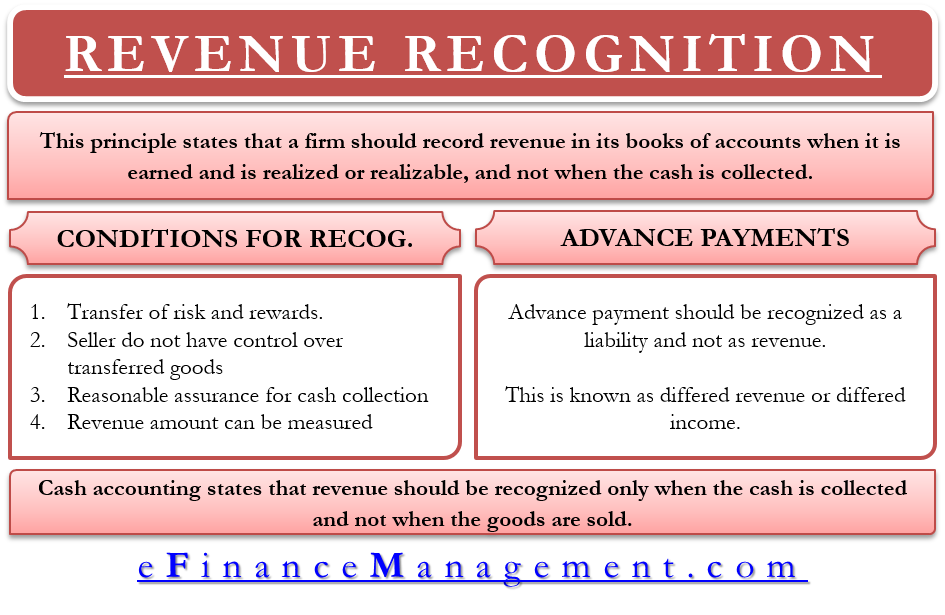

The revenue recognition principle states that a firm should record revenue in its books of accounts when it is earned, realized, or realizable, and not when the cash is collected. Revenue is earned when the company delivers its products or services. This means that the company has carried out its part of the deal. Revenues are realized when the cash is received for the goods/services sold. Revenues are realizable when the company receives an asset in exchange for the goods/services delivered. This asset usually is accounts receivables which can be converted into cash. E.g., suppose a customer purchases a television worth $5,000 from a shop on credit. In that case, the shop owner should immediately record the revenue even if it does not expect the customer to pay the purchase amount for several weeks.

One may question, what if the customer doesn’t pay for that purchase? First of all, as a wise businessman, you won’t sell a product on credit to someone whom you don’t expect to pay. However, later if you develop this doubt on some customers, in such a case, the solution is not to wait till all the customers pay their dues. The solution is to make a provision for such doubtful debts.

Conditions to Fulfill for Recording Revenue

According to the IFRS criteria, a firm must check for the following conditions before recognizing revenue:

- There is a transfer of risk and rewards from the seller to the buyer.

- The seller doesn’t have control over the transferred goods.

- There is a reasonable level of assurance regarding the collection of cash payments.

- The amount of revenue that is earned can be reasonably measured.

- Costs of revenue can be reasonably measured in the same period.

Revenue Recognition vs. Cash Accounting

The opposite of the revenue recognition principle is cash accounting. Cash accounting states that revenue should be recognized only when the cash is collected and not when the goods are sold. The revenue recognition principle, a part of accrual accounting, is superior to cash accounting. This superiority can be understood with the help of an example.

Applying Cash Accounting

Suppose Sam starts a new business of retailing t-shirts. He calculates that a t-shirt will cost him a total of $7.5. He plans to sell them at $10 each. On the first of April, he started the business and purchased 100 t-shirts. In the first month of his business, he sold all the 100 t-shirts to 100 different customers. Out of these 100 customers, 50 paid in cash, while the remaining 50 promised to pay in the next month. As Sam sits down on 30th April, using cash accounting, his calculations are as follows:

Also Read: Cash Basis Accounting

- Sales revenue (50 * 10) = 500

- Cost of Goods Sold (100 * 7.5) = 750

- Net Loss (1 – 2) = 250

Applying Revenue Recognition Principle

Cash accounting indicates that he has lost money. What puzzles Sam is that even after selling all the 100 t-shirts at a profit of $2.5 each, how could he possibly make a loss? After more analysis, he understands that though he has sold all the 100 t-shirts, he has not recognized the revenue he has earned from all of them. He understands that though he hasn’t received cash for 50 t-shirts, the earnings from them belong to this month’s revenue and not the month in which he will receive cash. So, he goes by the revenue recognition principle, and now his calculation looks like this:

- Sales revenue (100 * 10) = 1000

- Cost of Goods Sold (100 * 7.5) = 750

- Net Profit (1 – 2) = 250

This is how the revenue recognition principle gives a true picture of a firm’s profitability in a period.

Treatment for Advance Payments

Revenue recognition principle states that a firm should recognize revenue as soon as it earns them, and they are realized or realizable, no matter when the actual cash is collected. But, what if the firm receives cash in advance? Suppose a firm receives cash, even before it delivers the products or carries out its part of the deal. In that case, the revenue recognition principle states that a firm should recognize such advance payments as a liability and not as revenue. We usually call this resulting liability as differed revenue or differed income. Only when the firm completes its part of the deal should it consider the advance payment as revenue.

Exceptions to Revenue Recognition Principle

In the case of long-term construction and defense projects, it takes years to complete the task. Firms dealing with such long-term projects recognize revenues in two ways. (A) Proportionate completion method in which a firm recognizes revenues at various stages of completion. The firm divides the entire job into various stages of completion and recognizes revenue as soon as a stage of the job is complete. (B) Completed service contract method in which a firm recognizes revenue only when the whole rendering of services is complete.

Some companies recognize revenue as soon as the manufacturing process is complete. Mining and oil companies usually use this system as goods are effectively sold in their business as soon as they are mined.

In some businesses, the possibility of sales returns is high with every transaction. In such cases, companies may recognize revenue only after the right to return a product is gone.

Read about various other Accounting Principles.

Quiz on Revenue Recognition Principle

This quiz will help you to take a quick test of what you have read here.

very well explained. thank you