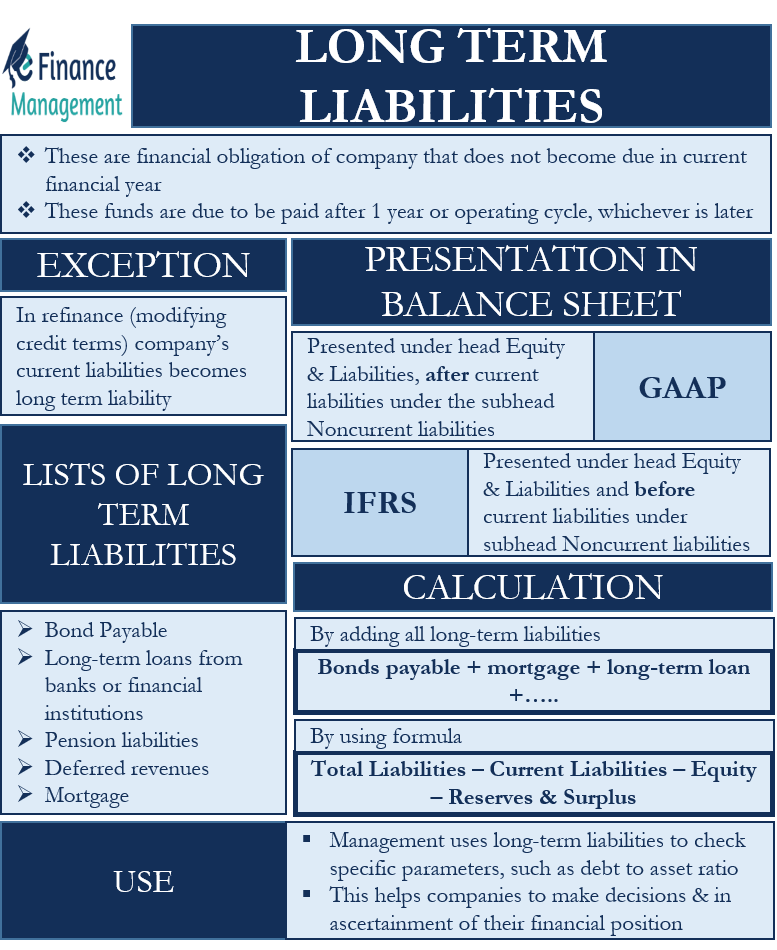

Long Term Liabilities: Meaning

Long-term liabilities are the financial obligations of a company that does not become due in the current financial year. Moreover, these funds are due to be paid after one year or the operating cycle, whichever is later. Further, if the operating cycle is less than one year, we will take one year as a base for identifying and classifying a liability between the short and long term. On the other hand, if the operating cycle is more than one year, we will take the operating cycle period as a base. Let us see an example to get a clear understanding of this concept of classification.

| Particulars | Year 0 | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

|---|---|---|---|---|---|---|

| Non-Current Liability | ||||||

| Long Term Liability | 5,00,000 | 5,00,000 | 4,00,000 | 3,00,000 | 2,00,000 | – |

| To be paid | – | 1,00,000 | 1,00,000 | 1,00,000 | 1,00,000 | – |

| Net Long-Term Liability | – | 4,00,000 | 3,00,000 | 2,00,000 | – | |

| Current Liability | ||||||

| Short Term | – | 1,00,000 | 1,00,000 | 1,00,000 | 1,00,000 | 1,00,000 |

| Total Liability | 5,00,000 | 4,00,000 | 3,00,000 | 2,00,000 | 1,00,000 | |

In the table above, a company takes a loan of $5,00,000 and pays $1,00,000 each year with interest. In the first year, the company shows $ 400000 in long-term liabilities and $1,00,000 separately as a short-term liability. Because $1,00,000 has to be paid in the current financial year. This process continues till that liability becomes nil.

Exception

There is one exception where a company’s current liability becomes long-term liabilities. And that is in the case of refinancing of the loan. It is a process where a company modifies an existing credit term and extends the period of payment, and that is how a short-term liability becomes a long-term liability.

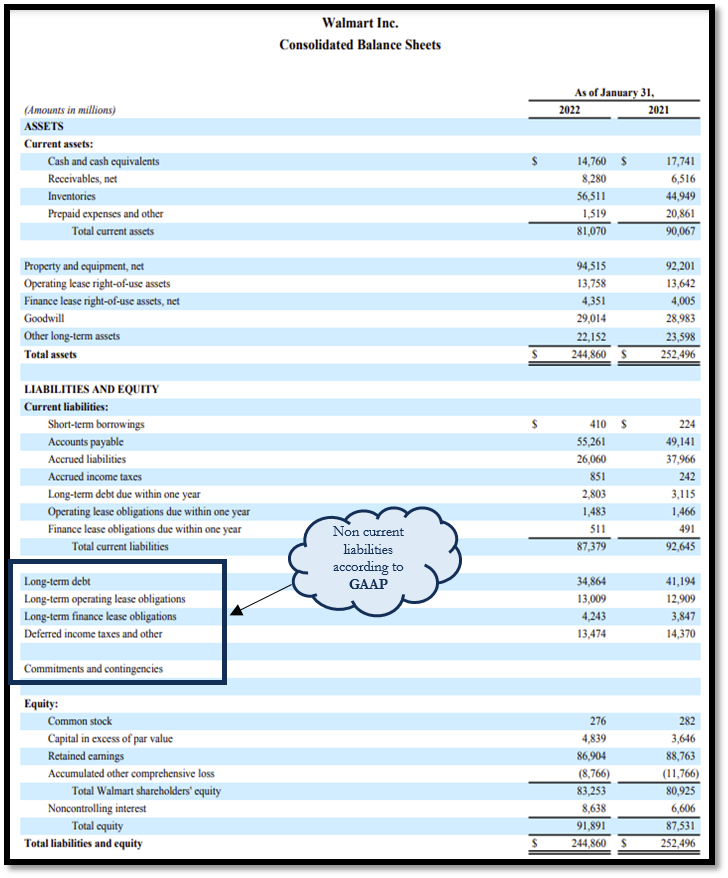

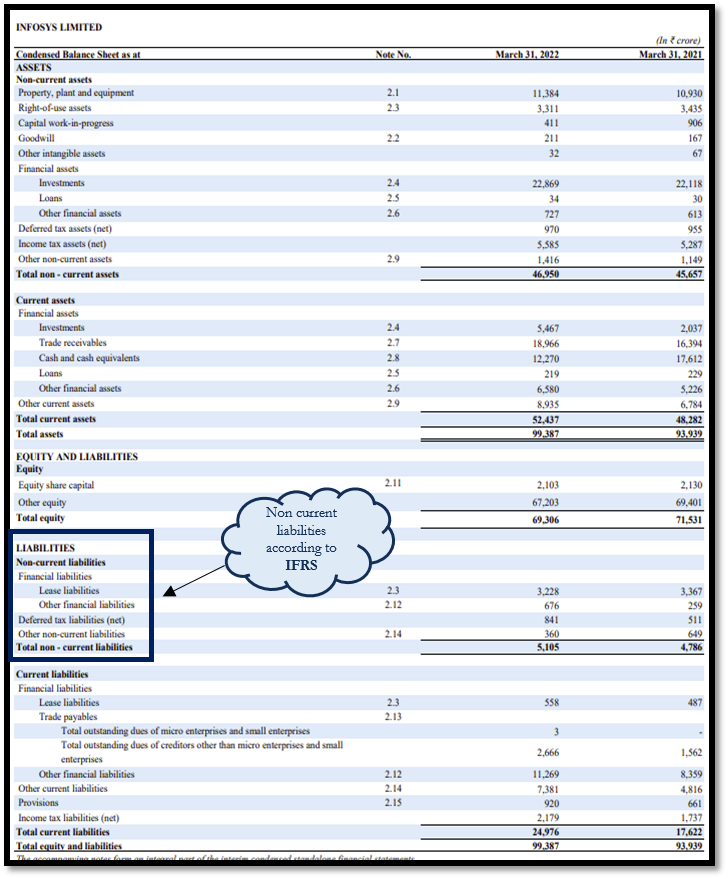

Long-Term Liabilities: Presentation in Balance Sheet

GAAP

Long-term liabilities are presented in the balance sheet of the company under the head Equity and Liabilities and after current liabilities under the subhead Non-current liabilities.

IFRS

Long-term liabilities are presented in the company’s balance sheet under the head Equity and Liabilities and before current liabilities under the sub-head Non-current liabilities.

You would observe that under both the practices it is presented under Equity and Liabilities with the sub-head Non-Current Liabilities only. The only difference is the sequence of items on the balance sheet. Under GAPP current assets are preceded by the Long Term or Non-Current Liabilities whereas in IFRS it succeeds Non-Current Liabilities.

Example/ List of Long Term Liabilities

Bond Payable

A bond is used for raising funds for a company. Usually, the repayment period of bonds extends beyond 3-5 years. Moreover, even after this period, the principal may be repaid either in one go or it can be in 2-4 installments. Interest may be paid every year and that will be part of the current liability. In the case of cumulative bonds, even the interest is also paid together with the principal. And such a scenario, even the interest portion will be part of long-term liabilities.

Long-Term Loans from Banks or Financial Institutions

A loan taken from banks or any financial institution for more than one year is considered a long-term liability.

Pension Liabilities

Pension liabilities are the amount that is kept aside to make pension payments in the future.

Advance received against supply or contracts

Sometimes the firms receive an advance against a contract or service or an advance against the supply of products or services. The delivery of such products or the completion of that contracts is beyond one year. Therefore, it is called unearned revenue and that is treated as a long-term liability.

Mortgage

It is an agreement where a company gets a loan against a mortgage of immovable property. Since the term of this loan is for a longer period, it is a long-term liability.

Also Read: Short-term Liabilities

How to Calculate Long-Term Liabilities

- By adding all the long-term liabilities – for example

Bonds payable + mortgage + long-term loan + …

- By using formula

Long-term liabilities = Total Liabilities – Current Liabilities – Equity – Reserves & Surplus

Use of Long-Term Liabilities

Management uses long-term liabilities to check specific parameters, such as debt to asset ratio, which shows how many assets have been funded by long-term debt or long-term funds. Similarly, for calculating the debt to equity ratio to know whether the gearing is right for the company or not. This ultimately helps companies to make various decisions about capital structure, and also helps in the ascertainment of their financial position.