A chart of accounts is an important part of the accounting system and serves as a base for preparing accounts. It lists all the accounts that a company uses in the accounting system. It does not include other information about the accounts, including their balances, either debits or credits. Before moving to the chart of accounts example, it is crucial to know what is a chart of accounts. We recommend reading the article – Chart of Accounts prior to moving toward the example.

Refer to the chart of accounts example below to get a basic idea of how companies number their chart of accounts.

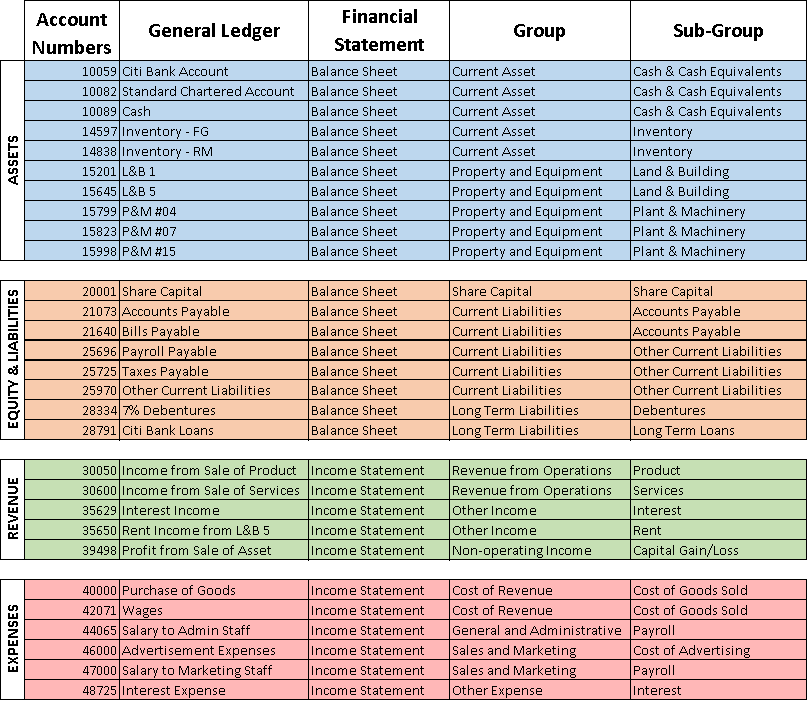

Chart of Accounts Example

A company first needs to define the range of numbers it will use for numbering its assets, liabilities, revenues, and expenses. Below is a table that defines the range of numbers that the company ABC has used.

| Account Group Description | Account Numbers | |

| From | To | |

| Assets | 10000 | 19999 |

| Equities & Liabilities | 20000 | 29999 |

| Revenue | 30000 | 39999 |

| Expenses | 40000 | 49999 |

Here, we have used five-digit codes. A company can also use up to ten-digit codes for its chart of accounts depending on the number of ledgers it is required to maintain.

After defining the range, the next step is to divide this range among the account groups and sub-groups such as the assets group will have current assets, property & equipment, etc. while liabilities include current liabilities and long-term liabilities. The following table shows how the above range is divided among various account groups.

| Account Group Description | Account Numbers | |

| From | To | |

| ASSETS | ||

| Current Assets | ||

| Cash & Cash Equivalents | 10000 | 10999 |

| Account Receivables | 11000 | 13999 |

| Other Current Assets | 14000 | 14999 |

| Property & Equipment | ||

| Land & Building | 15000 | 15999 |

| Plant & Machinery | 16000 | 16999 |

| Furniture | 17000 | 17999 |

| Intangible Assets | ||

| Trademark | 18000 | 18999 |

| Patent | 19000 | 19999 |

| EQUITIES & LIABILITIES | ||

| Share Capital | 20000 | 20999 |

| Accounts Payable | 21000 | 24999 |

| Other Current Liabilities | 25000 | 27999 |

| Long-term Liabilities | 28000 | 29999 |

| REVENUE | ||

| Revenue from Operations | 30000 | 35999 |

| Other Income | 36000 | 39999 |

| EXPENSES | ||

| Cost of Revenue | 40000 | 42999 |

| Services & Others | 43000 | 43999 |

| General & Administrative | 44000 | 45999 |

| Sales & Marketing | 46000 | 46999 |

| Research & Development | 47000 | 47999 |

| Other Expenses | 48000 | 48999 |

| Provision for Income Tax | 49000 | 49999 |

This range is assigned on the basis of the expectation of the number of ledgers that will be covered under each account group.

Now the accounts (general ledgers) falling under these account groups will be numbered from the range allowed to these account groups. Look below to know how.

How to Edit Chart of Accounts

In the future, if there is a new account, ABC company can adjust it between the same range of numbers. Usually, a company sets a range of numbers for a particular account type. In the above case, ABC has set numbers 10000-19999 for assets, 20000-29999 for equities & liabilities, 30000-39999 for revenue, and 40000-49999 for expenses.

For instance, if there is a new asset account for prepaid insurance. The company can list it as 14979 or any other number between 14000-14999 that has not been allocated. If the numbers are allocated, then the company can give it a sub-number, such as 14999-1.

Though an option to add a sub-number is available, the company should always try to avoid such situations. It should frame its chart of accounts in a manner that the range defined for an account group should have enough codes available for the addition of new ledgers.

A point to note is that the chart of accounts of one company may not be suitable for another company. Ledgers under the account group “inventory” in a company operating in the FMCG industry will be more as compared to the one operating in the Iron & Steel industry.

RELATED POSTS

- Accounting Worksheet – Meaning, Objectives, Benefits, and Format

- Closing Entries

- Balance Sheet – Definition and Meaning

- Classified Balance Sheet – Meaning, Importance, Format And More

- Calculation of Liabilities from Balance Sheet

- Fundamentals of Accounting: Meaning, Principles, Categories, and Statements