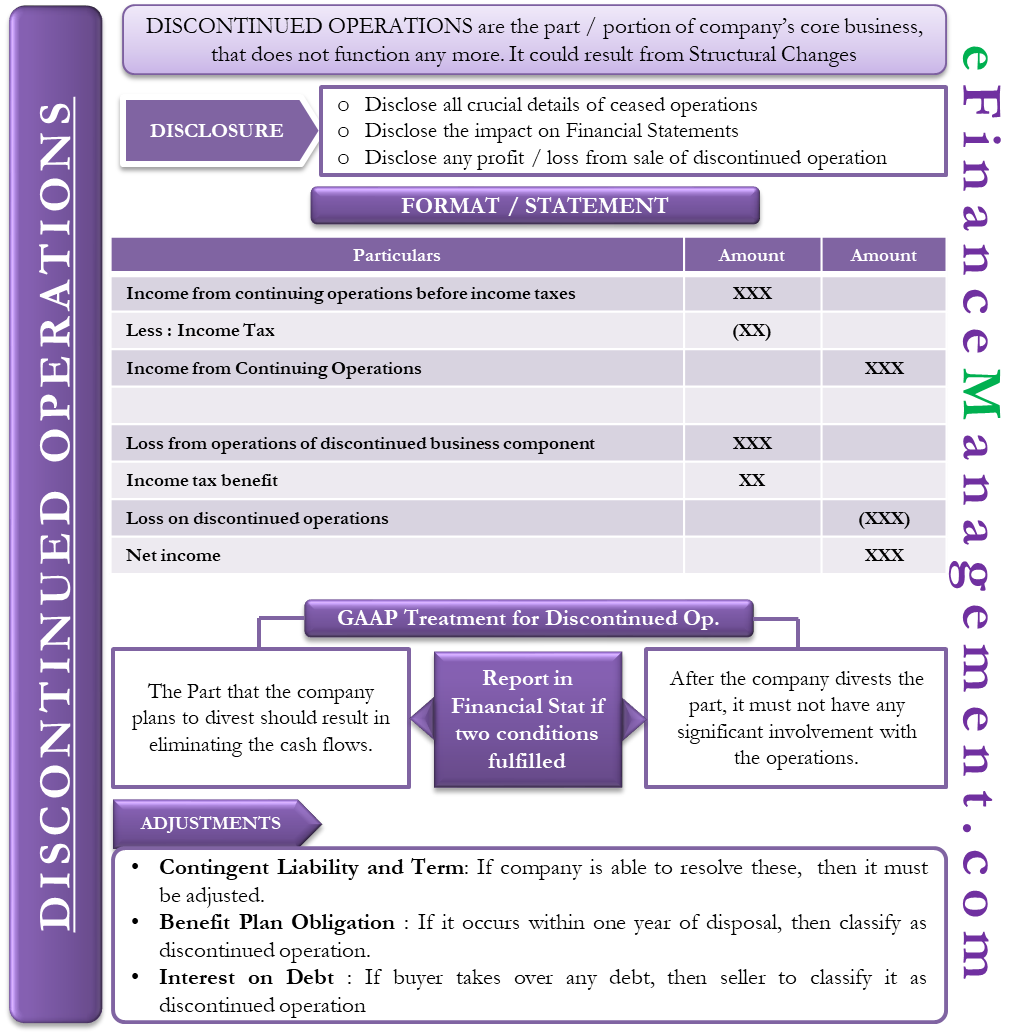

Discontinued Operations are that part or portion of a company’s core product that no longer functions. Also, these parts are either held for sale or are already sold. For accounting purposes, a company reports these parts separately from the continuing operations on the income statement.

Disclosure of Discontinued Operations

For a company, a discontinued operation could result from structural changes such as a shift in business models, sale of equipment, scrapping of product lines, and more. A company needs to follow strict accounting rules to disclose all crucial details regarding ceased operations. The company must also disclose its impact (if any) on the financial statements.

It does not mean that discontinued operations may not generate any profits for a business. In fact, in cases where the company is in the process of selling a part, such operations continue to generate profits. Still, the company must classify them as discontinued operations in the financial statements.

Importance of Disclosure

Moreover, a company must provide a clear definition of the operation (or operations) that is discontinued. Also, the management must clearly indicate that the discontinued operation is no longer part of the core operations.

Also Read: Divestitures

Such classification and information ensure that the external users get an accurate picture of the company’s continued operations. Additionally, the company must also disclose any profit or loss from the sale of a discontinued operation.

The distinction for discontinued operation also becomes very useful at the time of the merger. Such classification gives a clear picture of the company’s potential cash flows.

Disclosure on Income Statement

When a company discontinues operations, it has to report several items on the financial statements. Also, it is possible; that the discontinued operation generates some revenue in the current year in which the company shuts it down or sells it. Therefore, a company must calculate the gain or loss from operations, including the applicable income tax.

Such income tax is mostly a future benefit as discontinued operation usually leads to losses. Now, when the company calculates its total net income, this gain or loss from the discontinued operation must be included.

Also Read: Profit and Loss Statement

GAAP Treatment of Discontinued Operation

GAAP allows a company to report a discontinued operation on the financial statements if two conditions are met. First, the part that the company plans to divest should result in eliminating the cash flows. Second, after the company divests the part, it must not have any significant involvement with the operations.

Under IFRS (International financial reporting standards), the criteria are slightly different. IFRS also lays down two criteria. First, the company must dispose of or report it as being held for sale. Second, the asset or part that the company wants to remove must be distinguishable as a separate business.

Moreover, IFRS allows the equity method investments to be classified as held for sale. Also, under IFRS, the discontinued operation may continue involvement with operations.

Example (under GAAP)

The below scenarios will help you to understand discontinued operations better;

- A company, XYZ, has several products under various different product lines. XYZ tracks the cash flows for the product lines but not for each product. Now, if it plans to cease one of its products, then it must not classify the operations related to a single product as a discontinued operation as there is no way to track cash flows.

- Now XYZ plans to scrap one full product line. Since the company tracks cash flows for the product lines, it must classify it as a discontinued operation.

- XYZ also runs retail stores. It sells one store and agrees to supply the products to the buyer of the store. In this case, XYZ will continue to get the majority of cash flows from the same store. So, even though there is a change in the ownership, XYZ shouldn’t classify it as a discontinued operation.

- Suppose XYZ sells a few product lines. The sale agreement states that the buyer will pay XYZ a 5% royalty from the sale coming from these product lines for the next five years. In this case, XYZ will not have any continuing operational involvement in the product lines that it sells. So, the cash flows or the royalty is indirect, and therefore, it must classify the product lines as discontinued operations.

Format

If the conditions (under GAAP) are met, then the business must show the result of the discontinued operations in a separate section in the income statement. Also, if there is any gain or loss on disposal, then it should also come in the discontinued operations section. Below is a sample of how you should show operations that are discontinued in the income statement;

| Income from continuing operations before income taxes | $30,000,000 | |

| Income taxes | (10,500,000) | |

| Income from continuing operations | $19,500,000 | |

| Discontinued operations | ||

| Loss from operations of the discontinued business component | (12,000,000) | |

| Income tax benefit | 3,100,000 | |

| Loss on discontinued operations | (8,900,000) | |

| Net income | $10,600,000 |

Adjustments to Discontinued Operations

A company may discontinue an operation in the current year, but some related transactions may come up after the disposal transaction. Considering the adjustments for these were previously reported under discontinued operations, the company must then adjust them separately in the discontinued operation section of the income statement, provided they meet the GAAP requirements. Some examples of these adjustments are;

Contingent liabilities – if a company is able to resolve any such liability related to the disposal transaction, then it must come as an adjustment. For example, any site remediation liabilities are retained by the seller.

Contingent terms – if a company resolves any contingencies related to the terms of the disposal transaction, then it must be adjusted—for example, any adjustment to the initial price paid.

Benefit plan obligations – if such obligations occur within a year of the disposal transaction, then the company must classify it as discontinued operations—for example, post-employment benefits.

Interest on debt – if the buyer of a discontinued operation takes over any related debt, then the seller should classify any interest expense borne by it under discontinued operation.