What are Capitalizing Assets?

Capitalizing assets means you are carrying an asset to the balance sheet. It indicates you purchased an asset, the life of which is more than one financial year. In other words, capitalizing can be defined as ‘spreading of asset value into a number of years equals to the life of the asset by means of depreciation.’

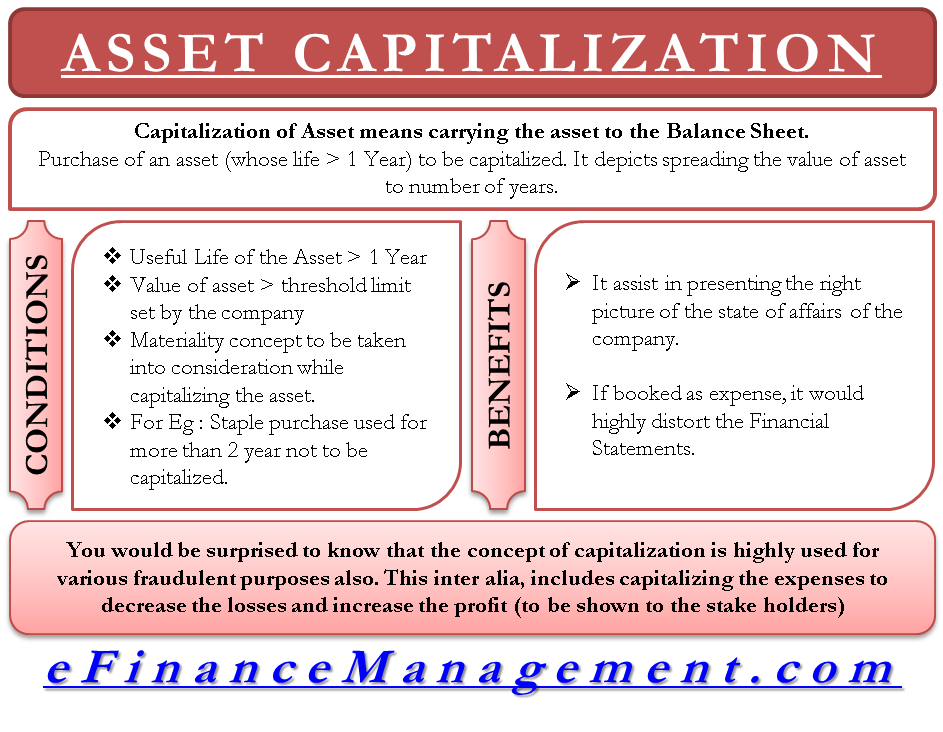

Conditions for Capitalizing an Asset

Normally, there are two conditions when the assets are capitalized

- When the asset’s useful life is more than 1 year, the financial year.

- The asset’s value is more than the threshold limit set by the company for capitalizing.

Capitalizing Asset Example

Let’s try to understand capitalizing on an asset with the help of an example. Supposed Mr. John has a shop near Garden. He wishes to start selling ice cream from that shop. So, he buys cold storage worth $1500 to store the ice cream. Note that the life of this storage is 10 years. The total expected revenue from this venture is Dollar 20000 for the year, and the cost of ice cream would be $18,000. And there are other expenses totaling $1,000.

| Particulars | Cash Flow | Profit / Loss |

| Revenues | 20,000.00 | 20,000.00 |

| Ice Cream Purchase Cost | (18,000.00) | (18,000.00) |

| Other Operating Expenses | (1,000.00) | (1,000.00) |

| Cost of Long-Term Asset i.e. Cold Storage. | (1,500.00) | (1,50.00) |

| Total | (500.00) | 850.00 |

In the above table, we have taken only 1/10th part of the cold storage cost in the profit loss column. It is because the cold storage will be useful for 10 years from now. Let’s take the other side; if we deduct the whole cost of $1,500, we get a loss of $500 in the first year, and that is not the right presentation. If Mr. John would have known that he would make a loss of $500 in the first year, he would not have made the investment itself.

Capitalizing Asset and Matching Principle

There is a role of the basic accounting principle, i.e., the matching principle behind capitalizing assets. The principle states that you should book only those expenses directly related to bringing out the revenues of the same period. When we invest in a long-term asset, we do not consume the whole asset in the first year or the first financial year itself, and that is why we capitalize on the assets and depreciate them every year till the life of the asset. In the example also, we are capitalizing the cold storage for the same reason.

Also Read: Capitalizing Versus Expensing Costs

Benefit of Capitalizing

The primary benefit of capitalizing is that it assists in presenting the right picture of the state of affairs of a business. Suppose the principle of booking an asset as an expense in the year of its purchase will highly distort the financial statements. In the first year, you will see heavy losses, and you will see heavy profits in the coming years.

Fraudulent Practices

You will be surprised to know that the concept of capitalizing is widely used for fraudulent practices as well. Obviously, everybody likes to have a good profit in the profit and loss account. But, for some reason, a business is not able to earn profit in a particular year. On the other hand, showing losses in the financial statement will go against the business’s creditworthiness in the eyes of bankers, shareholders, creditors, etc.

At this juncture, managers enter into fraudulent practices by capitalizing expenses that should not be capitalized as per the accounting principles. By doing this, they are able to reduce expenses and thereby show a profit in the financial statements.

Capitalizing and Immateriality

It is not necessary to capitalize on every small asset with longer life. For example, a stapler used as stationery items has a life of more than 1 year, but we need to choose not to capitalize on this asset, looking at the minuscule value of this asset in comparison to the business size. This is where the immateriality concept plays a role.

Also Read: Capital Expenditure

Which Assets are to be capitalized?

Following is a list of assets that are normally capitalized apart from those whose value is less than the threshold limit and those consumed within one financial year.

- Land

- Buildings

- Improvements

- Furnishing

- Equipment

- Capital Leases

- Vehicles

- Library Content

- Misc Assets

- Livestock

- Software

- Media (Films Generally Expensed)

- Works of Art

Read Capitalizing Versus Expensing Costs for more details.