending on the intended use of the asset:

- Asset for company’s captive use: In this case, the capitalized interest is recorded as a part of the asset on the company’s balance sheet. It is further expensed as a part of the depreciation expense over the asset’s useful life.

- For selling: In this case, the capitalized interest is recorded as a part of the inventory on the company’s balance sheet. It is later expensed as part of COGS (cost of goods sold) post the asset’s sale.

It is imperative that both the expensed and capitalized part of interest expenditure be considered to calculate interest coverage ratios.

Capitalizing Internal Development Costs

Costs incurred during the internal development of the tangible assets are mostly expensed and not capitalized. However, there are a few exceptions to this rule:

Also Read: Capital Expenditure

- Under IFRS, the research expenditures are treated as expenses while the development expenditures are capitalized as an asset.

- Under U.S.GAAP, both research and development costs are supposed to be expensed. However, some costs incurred in software development should be capitalized.

Expensing the internal developing costs instead of capitalizing results in lower NI in the incurred period. It is also treated as an outflow from operating cash flows.

Effect on Financial Statements

The capitalizing and expensing of the expenses have different effects on the financial elements of the company as follows:

- Total assets, shareholder’s equity, net income in the first year, operating cash flows, and interest coverage in the first year are higher in capitalizing than those in expensing.

- Income variability, net income in later years, investing cash flows, interest coverage in the subsequent periods, debt ratio, and debt-to-equity ratio are lower in capitalizing than those in expensing.

Conclusion

Expensing an expenditure lowers the current profitability but enhances the trend in later years, whereas capitalizing increases the current profits. However, the total NI remains the same under both techniques. Since both capitalizing and expensing have different effects on the financial statements, an analyst should adjust the numbers for a better comparison.

Continue reading – CAPEX vs OPEX.

I got good info from your blog.