Double Declining Depreciation Method

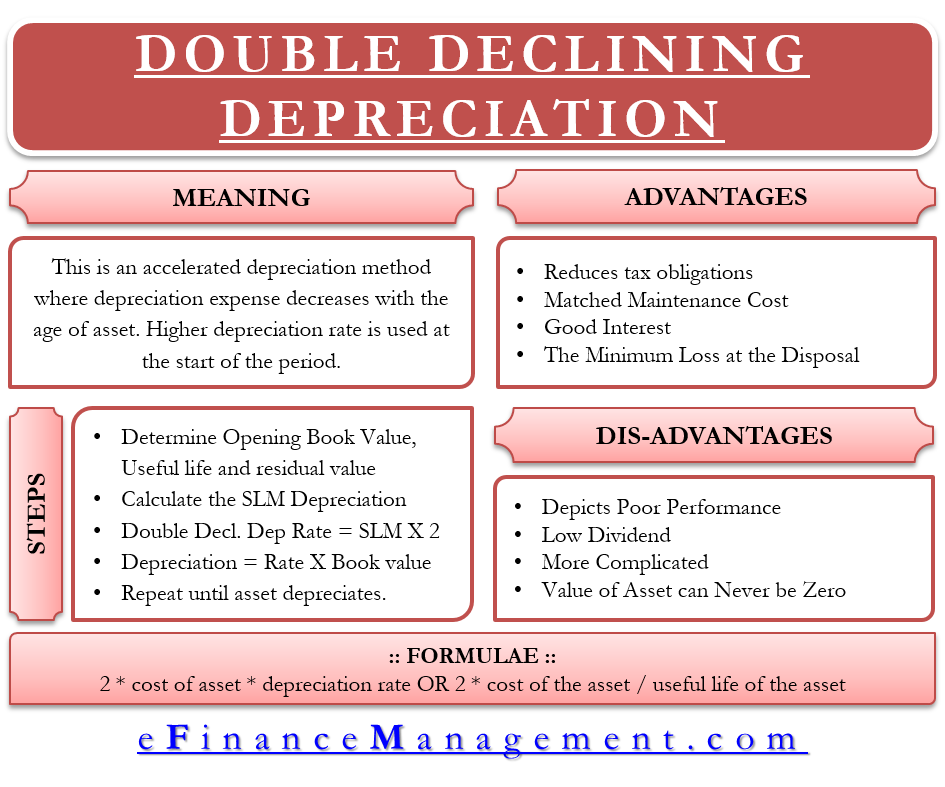

The double-declining depreciation is an accelerated depreciation method where the depreciation expense amount decreases with the age of the asset. The depreciation charge under this method is calculated by applying the higher depreciation rate to the asset book value at the start of the period.

Why do we Use Double Declining Depreciation Balance Method?

Though the straight-line method is a straightforward and popular method for calculating depreciation, there are some instances when it is not appropriate to use it.

This method assumes that an asset is more productive in its initial years, and slowly and steadily, its productivity reduces due to normal wear and tear. Thus, the asset generates more revenue in its early years. Therefore, to get the true picture of the performance of the company through financial statements, it is required to match the expenses with revenues. The double-declining method achieves this as, under this method, more depreciation is charged in the early years and gradually reduces in the subsequent years. The ratio of depreciation charged to the asset each year is the difference between the straight-line and double-declining depreciation methods. In the former, the total depreciation is equally charged every year during the lifetime of the product. While in the case of later, depreciation is charged in line with the productivity of the year.

This method is also known as the 200% declining balance method of depreciation. Here, double means 200% of the straight-line depreciation rate.

How to Calculate the Double Declining Balance Depreciation?

The formula to calculate the double-declining depreciation is:

| Double Declining Balance Depreciation = Opening Book Value of Asset * 2 * Straight-Line Depreciation Rate |

Or,

| Double Declining Balance Depreciation = Opening Book Value of Asset * Double Declining Depreciation Rate |

The calculation of the depreciation under this method is not as easy as it looks. The following is the step-by-step process for calculating depreciation under this method:

Also Read: Double Declining Depreciation Calculator

Step 1: Straight-Line Depreciation Rate

The first step towards calculating depreciation under this method is to find out its straight-line depreciation rate. For this, you have to determine the cost of the asset, its residual value, and the remaining life of the asset.

| Straight Line Depreciation Rate = (1 / Useful Life of Asset) * 100 |

Step 2: Double Declining Depreciation Rate

Calculate the double-declining balance rate by multiplying the straight-line depreciation rate by 2 (i.e., 2 * Step 1).

| Double Declining Balance Rate = 2 * Straight-line Depreciation Rate |

Step 3: Calculate Depreciation

Apply the rate (Step 2) to the opening book value of the asset at the start of each period

| Double Declining Balance Depreciation = Double-declining Balance Rate * Opening Book Value of the Asset |

Repeat until the asset depreciates completely.

And, you can also refer to our Double Declining Depreciation Calculator for a quick calculation.

Explanation using Example

Suppose that a company has purchased a machine worth $1,200,000 with an economic life of 5 years. The scrap value of the machine is $100,000.

The Straight-line Depreciation Rate = 100% / 5 = 20%

Double Declining Depreciation Rate = 2 * Straight Line Depreciation Rate = 2*20% = 40%

The depreciation using this method is:

| Year | Opening Book Value | Depreciation | Closing Book Value | Rate of Depreciation |

|---|---|---|---|---|

| 1 | 1,200,000 | 480,000 | 720,000 | 40% (480,000/1,200,000) |

| 2 | 720,000 | 288,000 | 432,000 | 40% (288,000/720,000) |

| 3 | 432,000 | 172,800 | 259,200 | 40% (172,800/432,000) |

| 4 | 259,200 | 103,680 | 155,520 | 40% (103,680/259,200) |

| 5 | 155,520 | 55,520 | 100,000 | 37.50% (55,520/155,520) |

The rate in the fifth year has decreased to 35.70% from 40% as the asset cannot be depreciated more than its scrap value. Or we can say this year’s depreciation will not exceed the residual value of the machine.

Advantages of Double Declining Depreciation Method

Reduces Tax Obligation

In the initial years, the depreciation charge is higher than in the later years. so, by adopting this method, the business can save tax by lowering its tax liability.

Also Read: Straight Line Depreciation

Matched Maintenance Cost

In the early years, higher depreciation is charged when the cost of repairs and maintenance is low. And in later years of asset life, low depreciation is charged when the cost of repairs and maintenance increases. This creates uniformity with revenues throughout the asset’s life.

Good Interest

Since depreciation is a non-cash expense, a company can invest this amount. A business generates interest when it invests the depreciation outside the business. Consequently, this helps to generate more funds to replace the asset.

Minimum Loss at Disposal

The business will have a minimum loss when the asset disposes of due to the innovation as a large part has already been changed into the profit and loss account through depreciation.

Disadvantages of Double Declining Depreciation Method

Depicts Poor Performance

The financial statements, when using this, shows the lower profit in the earlier years as the depreciation charge is higher in these years. This shows the poor performance of the business in the earlier years.

Low Dividend

Charging more depreciation reduces the net income of the company, which belongs to the shareholders. This ultimately reduces the per-share earnings and in turn dividends too. Also, lower profits will indicate that the company is not performing well.

More Complicated

The double-declining method is more complicated than the straight-line method. The calculations are to be done carefully to avoid any costly mistakes.

Value of Asset can Never be Zero

Under this method, the value of an asset can never reach zero if the asset has no residual value.