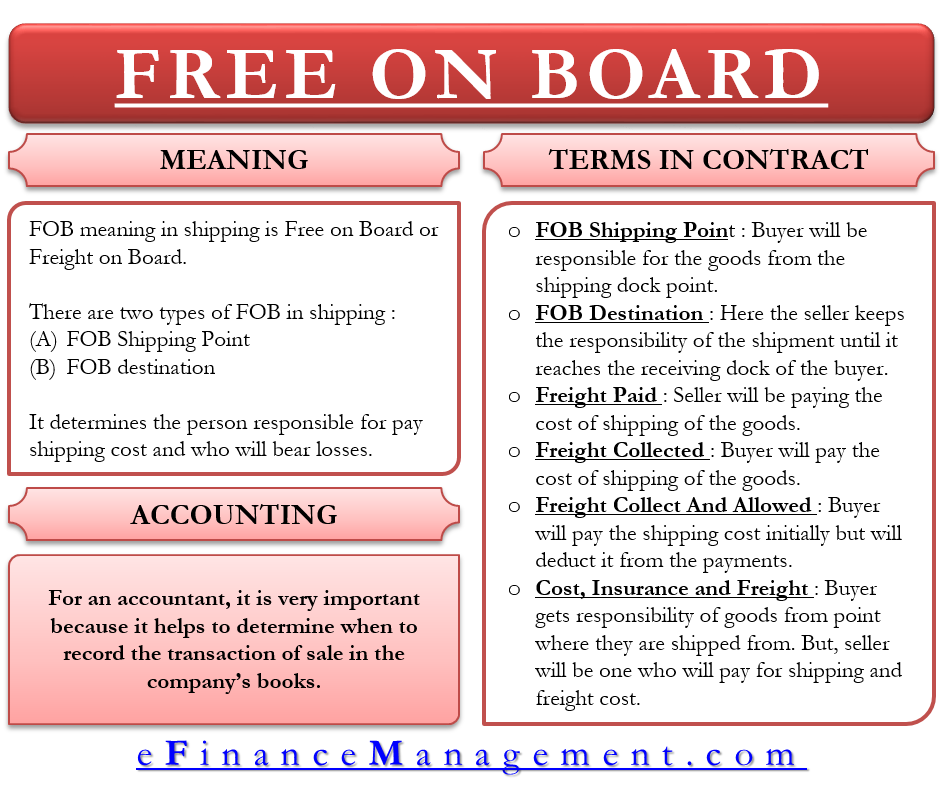

FOB, meaning in terms of shipping, is Free on Board or Freight on Board. There are two types of FOB in shipping. The first one is the FOB shipping point, and the second one is the FOB destination. The difference between these two is a very big deal in the business world because it determines the person responsible for paying shipping costs and the person who will bear the losses in case of loss, damage, or theft.

FOB shipping point or FOB origin means that the buyer will be at risk once the seller has shipped the goods. FOB destination means that the seller will bear the risk of loss until the goods reach the buyer safely. In accounting, FOB determines when the buyers and sellers will record the purchases and sales in their book of ledgers.

History of FOB Shipping

In FOB, throughout history, is full of various different shipping terms. Initially, the meaning of FOB was freight on board. It is still in use in many parts of the world. If the goods are shipped from New Jersey as “FOB New Jersey,” that will mean that the responsibility of the seller is to get the shipment to the boat in precise order. Once the ship or vessel receives the goods, the responsibility of the seller is over. Now the goods or shipments become the responsibility of the buyer. Now, if the shipment is damaged or someone stole it, then it becomes a financial loss for the buyer, not the seller. The term FOB refers to the goods that are transported through water.

Few terms will help understand how the term FOB is used in the contracts.

Terms Used in Contracts

FOB Shipping Point

It is also termed FOB Origin. This means that once the goods leave the shipment docks of the seller, they are no longer responsible for the goods. The buyer will be responsible for the goods from that point.

For more information, read our exclusive post on FOB Shipping Point – Meaning, Example, And More.

FOB Destination

Here the seller keeps the responsibility of the shipment until it reaches the receiving dock of the buyer.

To know more about this, you can read our post on FOB Destination – Meaning, Types, Importance, And More.

Freight prepaid

It means that the seller will be paying the cost of shipping the goods.

Freight Collect

This term means that the buyer will pay the shipping cost of goods.

Freight Collect and Allowed

This term means that the buyer will pay the shipping cost initially but will deduct it from the payments while making payments to the seller.

Cost, Insurance, and Freight

This is similar to the FOB origin prepaid. The buyer gets the responsibility of the goods from the point where they are shipped from. But, the seller will be the one who will pay for the shipping cost and freight cost.

Example of FOB Origin

David’s company purchase 20,000 jars of jelly from ABC. Ltd. David pays the shipping cost, and the jars are shipped FOB ABC LTD. (also known as the FOB origin). On the way to David’s store, the truck meets with an accident that damages the jars. David tries to sue ABC Ltd., but he cannot because the title has already passed to him as soon as the jars were loaded on his truck.

Example of FOB Destination

Let us take the same scenario at a different point, i.e., FOB Destination. Here, David can sue ABC Ltd and ask for the replacement of the damaged jars because the title of the goods throughout the transit will remain with the ABC LTD. It is the responsibility of ABC Ltd. to deliver the jars safely to David.

Why does FOB Matter?

The term FOB indicates when the risk of losses shifts from the seller to the buyer. In international transactions, they are very important for the participants, especially in the case of goods that are very delicate or for items that are vulnerable to theft.

The above example shows both the cases of FOB ORIGIN and FOB DESTINATION. Both of these terms are standard and most used FOB terms. It is important to remember that under the uniform commercial code (UCC), if the purchase contract does not specify any FOB term, then it is to assume the transaction terms are of FOB origin.

FOB in Accounting Terms

For an accountant, it is very important because it helps to determine when to record the transaction of sale in the company’s books. Let’s take an example, assume there is a contract for a $300,000 shipment of precious jewelry sets. The term of the contract is FOB Origin. In this case, when the gems leave the seller’s dock, the sale is closed. The seller can enter the transaction of $300,000 in the receivable account and can deduct $300,000 from its account of Inventories. But for the buyer case is completely its opposite. Once the buyer receives the ownership, it can increase its inventory account by $300,000 and reduce the accounts payable by $300,000.

Now, if the terms of the contract are FOB destination, the same transactions will take place. But the company will record the transactions only when the goods will arrive at the receiving dock of the buyer.

The buyer or seller, whoever pays the shipping cost, will enter the transaction in its book of accounts. The physical handling, loading and unloading, transportation, shipping, and insurance costs can be included in the shipping cost. Both the buyers and sellers treat the shipping cost differently. If the shipment is of the FOB destination, the seller will treat it as the expense on the cost of goods sold. At the same time, the buyer will credit the amount in the inventory costs and then to the cost of goods sold at the time of disposal.

RELATED POSTS

- FOB Destination – Meaning, Types, Importance And More

- Cost and Freight – Meaning, Obligations, and Use

- Free Alongside Ship – Meaning, Obligations, Advantages and Disadvantages

- Free Carrier – Meaning, Obligations, Benefits, Pros and Cons

- Inland Bill of Lading – Meaning, Importance and More

- Delivered Ex-Ship – Meaning, Example, and Relevance