What is Transfer Price?

Transfer Price is the price that related parties charge to each other. In simple words, we can say it is the price at which different departments in a company transfer goods to each other. Transfer pricing comes into play when various departments in a company operate as separate entities.

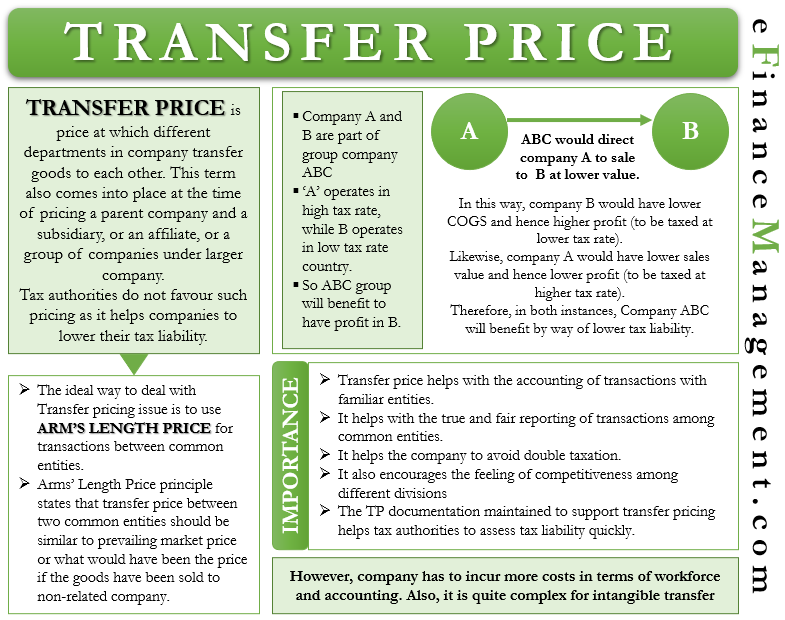

It is the pricing between different departments in a company, or a parent company and a subsidiary, or an affiliate, or a group of companies under a larger company.

Transfer pricing is useful for tax purposes and thus, results in tax savings. Tax authorities do not favor such pricing as it helps companies to lower their tax liability. Transfer pricing exploits the loopholes in the tax system in different countries and thus is subject to heavy scrutiny from the tax department. With such pricing, a company aims to book more profit in countries with lower tax rates.

Example

Suppose there are two associate companies, A and B, and both are part of a bigger company ABC. Company A operates in a country with a high tax rate, while Company B works in a low-tax rate country. In this case, it will benefit Company ABC to have more profits with Company B. This would help to bring down the tax burden.

For this, Company ABC may direct Company A to charge a lower transfer price when dealing with Company B. In this way, Company B will have a lower cost of goods sold (COGS) and, in turn, more profits. On the other hand, Company A will have less revenue and, thus, lower earnings. Therefore, in both instances, Company ABC will benefit by way of lower tax liability.

International tax laws fall within the ambit of OECD (Organization for Economic Cooperation and Development). The auditing companies or auditors under the OECD audit the financial statements of MNCs.

Arm’s Length Dealing Principle

The ideal way of deciding the transfer pricing is using the Arm’s Length Principle. During scrutiny by regulatory authorities, the prices are tested concerning this principle. This principle provides that the transfer pricing between two common entities must be treated as transactions between two different companies. In other words, we can say the transfer price between two common entities should be similar to the prevailing market price or what would have been the price if the goods have been sold to some other non-related company. The Arm’s Length Principle ensures that governments get their due taxes. Also, it makes sure that a company is not a victim of double taxation.

For example, Google has a regional headquarters in Singapore and a subsidiary in Australia. For the year 2012-13, the Australian arm made a profit of $46 million on revenues of $358 million. But, Google paid AU$7.1 million in tax, including a $4.5 million tax credit. Clarifying why it didn’t pay more taxes, the company said the taxes attributable to the Singapore headquarter were paid in that country.

Also Read: Tax Due Diligence

Transfer Price – How it Works?

As said above, a company needs a transfer price when dealing with the divisions, its subsidiary, or an affiliate. When these entities transact with each other, they use transfer prices to determine their costs. Generally, a transfer price should not be very different from the market price. If there is a big difference, then it is possible that one side is at a disadvantage, or it is to avoid taxes.

Regulations, however, are in place to check and stop the misuse of the transfer pricing mechanism. These regulations mostly work on the principle of arm’s length transactions. It means that companies must determine the transfer price on the same guidelines; it determines the market price when dealing with the outside parties.

The financial reporting of a company helps to keep a check on the transfer pricing. A company using transfer pricing needs to maintain all documents and mention them in the footnotes in the financial statements. It allows auditors, regulators, and investors to review such transactions. If found inappropriate, a company can be made liable to pay fines and more taxes.

Transfer Price – Objectives and Importance

The following points highlight the objectives and importance of the transfer price:

- As said above, a company can easily avoid a large amount of tax by using transfer pricing. A company does this by transferring the value of the products to a company or subsidiary operating in a country with a lower tax. Moreover, even within the same country, a company can use transfer pricing to avoid tax liability.

- A company may also use transfer pricing to shift profit from one jurisdiction to another. Moreover, this pricing could also help a company if it wants to make one of its subsidiaries or affiliate look more profitable.

- A transfer price is also essential to come up with a fair and equitable price when the transaction takes place between two common entities.

- Transfer price helps with the accounting of transactions with familiar entities. It, in turn, helps to determine their profit or loss.

- It also helps with the true and fair reporting of transactions among common entities.

- Such pricing also helps the company to avoid double taxation.

- It also encourages the feeling of competitiveness among different divisions as they are aware of the revenues they are generating and the cost they are incurring.

- The documentation that a company maintains to support transfer pricing helps the tax authorities to assess the tax liability quickly.

Importance of Transfer Price

Let’s try to understand the importance of transfer price with the help of an example.

Assume there are two companies, X and Y. Both these firms belong to XYZ. Company X makes mobile in Malaysia, while Company Y sells those in Hong Kong. The market demand and supply determine the selling price of the mobile. However, Company XYZ does have control over transactions between X and Y.

Even though both companies belong to XYZ, both have their entity as well. So, the sale price does impact their financial results. Meaning, if Company X charges more for mobile, it makes more profit, and Y makes less profit and vice versa.

However, it does not matter which of the two makes more profit for XYZ. In both cases, the results will be better for XYZ. Even for the shareholders of XYZ, it doesn’t matter which of the two makes more profit. But, for tax, it matters which of two makes more profit.

Company X operates in Malaysia, where the corporate tax rate is 25%, while in Hong Kong, the tax rate is 15%. To maximize its profit, Company XYZ can use its control to influence the transfer price between X and Y. It will direct X to transfer mobiles to Y at a lower price. In this way, Company X will make less profit, hence less tax liability. Company Y will make more profit, but since the tax rate on Hong Kong is less, the tax liability comes down.

Risks

The following are the risks of using transfer pricing:

- Often there could be a disagreement among departments or subsidiaries over the rules governing transfer pricing.

- For proper implementation of the transfer pricing, a company needs to incur more costs in terms of workforce, accounting system, and more.

- Using transfer pricing for intangible products could be complex.

Final Words

As with any other concept, transfer price also has its benefits and limitations. It helps to reduce uncertainty in pricing when dealing with related parties. On the other hand, a company can also misuse it for tax evasion.