In the financial world, the term Fair Value (FV) is used when talking about investing and accounting. When talking about investing, it means the price of the asset that the buyer and seller agree on. In terms of accounting, it means taking the assets and liabilities at the current market price and not at the book value.

Let’s talk about each one in detail.

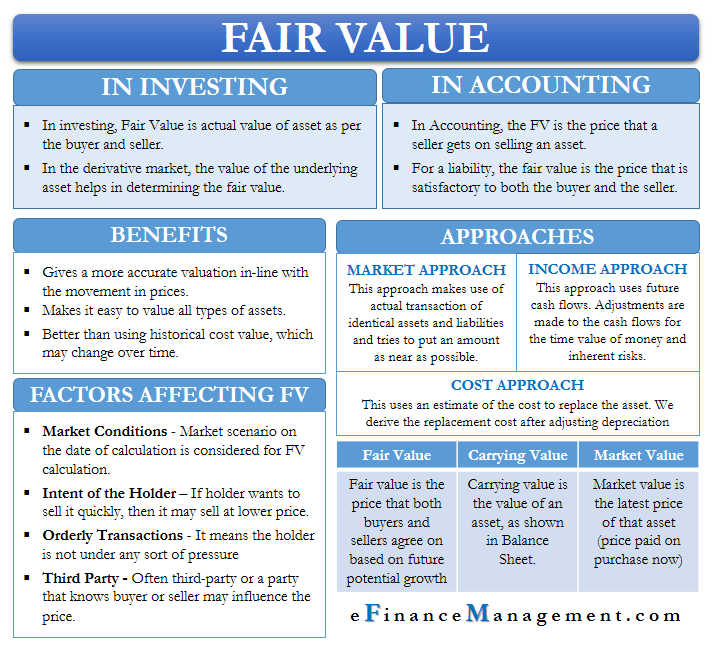

Fair Value in Investing

It is the actual value of an asset as per the buyer and seller. The asset in question could be anything a product, stock, or security. It is the value that both buyer and seller feel appropriate, i.e., both parties stand to benefit.

In the investing world, one of the best ways to arrive at the FV is to list it on a public marketplace, such as a stock exchange. On a stock exchange, the price of a security moves based on the demand and supply of that security.

In the derivative market, the value of the underlying asset helps in determining the fair value. For instance, if you buy a $10 call option for Company A stock, then you have the right to purchase the shares at $10. If the price of Company A shares rises, the value of the option would also increase.

Similarly, the fair price in the futures market is the equilibrium price for a futures contract. The equilibrium price is when the supply and demand are equal. It is similar to the spot price after including the compound interest.

Even though the price of a security on an exchange seems to be the fair value, in reality, it may not be. Thus the buyer needs to find out the FV on their own. There are several ways to find the value of a stock, but one of the best valuation methods is DCF (Discounted Cash Flow). DCF attempts to calculate/derive the present value of all estimated future free cash flows. Though there is a formula for DCF, however, calculating fair value through it is both a science and an art. It is because it involves the analyst taking assumptions to arrive at a fair value.

Fair Value in Accounting

As per IASB (International Accounting Standards Board), the FV is the price that a seller gets on selling an asset. For a liability, the fair value is the price that is satisfactory to both the buyer and the seller. In a mark-to-market valuation, a company must list its assets and liabilities at fair value.

In accounting, we also use FV at the time of consolidation. We use this value when we consolidate the accounts of the subsidiary with that of the parent company. Similarly, when a company buys a stake in a subsidiary, accountants value the asset and liabilities of the subsidiary at fair value.

Also Read: Value of a Firm

It may get challenging for an accountant to arrive at a fair value in some cases. It could be because there is no active market for that asset. In such a case, the accountant can make use of valuation techniques, such as DCF, to come up with a fair value.

Fair Value Accounting – Benefits

Following are the advantages of using the FV in accounting:

- It gives a more accurate valuation that is in line with the movement in prices as they go up and down.

- The value of a total asset reflects the real financial strength as well as the income status of a company. This means that one doesn’t need to look at the profit and loss report; instead of, looking at the actual value will give the information.

- It makes it easy to value all types of assets.

- It is better than using historical cost value, which may change over time.

- It is a better approach during a crisis as it allows asset sales and, thus, the generation of funds.

Factors Affecting

The following factors affect the FV in accounting:

Market Conditions – a market scenario on the date of calculation and not at the time of historical transaction affect the value.

The intent of the holder – for example, if the holder wants to sell an asset quickly, then they may be ready to get a lower price of the asset.

Orderly transaction – such transaction leads to fair value. It means the holder is not under any sort of pressure, such as liquidation, to sell the asset, and so no depressed value factor comes into play.

Third-Party – the fair value is the price at which both the buyer and seller agree. However, a third party or a party that knows the buyer or seller may often influence the price.

Approaches to Fair Value

Three general approaches help to derive the fair value:

Market Approach – This approach makes use of the actual transaction of identical or similar assets and liabilities and tries to put an amount as near as possible to the same asset.

Income Approach – This approach uses future cash flows. Adjustments are made to the cash flows for the time value of money and inherent risks.

Cost Approach – This uses an estimate of the cost to replace the asset. We derive the replacement cost after adjusting the asset value for scrap and obsolescence, i.e., depreciation.

How to Determine (Levels)?

GAAP (Generally Accepted Accounting Principles) lays down levels of information sources, ranging from Level 1 to Level 3. These tell the ways to determine the fair value and also the method that is preferable (Level 1). Following are those levels:

Level 1

Under this, the accountant uses the price of identical assets and liability in the market. The market that an accountant observes must be active, meaning the volume of transactions should be substantial. Stock exchanges are the best example of an active market.

Level 2

Under this, the accountant observes similar assets and liabilities in the active or inactive markets, for example, by using the value of a similar building in the same area to get the value.

Level 3

If the information from the above two levels is not available, then an accountant can use valuation techniques to estimate the value. The valuation under this could be highly subjective. A company may use its data along with any other readily available information.

Fair Value vs. Carrying Value vs. Market Value

- Fair value is the price that both buyers and sellers agree on. To calculate the fair value, one needs to consider future growth potential, risk factors, etc.

- Carrying or the book value is the value of an asset, as is shown in the balance sheet. It is not the original purchase price but rather the price after adjusting for depreciation and impairment expenses plus any improvement thereon. Or, we can say the carrying value is the value of an asset after several years.

- Market value is the latest price of that asset. Or the price you will pay if you purchase a new asset now. The market value determines the supply and demand factors, but it usually fluctuates more than fair value.

Final Words

We now know that the best way to get the FV is to look for the same or identical asset in the active market. An active market is one where buyers and sellers frequently buy and sell that asset. A busy market sees a high volume of transactions and in turn, ongoing pricing information.