What is Sharpe Ratio?

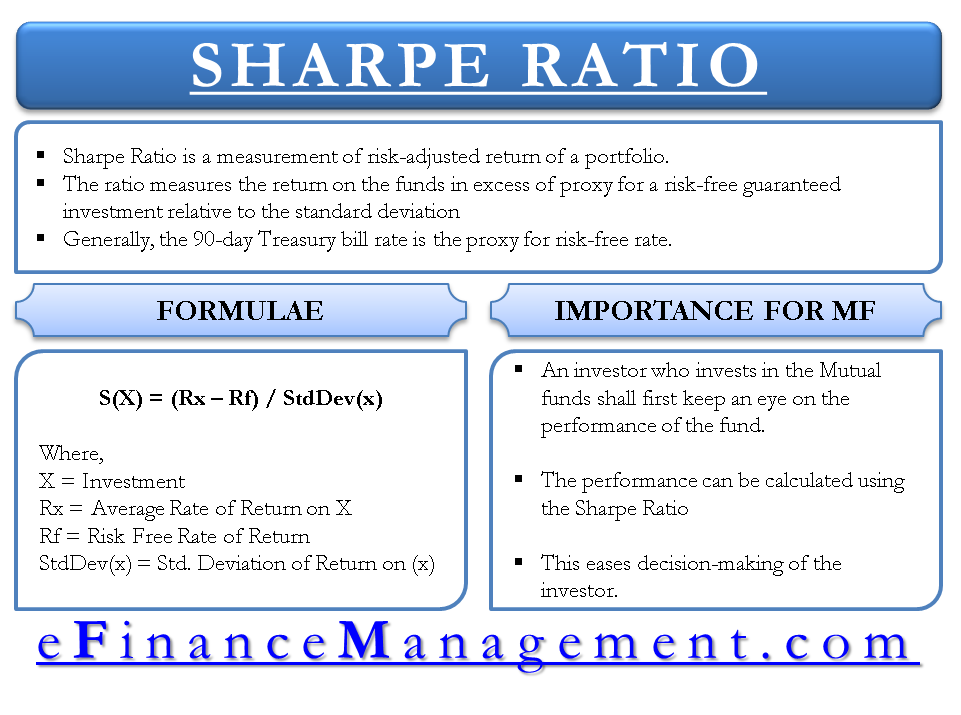

Sharpe Ratio is a measurement of the risk-adjusted return of a portfolio. The concept is named after William F. Sharpe of Stanford University. The ratio measures the return on the funds in excess of proxy for a risk-free guaranteed investment relative to the standard deviation. Generally, the 90-day Treasury bill rate is the proxy for the risk-free rate.

A portfolio with a higher Sharpe ratio is superior to its peers. Among the many available formulas, mutual fund managers use this ratio to measure the risk-adjusted returns on their portfolios.

The ratio gives the investor an idea of how much extra returns he is earning in the volatile market for holding a riskier asset. The whole idea behind calculating this ratio is to know an investor’s compensation for the additional risk he is bearing for not holding a risk-free asset.

Let us have a look at the formula of this ratio.

Sharpe Ratio Formula

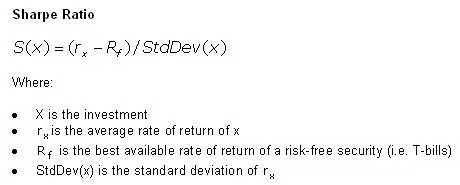

William F. Shape developed this formula. The formula is as follows.

Sharpe Ratio = (Mean Portfolio Return − Risk-Free Rate) / Standard Deviation of Portfolio Return

Note: The formula image is taken from Investopedia.

Example of Sharpe Ratio

ter is the portfolio. Hence, the second portfolio will give higher returns.

Suppose there are two portfolios: Portfolio A and Portfolio B

The details of both the portfolios are as follows:

| Particulars | Portfolio A | Portfolio B |

| Average return (Rp) | 15% | 12% |

| Risk-free rate (Rf) | 6% | 6% |

| Standard deviation (σ) | 6 | 3 |

Sharpe’s Ratio of Portfolio A = (15 – 6) / 6 = 1.5

Sharpe’s Ratio of Portfolio B = (12 – 6) / 3 = 2

Interpretation

A higher Sharpe Ratio is always considered better. In the example above, A has a ratio of 1.5 while that of B is equal to 2. Hence, portfolio B is better than A as it has a higher Sharpe Ratio. A higher ratio signifies higher returns.

Also Read: Sharpe Ratio Calculator

For calculation, you can use Sharpe Ratio Calculator.

Let us now understand the importance of the Share ratio formula for Mutual Funds.

Importance of Share Ratio Formula for Mutual Funds

An investor who is keen to invest in Mutual Funds shall always look at the performance of the funds first. The performance of the funds is measured using this ratio. This ratio gives the investor the exact information about which Mutual Fund has the best performance among the options available. This eases the decision-making of the investor. The comparison between different Mutual Funds can be made by checking this ratio of the different funds. The Higher ratio represents higher returns for every unit of risk.

Conclusion

Sharpe ratio is one of the most important tools to measure the performance of any fund or investment. The investors get the real benefit from using this ratio. Based on this ratio, the investor can determine whether the fund meets his requirements or not. The use of this ratio is all over the globe and investors should use it for their benefit. This ratio helps in getting the right analysis of the funds and enhancing the returns on investment. Also, there could be times when this Sharpe ratio can turn negative. One should also have clarity about how to deal with a negative Sharpe ratio.

Also, learn about advantages and disadvantages of the Sharpe ratio.

Hi Sanjay looking at the yahoo finance screen for let say amzn where can I find the Sharpe Ratio figure.Thanks.