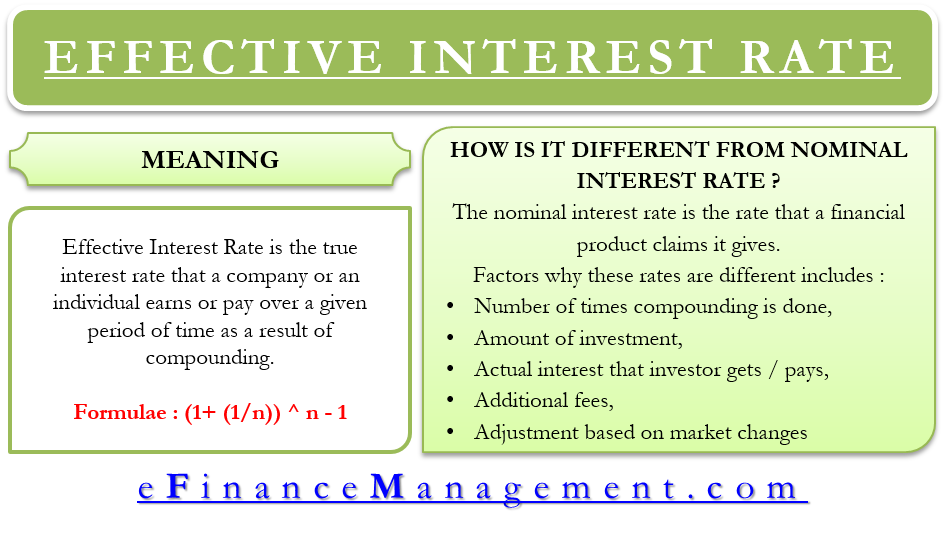

Effective Interest Rate is the true interest rate that a company or an individual earns or pays over a given period of time as a result of compounding. It could be an interest rate on an investment, a loan, or any other financial product.

One can also call such a rate as the effective rate, annual equivalent rate, discount rate, the internal rate of return, yield to maturity, market interest rate, required interest rate, and the annual percentage rate (APR).

Effective interest rate is a crucial term in finance as it helps to compare varying financial products that calculate interest on a compounding basis. These financial products can be lines of credits, loans, or investment instruments such as deposit certificates.

How it’s Different from Nominal Interest?

The nominal interest rate is the rate that a financial product claims it gives. For example, if a fixed deposit (FD) offers 8% interest, this 8% is the nominal interest rate. An effective rate may differ from the nominal rate due to several factors. These factors are:

Also Read: Effective Annual Rate (EAR)

- The number of times the compounding is done for that financial product.

- The amount that an investor pays.

- Actual interest that the investor pays or gets.

Apart from these, there are more factors that can impact the effective interest rate to an even bigger extent. These are:

Additional fees: the product may require the investor or borrower to pay some hidden fees. The inclusion of such fees in the calculation may alter the effective rate.

Adjusting amount on the basis of market rate: if an investor believes that the market rate for a product is more or less than the nominal interest rate, they can bid less or more than the face value of the debt. For instance, if the market rate is higher in the case of the loan, then the borrower pays less for the debt. This results in a higher effective yield.

For example, assume a $1000 bond pays 5% or $50 per year till the lifetime of the bond. If, after a year, the market interest rate rises, say 6%, then the 5% bond will lose some of its value because a similar $1000 bond is giving 6% now. So, an investor will go for the 5% bond only if its effective rate is 6%, i.e., they will pay less than $1000 for the same 5% bond now.

Formula

One can calculate the effective rate by taking the nominal rate and then adjusting it for the number of compounding periods. The formula for calculating the effective interest rate using the nominal rate is

Effective Annual Interest = (1+ (1/n)) ^ n – 1

Here ‘i’ is the nominal interest rate, and ‘n’ is the number of compounding periods.

It is a general rule that as the number of compounding periods increases, the effective annual interest rate also rises. For instance, quarterly compounding gives a higher return than the semi-annual compounding, while monthly compounding gives more return than the quarterly. Similarly, daily compounding produces a higher return than monthly.

Also Read: Effective Annual Rate Calculator

Though the effective rate increases as the number of compounding periods increases, there is a limit to this. Even if one tries to compound infinite times, i.e., every second or microsecond, the limit will be hit. For calculating the continuously compounding effective annual interest rate, we raise the number “e” to the power of the interest rate. The number e equals to 2.71828.

For example, for a 10% rate, the continuously compounding effective annual interest rate would be 10.517%. In comparison, the daily compounding is 10.516%, while monthly is 10.471%.

Why it’s Useful?

To demonstrate the usefulness of the effective rate, let us take an example. Suppose John invests money in an investment (A) that pays him 10% compounded monthly and an investment (B) that pays him 10.1% compounded semi-annually. From the outset, investment B seems more profitable, but calculating the effective rate will tell the real thing.

The effective interest rate for investment A is 10.47%, while for investment B is 10.36%. So, on the basis of interest rate, investment A is more profitable.

When Banks Use Don’t Use Effective Rate?

When you apply for a loan, banks or other financial organizations use the nominal interest rate, not the effective rate. They do this to make you believe that you are paying a less interest rate. For instance, a loan that the bank says is at 12%, but when compounded monthly, the effective rate will be 12.69%

On the other hand, when banks pay interest on deposits, they usually advertise the effective annual rate. The reason they do this is the same – the effective rate in deposit looks more attractive than the nominal one.

Read Types of Interest Rates to learn more about different types of interest rates.