What is Market Risk?

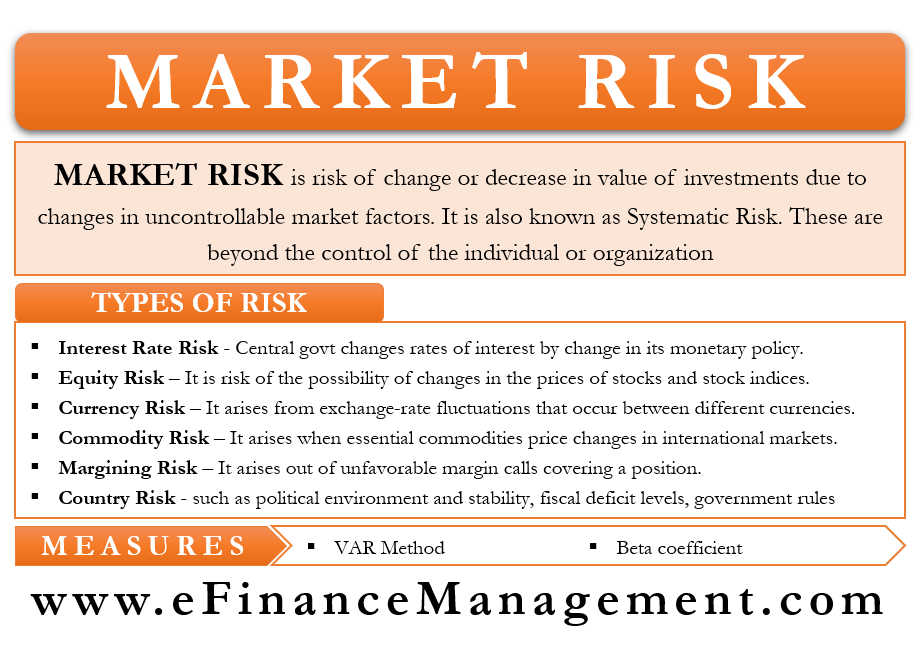

Market risk is the risk of change or decrease in the value of investments due to changes in uncontrollable market factors. These market factors can be recession or depression, changes in government policies affecting key interest rates, natural calamities and disasters, political unrest, terrorism, etc.

Another name for Market risk is “Systematic risk,” which affects the entire financial market as a whole. Hence, these are beyond the control of any individual or organization. Such risk can be controlled or curtailed by various strategies. The strategies may call for diversifying the various investments. Further, the diversification should be in such asset classes and portfolios that are directly unrelated to the market. This negative correlation with the market will provide stability to the portfolio or financial assets. Also, continuous monitoring and control by the investors are important. This will help them to keep a check on macro variables such as inflation and rate of interest to minimize market risk.

What are the Key Types of Market Risk?

There are many types of market risks that an investor can face.

Interest Rate Risk

Fixed-income securities such as bonds are most affected by changes in the interest rate in an economy. The Central bank of a country changes the rates of interest prevailing in the economy by changing its monetary policy. Such interest rate changes directly impact the prices of securities and investments. A high market rate of interest will lead to a decline in demand for lower interest rate instruments. Similarly, a reduction in the market rate of interest will result in a shift of investment to higher interest rate financial instruments. These changes in interest rates change the traded value of these bonds and financial instruments. If the rates are on an increasing trend, the value of the existing securities will go down and vice versa.

Equity Risk

Equity risk is the risk of the possibility of changes in the prices of stocks and stock indices. This can be due to various factors such as a new invention or discovery, new product launches, changes in government rules and laws, the general economic environment, any major epidemic, etc.

Currency Risk

Currency risk arises from exchange-rate fluctuations that occur between different currencies. Exchange rates are not country-specific and depend on the rates of currencies worldwide. Hence, investors that invest in international markets and foreign countries are more prone to currency risk. Not only the corporates doing trading in the international market will also get affected by currency fluctuations because their net inflow or outflow will vary with the change in the currency rates.

Commodity Risk

Commodity risk arises due to the changes in the prices of essential commodities in the international markets, such as crude oil, that affect the financial markets across the world. Such risk is also out of control for any country and may happen due to changes in demand and supply, political situation, government laws and controls, etc. Similar could be the risk of price changes in other key commodities like bullion, steel, copper, natural gas, etc.

Margining Risk

Margining risk arises out of unfavorable margin calls covering a position. This may lead to uncertainty in cash flows for an investor.

Country Risk

Factors such as political environment and stability, fiscal deficit levels, government rules, regulations, and control, etc., affect the returns from an investment. Instability in the economy of countries can pose a major risk to investment value and returns, and it may fluctuate wildly.

What is the Measure of Market Risk?

VAR Method

The best measure of market risk is the value-at-risk or VAR method. It is a statistical method for managing risk. It calculates the probable loss that a stock or portfolio can potentially make and the probability for the same. The measure of VAR is price units or a percentage form that makes it easy to understand and interpret.

It can be applied to all types of investment assets like stock, bonds, derivatives, etc. It helps assess the profit potential of different investments and accordingly plan how much to invest in a respective investment opportunity.

The VAR method has a number of limitations too. The method involves the calculation of risk and return for each individual asset and also the correlation between them. Thus, it becomes very complex to calculate VAR if the number of assets is large and diversified in a portfolio. Also, it assumes that the portfolio remains unchanged over a specific period of time. Thus, it is more feasible for the short-term and becomes unreliable in the case of long-term investments where the portfolio content keeps on changing.

Beta Coefficient

Beta coefficient is a measure of volatility or market risk of an investment or portfolio in comparison with the market. It is of use in the Capital Asset Pricing Model (CAPM) and describes the asset return in view of the systematic risk. It helps to gauge the risk addition to a diversified portfolio by the inclusion of a stock or investment.

An investment with a Beta coefficient equal to “1” is as volatile as the market. In other words, the security or stock is said to be strongly correlated with the market and will behave in sync with the market changes. Such security can also be said to have a systematic risk to the market.

A beta value greater than “1” indicates that the investment or security has more volatility than the market. So, in a rising market, it can rise faster than the market, and vice versa. Therefore, the investment is of high risk, but the returns too can be much higher than the market.

Similarly, an investment with a Beta coefficient of less than one means that it is less volatile than the market. Hence, the investment is a safe option with little risk, but the return factor is also limited.

Regulations for Market Risk

There are a few regulations, too, with regards to disclosure of the market risk of investments. The Securities and Exchange Commission makes it compulsory for companies to disclose their market risk exposure in a section in all annual reports submitted on Form 10-K. It requires the companies to disclose their exposure to financial markets and how volatility in the markets will impact them.

Many Companies have a simple business operation in view of the general public but may be involved in trading and investing in complex derivatives and financial instruments. They may put the money of gullible investors at risk through such risky investment activities. Hence, the required disclosures in its Annual Report can help an investor gauge the risk of investing in such a company.