Operating cycle and cash operating cycle are used interchangeably, but it’s a misconception. They are different by a small margin, but that makes a big difference.

This raw material conversion to cash is called the operating or working capital cycle.

Raw material >> Work-in-Process >> Finished Goods >> Accounts Receivable >> Cash

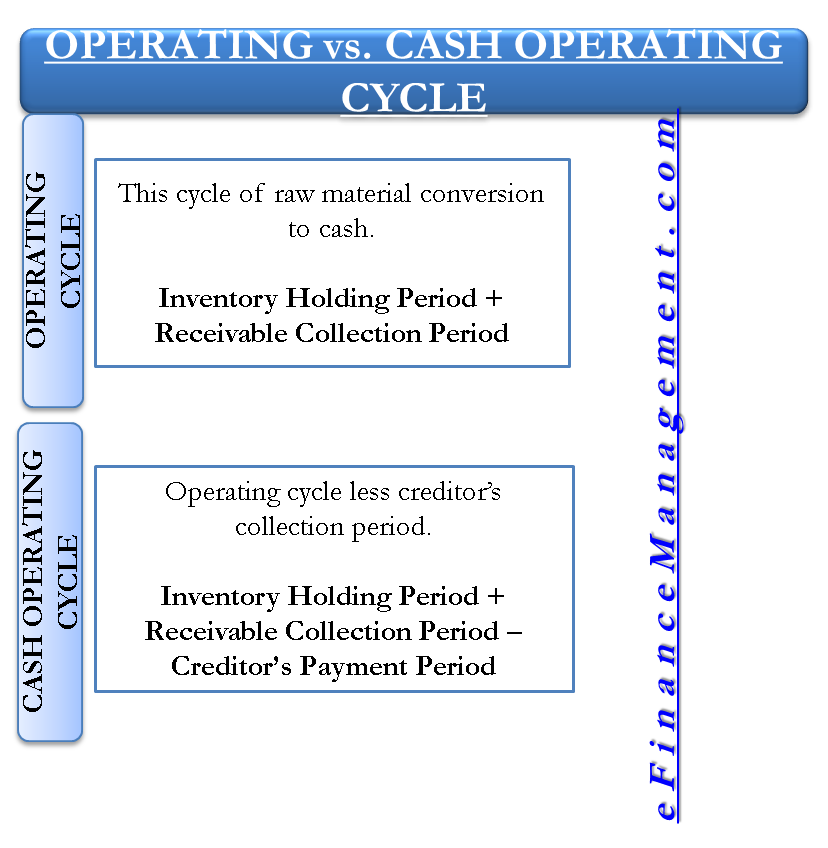

In terms of time, it is the time taken after the purchases of raw material till its translation into cash. The total of inventory holding period and receivable collection period of a firm is the operating cycle time of that firm.

Cash Operating Cycle

Like working capital, the operating cycle can also be gross operating cycle (operating cycle) and net operating cycle (cash operating cycle). The cash operating cycle is the gross operating cycle less the creditor’s collection period. It is the time period for which there is a requirement for working capital.

How to Calculate using Formula?

For the calculation of the operating cycle, the time of the operating cycle can be as follows:

1. Inventory Holding Period

Raw Material Holding Period

Work-in-process Period

Finished Goods Holding Period

2. Receivables Collection Period

Formula for Operating Cycle

Operating Cycle = Inventory Holding Period + Receivable Collection Period

Or, Operating Cycle = Raw Material Holding Period + Work-in-process Period + Finished Goods Holding Period + Receivable Collection Period

Formula for Cash Operating Cycle

Cash Operating Cycle = Inventory Holding Period + Receivable Collection Period – Creditor’s Payment Period

Or, Cash Operating Cycle = Raw Material Holding Period + Work-in-process Period

+ Finished Goods Holding Period + Receivable Collection Period – Creditor’s Payment Period

Operating Cycle Example

Suppose $500 worth of inventory is purchased from a supplier on 20 days of credit, and it was sold after 40 days of purchasing it. The credit of 40 days is given to the buyer. The buyer paid on completion of the credit period.

The operating cycle is extremely important because business is all about running the operating cycle smoothly. If it is running smoothly, almost everything will be smooth. If any part of the working capital cycle is stuck, the whole business gets disturbed. For a manager to effectively manage the business, he should understand his business cycle and potential threats and risks to it. Proactively, he should have ways and means to mitigate those threats and risks.

In our example, the operating cycle is 80 days. The entrepreneur should always focus on reducing it as much as possible, ensuring better utilization of their fixed assets. In turn, they will gain a higher return on their investment.

On the other hand, the cash operating cycle is the base for working capital estimations. In our example, the working capital requirement is $500 for 60 days. Banks take this as a base for funding their client. A manager handling finance should focus on reducing the cash cycle to save him the interest cost. Reducing this cycle means reducing the inventory holding period and increasing the supplier’s payment period. Other than normal strategies, the Japanese techniques ‘Just-in-Time (JIT)’ can reduce the inventory holding time to practically zero. More prominent companies are trying to adopt JIT with the help of tools like supplier system integration etc.

Sanjay Borad, Founder of eFinanceManagement, is a Management Consultant with 7 years of MNC experience and 11 years in Consultancy. He caters to clients with turnovers from 200 Million to 12,000 Million, including listed entities, and has vast industry experience in over 20 sectors. Additionally, he serves as a visiting faculty for Finance and Costing in MBA Colleges and CA, CMA Coaching Classes.

3 thoughts on “Operating and Cash Operating Cycle”

This is a very helpful site. I think that this will definitely help me to understand cash operating cycle. I think that this will definitely help me to do my business accounting very well. Thanks for sharing this article.

Great article. This will definitely help me to do my business accounting. This article is very easy to understand.I’ll definitely follow what you said here.

This is a very helpful site. I think that this will definitely help me to understand cash operating cycle. I think that this will definitely help me to do my business accounting very well. Thanks for sharing this article.

Great article. This will definitely help me to do my business accounting. This article is very easy to understand.I’ll definitely follow what you said here.

Very simple and easy to understand the explanation