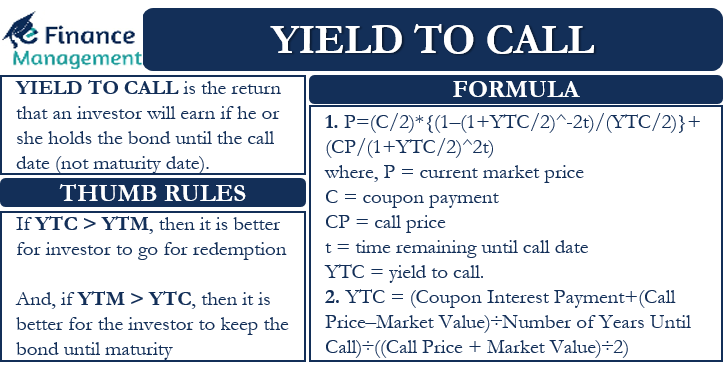

Yield to Call or YTC is the return that an investor will earn if they hold the bond until the call date (not maturity date). A call date is usually before the maturity date. YTC only occurs in the case of the callable bond. A callable bond is an instrument that an issuer can redeem or call or pay before the maturity date.

An issuer usually calls back the bonds when there is a drop in the interest rate. This allows the issuer to issue new bonds at less coupon rates.

Some types of callable bonds can be redeemed at any time. However, most of the time, the issuer gives the timeline for calling the bonds back at the time of the issue. And then, such callable bonds can be recalled only after a certain period and during the pre-defined time period. A callable bond usually carries more yield than a non-callable bond because the former carries the risk of being called back. Moreover, the call will be when the prevailing interest rate is lower than the coupon rate of the bonds. This implies that the investor will have to redeploy the proceeds at a lower rate of interest.

One can easily calculate the YTC by arriving at the interest rate:

- at which the present value of a bond’s future coupon payments/interest payments,

- as well as the call price (it could be FV of the bonds or sometimes some premium), equals the current price of the bond.

- A point to note here is that bonds always do not trade at their issue price or FV. Hence, to get an effective yield, we need to consider the bond’s current market price. Further, this price needs to be adjusted for the accrued interest, if any.

Understanding Yield to Call

The calculation of YTC takes into account three sources of potential return. These are 1. the interest payments; 2. capital gains: if there is redemption at a premium or the current price of the bond is lesser than the Face Value/Issue Price; 3. and the return from reinvestment of the redemption proceeds.

Many experts believe, and that may not be true also to assume that the reinvestment of the redemption proceeds can happen at the YTC interest rate level. Because yield to call depends upon various factors, premium if any on redemption, issued at discount or premium, the prevailing market price of the bonds, the strength of the Issuer Company, time horizon leftover with the investor, liquidity, and overall sentiments prevailing in the economy and so on.

The YTC calculation makes two more assumptions. The first is that an investor holds the bond until the call date. And the second is that the issuer redeems the bond on a pre-decided date/time period.

At any price, the true yield of a bond is generally less than its yield to maturity. This is because the call feature puts a limit on the bond’s potential price appreciation. In the situation of dropping interest rates, the price of a bond will not go over the call price.

Thus investors start to consider lesser of the YTC and YTM (yield to maturity) as a realistic indication of the return to expect on a callable bond. A few investors try to get a bit smarter by calculating the YTC for not just one date but for all the possible call dates. They then compare all the YTCs with the YTM to get the lowest of all. This lowest yield is the yield to worst or YTW.

There are a couple of rules of thumb that investors should follow:

- If YTC is more than YTM, then it is usually better for the investors to go for the redemption.

- And, if YTM is more than YTC, then it is usually better for the investor to keep the bond until maturity. This is, however, subject to the liquidity and time horizon available with the investor.

Yield to Call Formula

The formula to calculate the YTC may look quite complex. But once you understand the concept and calculation, it becomes quite easy.

Following is the formula to calculate YTC:

P = (C / 2) x {(1 – (1 + YTC / 2) ^ -2t) / (YTC / 2)} + (CP / (1 + YTC / 2) ^ 2t)

Here P is the current market price, C is the coupon payment, CP is the call price, t is the time (years) remaining until the call date, and YTC is the yield to call. A point to note is that time remaining for maturity is not needed for the calculation.

Using the above formula, we can not calculate the YTC directly. Instead, we have to follow an iterative process to get the YTC. But, if we use excel or any software for the calculation, we can directly solve for YTC.

Let us work with an example to simplify this complex calculation. Suppose a 10% coupon rate bond with a face value of $1,000 pays coupon semiannually. The current price of the bond is $1,175. It comes with a call option at the end of five years at $1,100.

Now, putting the values in the formula:

$1,175 = ($100 / 2) x {(1- (1 + YTC / 2) ^ -2(5)) / (YTC / 2)} + ($1,100 / (1 + YTC / 2) ^ 2(5))

This we get the YTC as 7.43%.

Another Formula to Calculate YTC

There is also a direct formula to calculate the YTC, and it is:

YTC = (Coupon Interest Payment + (Call Price – Market Value ) ÷ Number of Years Until Call ) ÷ (( Call Price + Market Value ) ÷ 2)

Let us take a simple example to understand the calculation. Suppose the current price of the 7% bond with a face value of $10,000 is $9,000. The call premium is 102%, and there are five years to call. This bond makes two coupon payments a year. So, the total annual coupon payment will be $1,400.

Now, putting the values in the formula:

YTC = ($1,400 + ($10,200 – $9,000 ) ÷ 5 ) ÷ (( $10,200 + $9,000 ) ÷ 2 ) = 5.4%

Another way to calculate the YTC is to use the formula for YTM and make some adjustments to it. We need to replace the maturity value with the call value in the YTM formula. Also, we need to consider only those coupon payments that the holder expects to receive by the call date.

So, the final formula will be:

Market Price of Bond = Coupon payment × (1 − (1+r)^n)/r + Call Price/(1+r)^n

Final Words

Yield to call is an important concept that helps investors to prepare for the volatility in the interest rate. Though its calculation is on the basis of the first call date, many investors calculate it for all possible call dates. And then use those YTCs to come up with the worst outcome to decide whether to invest or not in such bonds at the time of issue or for subsequent investment.