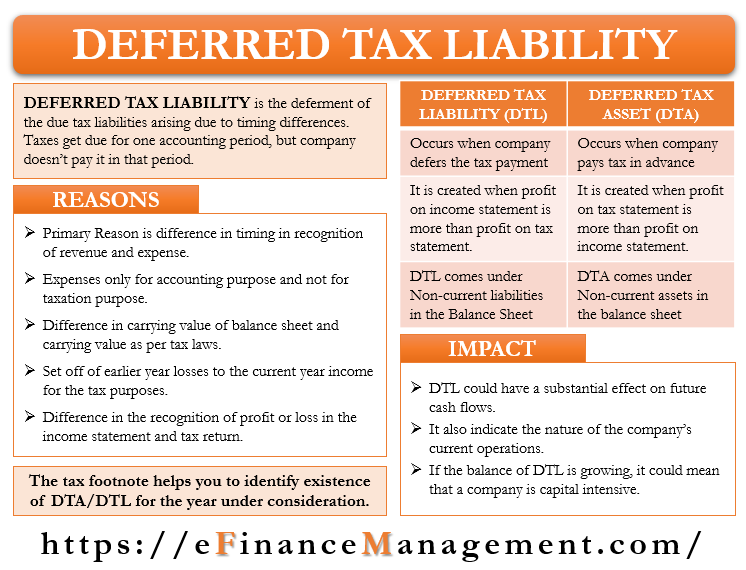

Deferred Tax Liabilities or Deferred Tax Liability (DTL) is the deferment of the due tax liabilities. In other words, when the due tax will be paid in future years. Such a difference in tax primarily arises because of the timing difference between when the tax is due and when the company pays it. Or, we can say taxes get due for one accounting period, but the company doesn’t pay it in that period. It is a type of long-term liability.

We can also say that DTL is the income tax that a company needs to pay in the future because of temporary differences in tax calculation. In simple words, we can also call it a provision for future tax, but it is different from the tax provision.

For example, payment due to current receivables is not taxable until they make the payment. However, the sale that a company makes on credit comes in the income statement, resulting in variance between earning and taxable income.

Deferred Tax Liabilities – Why it Arises?

Generally, the accounting rules (GAAP and IFRS) are different from the tax laws of a country. Such a difference in tax laws leads to a difference between the calculations of income tax when using the income statement figures and using the actual taxation rules. This difference results in deferred tax liabilities or assets.

A company will have a deferred tax liability on its balance sheet if the earning before taxes on the income statement is more than the taxable income on the tax return. In case the earning is less on the income statement. It would result in a deferred tax asset (DTA).

These differences are temporary as the company would pay them in the future. Thus, the company records it as deferred tax liability.

Following are some reasons that result in deferred tax liabilities:

- The primary reason, as said above, is the difference in timing in recognition of revenue and expense.

- Some expenses and revenue are there only for the income statement and not for tax purposes, or vice versa.

- There is a difference in the carrying value of the assets on the balance sheet and for tax purposes.

- There is a difference in recognition of profit or loss in the income statement and tax return.

- Then there is a set-off of earlier year losses to the current year income for the tax purposes.

- Sometimes a company may choose to carry forward its profit to the next year. Such an adjustment allows the company to lower its tax liability for the current year. It creates a DTL as the company will eventually have to pay taxes on the profit it carried forward.

Deferred Tax Liabilities Examples

One common cause of deferred tax liability is if a company uses accelerating depreciation for tax calculation and the straight-line method for accounting purposes. For example, if a company has an asset worth $10,000 with a useful life of 10 years. The tax rate is 30%.

Now suppose for the first year, the company uses straight-line depreciation of $1,000 and MACRS depreciation of $1,500. For the rest of the years, the depreciation for both tax and accounts purposes is the same. Now, the difference of $500 is temporary. For this, the company records $150 ($500 *30%) as the deferred tax liability on the balance sheet.

Revenue recognition policy is another source of DTL. For example, a company sells goods worth $5,000 to a customer, who will pay in five equal installments. In its books, the company shows a full $5,000 a sale. But, for the taxation purpose, it only receives $1,000 from the customer in the first year. It results in a difference of $4,000, which the company expects to adjust over the next four years. If the tax rate is 30%, the company will record $1,200 ($4,000 * 30%) as DTL in its books.

Another example of deferred tax liabilities is the difference in method to value inventory. As per the U.S. tax code, a company must use LIFO (last-in-first-out) method to value its stock. Some firms, however, may go for FIFO (first-in-first-out) to value the inventory. It may result in differences between the value of inventory in tax and financial books, leading to DTL.

For example, Company A buys 500 mobiles for $100 in the first six months and 500 mobiles at $150 in the last six months. In the full year, the company sells 500 mobiles. As per FIFO, the value of inventory would be $75,000, while as LIFO, the value would be $50,000. If the tax rate is 30%, Company A will incur a deferred tax liability of $7,500 ($25,000 * 30%).

Change in Tax Rate

A company must account for any change in the tax rate after it calculates its deferred tax liabilities. It must adjust the DTL as per the change in the tax rate. If there is an increase in the tax rate, there would be an increase in the company’s DTL and vice versa. Also, a company must adjust the balance sheet values of DTL and DTA as per the change in the tax rate.

Deferred Tax Liability vs Deferred Tax Asset

Like DTL, DTA (Deferred Tax Asset) also arises from the difference in the tax code and accounting guidelines. Following are the difference between the two:

Recognition

DTA occurs if a company pays tax in advance, which accrues in a later period. If a tax expense is of the current year, but the company pays it later, then it is a DTL.

Creation

If the profit on the income statement is more than the taxable income, it creates DTL. On the other hand, if the profit on the income statement is less than the taxable income, then it results in DTA.

Treatment

DTA comes under Non-current assets on the balance sheet, while DTL comes under Non-current liabilities.

How to Identify DTL?

A company shows its deferred tax liabilities on the balance sheet. But, to know details or what is driving the DTL, one needs to read the tax footnotes that a company provides. In the notes, companies do mention the transactions that result in deferred tax assets and liabilities. Moreover, companies also share effective tax rates.

Below are some of the items that you will find in the footnotes for DTL:

- Any change that has been brought out in the company’s policy regarding depreciation or amortization of assets.

- Change in capitalizing and revenue recognition policy.

Impact of Deferred Tax Liability

Once we understand DTL and what is causing such liabilities, you can quickly analyze its impact (if any) on the operations of the company. If the amount is significant, then DTL could have a substantial effect on future cash flows.

Along with the impact, you should also try to study the trend of DTL. You should analyze the change in their balances to get an idea of their future direction. Analyzing the pattern would give you an idea if it would move up or go down in the future. Also, it may indicate the nature of the company’s current operations.

For instance, if the balance of DTL is growing, it could mean that a company is capital intensive. It is because a new asset would result in more depreciation if a company is following the decelerating depreciation method. It would result in a difference between the earnings on the income statement and taxable income.