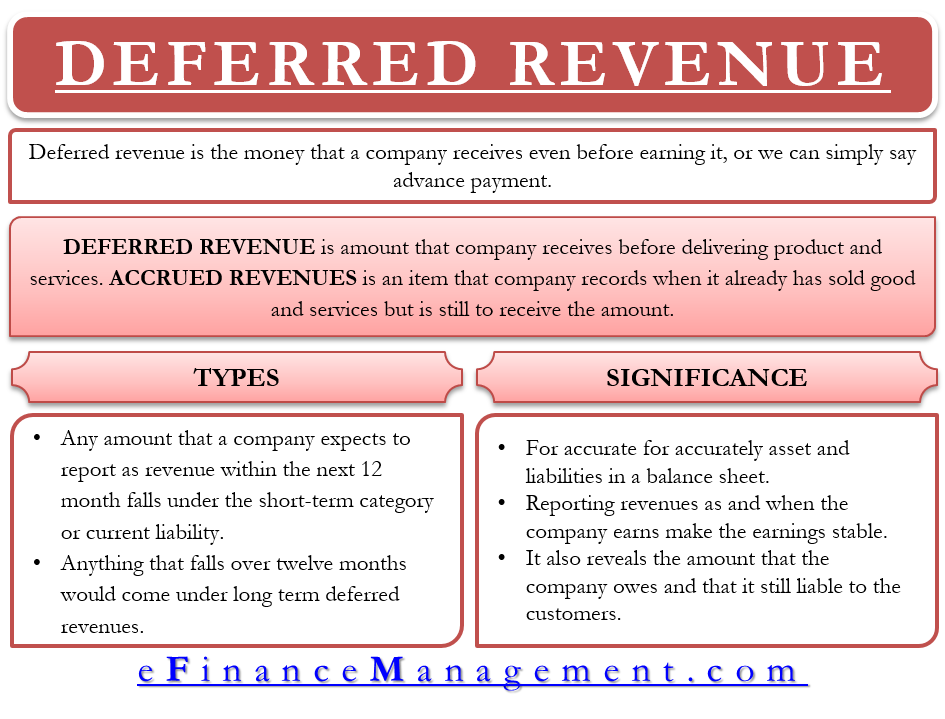

Deferred revenue is the money that a company receives even before earning it, or we can simply say advance payment. Companies do not report deferred revenues in the income statement because they are still to earn it as revenue. Such revenue is not a ‘real revenue’ and doesn’t affect the net income or loss. Therefore, the amount comes on the balance sheet as a liability. Such amounts can also come on the balance sheet as Customer Deposits or Unearned Revenues.

Usually, companies that deal in subscription-based products and services, which require prepayments, report such items. Deferred revenue could be payment of rent in advance or prepayment for a service, such as tax, subscription to a streaming service, and more. More examples of deferred revenues are advance rent, deposits for future services, service contracts, legal retainers, advance insurance, ticket selling, etc.

As the company delivers the product and services, they add the revenue to the income statement. Many companies do aggressive accounting wherein they add such items as revenue in the income statement.

Deferred Revenue Vs. Accrued Revenue

Deferred revenue is the amount that a company receives before delivering the product and services. On the other hand, accrued revenues are items that a company records when it has already sold the goods and services but is still to receive the amount. Most companies add the item into the account receivables category, and accountants then do not post it separately.

Also Read: Unearned Revenue

One example of it is the interest earned by the company but not received. The journal entry for this is to debit or increase interest receivable (an asset account) and credit or raise interest revenue, which comes in the income statement. Once the company receives the interest, it debits the cash and credits the interest.

In the case of deferred revenue, the journal entry is to debit the cash or increase the cash and credit or increase the liability account. After the company delivers the service or product, the entry is to debit or reduce the liability account and credit or raise the revenue account. Now, the deferred revenue turns into ‘real revenue’ and impacts the net income or loss.

All businesses do not necessarily report deferred revenue. The service companies where customers make full upfront payments usually report tons of such revenue. Though the customers make a full upfront payment, companies recognize revenue over the term of the service.

Short and Long-term Deferred Revenues

Since companies reports deferred revenue in the subsequent quarters, the amount has to be deducted from the deferred revenue account. Any amount that a company expects to report as revenue within the next 12 months falls under the short-term category or current liability. And anything that falls over twelve months would come under long-term deferred revenues.

A subscription service provider who offers different packages will get the subscription amount upfront. For instance, an online magazine offering subscription service will have monthly, half-yearly and annual packages. When the customer opts for the half-yearly package, they are paying upfront for those six months. However, the company evenly distributes the payment over six months and shows it in the income statement for each month.

Let’s understand this with the help of a simple example. Assume you have a subscription to a magazine for six months, and you pay the full amount of $24 ($4 per month) upfront. The magazine will put the full amount in the short-term deferred revenues line and add it as cash in the balance sheet. Now, for each month, it will move $4 out of the deferred revenues to report it as revenue in the income statement.

Now, if you pay in advance for two years ($96), $48 will go into the short-term deferred revenues line. And the remaining into the long-term deferred revenues. It is because the company will realize it after twelve months. After every month, $4 from the short-term will come as revenue in the income statement. Also, $4 will move each month from the long-term to the short-term deferred revenue line.

Significance of Deferred Revenue

- It is an important item to accurately report assets and liabilities on a balance sheet. By reporting deferred revenue on the liability side of the balance sheet, the company avoids reporting unearned income in the asset. Therefore, it avoids overvaluing the company’s net worth.

- Deferred revenue holds significance for the company as they finance operations. Thus relieving the burden on other assets or avoiding taking a loan.

- Payment by customers can vary and impact financial performance. Thus, investors may not like such volatility. So, reporting revenues as and when the company earns makes the earnings stable.

- It also reveals the amount that the company owes and that it is still liable to the customers. Though cash is the safest asset, the cash from deferred revenue may be risky. Cash that company gets but it is yet to earn, is a risk unless it delivers the product or service.

Valuation of Deferred Revenue

The challenge of valuing deferred revenue is to understand the performance obligation. The fair value of deferred revenue is taken as per the nature of activities that a company needs to perform and the costs that it incurs to complete the task.

The companies usually value deferred revenues using the bottom-up approach. Under this, the company adds the cost that it incurs to fulfill the performance obligation to the profit margin. The cost does not include items such as marketing, training, and recruiting. Such costs are not included as the company incurs these either before the business combination, or these are not needed to fulfill the obligation.

Alternatively, managers can also use the top-down approach. Such an approach relates to taking the market price of the deferred component and deducting the cost that is already incurred.

In the case of an acquisition or a merger of a software company, the GAAP rule requires the deferred revenue to be revalued at current market value instead of book value. For instance, a company that is showing $1000 as deferred revenue will show a different amount after it recalculates at the fair market value.

Final Words

Deferred revenue is a crucial concept that helps a company to avoid misrepresenting assets and liabilities. It is mostly useful for companies that get payments in advance before it delivers products and services.