What is a Single Entry System?

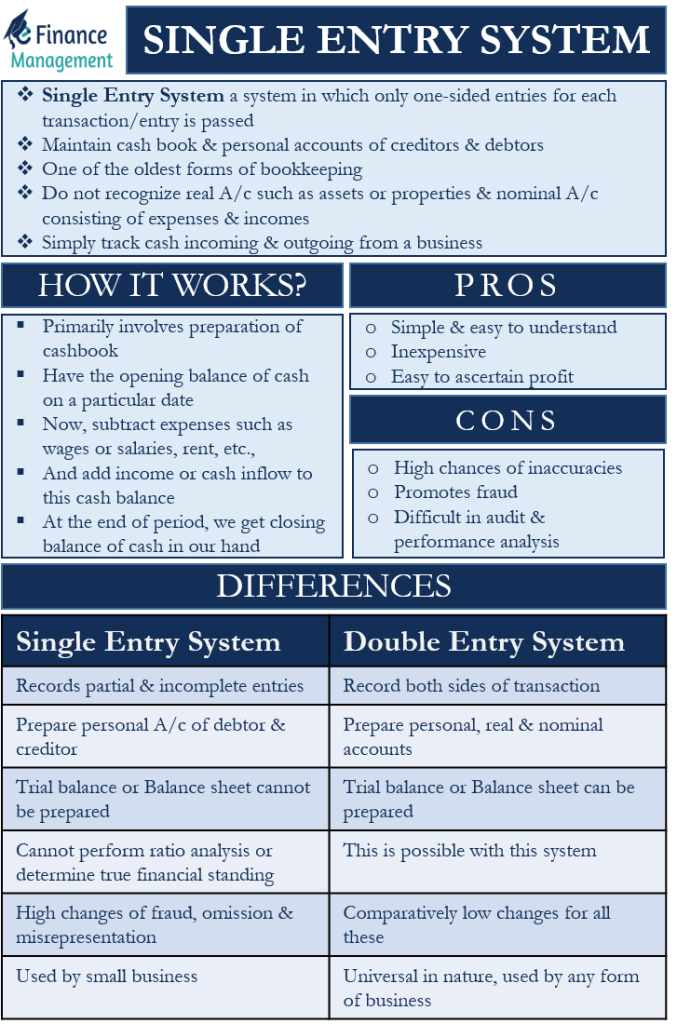

A single entry system of accounting is a system wherein only one-sided entries are passed in the books of accounts for each transaction or entry. Unlike the double-entry system, with one-sided entries, the value of only one account increases or decreases with every transaction in this system. However, there are a few exceptions to this. That we will touch upon later. In this system, the firms maintain only a cash book and the personal accounts of creditors and debtors. We record every single transaction under their heads, and their value keeps going up or down. This is one of the oldest forms of bookkeeping.

In a single entry system, we do not recognize the real accounts such as assets or properties. Also, we do not recognize the nominal accounts consisting of expenses and incomes. This is cash oriented system and thus simply tracks the cash and its inflow or outflow, to and from the business. It is a simple form of bookkeeping with very few rules and regulations to follow. Hence, it is of use for small businesses which have a limited number of transactions over the year. Also, this system requires just basic training for usage and is not costly to implement because there is no need for any expensive accounting software.

How does the Single Entry System of Accounting Work?

As we discussed above, this accounting system primarily requires the preparation of a cash book. The firm will have the opening balance of cash on a particular date. We subtract the expenses such as wages or salaries, rent, etc., and add the income or cash inflow by way of business activities to this cash balance. At the end of the period, we can calculate the closing balance of cash in our hands.

A single entry system of accounting does not necessarily imply that we pass only a single entry for every transaction. There are transactions in which we may pass both sides of the entry. For example, when we receive cash from a debtor, we record it in the cash account as well as the account of the respective debtor.

Also Read: Double Entry System of Bookkeeping

However, we may not record the complete entry in many instances under this system too. While making a cash purchase, we simply deduct the purchase amount from the cash balance. Furthermore, there are instances where we do not pass any entry at all in the single entry system. For example, we do not pass any entry to record bad debts, depreciation, or amortization expense. Hence, the entries in this system may be incomplete. We will not be able to prepare a trial balance which can increase the chances of mistakes and fraud.

Thus, the single entry system of accounting can help in finding out the profit and loss of the business over some time. But due to the recording of partial transactions or not recording some of them at all, we will not be able to prepare the Balance sheet of the firm.

Example

Let us understand the concept of the single entry system with the help of the following cash book.

Suppose the opening balance of cash in hand as on 01/07/22 is $5000. The income (Sales) over the month is $500 which we add to our cash balance. The expenditure over the month is $2200 which we deduct from our cash balance. Hence, the closing balance of cash in hand as on 31/07/22 works out to $3300.

| Date | Particulars | Income | Expenditure | Balance |

| 01-07-22 | Balance b/f | $5000 | ||

| 02-07-22 | Rent Payment | $1000 | $4000 | |

| 06-07-22 | Sales | $500 | $4500 | |

| 10-07-22 | Repairs and maintenance | $200 | $4300 | |

| 20-07-22 | Printer purchase | $1000 | $3300 | |

| 31-07-22 | Closing Balance | $3300 |

Differences between Single Entry and Double Entry System of Accounting

- A single entry system of accounting usually records partial and incomplete entries. However, we record both sides of a transaction in a double-entry system.

- We only prepare the personal accounts of debtors and creditors in the single entry system of accounting. We prepare all three types of accounts in the double entry system- personal, real as well as nominal accounts.

- We cannot prepare a trial balance or a Balance sheet in a single entry system. Hence, taxation authorities do not accept books of accounts based on this accounting system. They require books of accounts that follow the double entry system of accounting.

- We cannot perform ratio analysis or determine the true financial standing of a business that uses a single entry system of accounting. Ratio analysis, as well as complete financial scrutiny, is possible by using a double entry system of accounting.

- Chances of fraud, omissions, and misrepresentation are high in the case of a single entry system because of incomplete entries. However, this is rarely possible in the case of a double entry system of bookkeeping. Moreover, frauds and errors, if any, can also be traced during the auditing of the books of accounts.

- We can use the single entry system only in small businesses with a few transactions. The double-entry system of bookkeeping is universal. It can be used in any form of business or company.

Advantages of Single Entry System of Accounting

Simple and Easy to Understand

This system is extremely simple and easy to understand and interpret. Even a layman can record the entries by using this system of accounting. There are no complex procedures to pass the entries. We do not have to match every ledger or prepare the trial balance, and the balance sheet like in the double-entry system. Hence, it is very useful for small businesses and sole proprietorships.

Also Read: Journal Entry

Inexpensive

The system is very simple and has no strict rules and regulations. Hence, the requirement of a specialist or professional is not there for the preparation of books of accounts in this system. Also, we do not require expensive accounting software to record business entries. This can help small businesses to save a lot of money over some time.

Daily Recording of Cash Inflow and Outflow

We daily record the cash inflow and outflow from the business in the single entry system. Hence, we are always aware of our cash in hand. Also, it is very easy to ascertain the profit and loss from the business in this system.

Limitations of Single Entry System

High Chances of Inaccuracies

The biggest disadvantage of the single entry system of accounting is that there is always a high chance of inaccuracy in the books of accounts. There is a partial or incomplete entry of transactions. The individual ledgers will never match or may give wrong balances. We cannot prepare a trial balance and the Balance sheet because of which we can never be certain of the accuracy of our books of accounts.

Promotes Fraud

The single entry system of accounting promotes fraud and misappropriations within a business organization because of partial and incomplete entries. For example, there is no record of assets which can result in them getting stolen.

Audit and Performance Analysis

It is impossible to audit the books of accounts in the single entry system of accounting. An auditor will have to first convert the entries into a double-entry system, balance every ledger and then audit the books of accounts.

Moreover, the management cannot analyze the performance of the business due to the absence of all the accounts and the balance sheet. We cannot do a ratio analysis. Hence, it cannot effectively take measures for the betterment of the business and improving it.

Conclusion: Single Entry System of Accounting

The single-entry system of accounting is simple to use and easy to understand. It can give us the answer to some important metrics such as the cash in hand and the profit or loss situation of the business. It is good for small businesses with a limited number of transactions and entries. For big corporates and a large number of transactions definitely it falls short of too many important aspects. There the Double Entry Accounting System has a clear edge over it.