Cost Plus Contract: Meaning, Types, Advantages, Example, and More

Cost Plus Contract: Meaning

An agreement between two parties whereby one party promises to reimburse the other party for the costs incurred and any… Read Article

There are various questions and terms one comes across while learning about costing or practically conducting it. Such questions include what is cost, how is costing done, what is the basis of cost allocation, and so on. This article is all about the basic costing terms one would come across.

Cost means any type of expenditure that an entity incurs to make or sell a product or while rendering a service. Or, we can also say cost means any expenses towards getting an asset ready for normal use. There are different types of costs, but two of the most important ones are fixed and variable costs.

It refers to the system of assigning costs to the cost objects or the final products. There are various methods of costing. And which method is to be used for a particular product depends based on its method of production. For example, medicines are produced in batches; therefore, we use the batch costing method to determine the cost of medicines.

Cost accounting refers to recording the data related to costing in proper accounts. This is a useful step that helps managers in making informed decisions. (Read Types of Cost Accounting to learn more).

Read Cost, Costing, Cost Accounting, and Cost Accountancy for a more detailed article.

A cost object is anything for which the whole process of costing is done. It is anything to which the cost is assigned. Apart from the final products or services, there can be different cost objects in a company. For instance, one could measure the cost of designing a new product, the cost of each customer service call, and more.

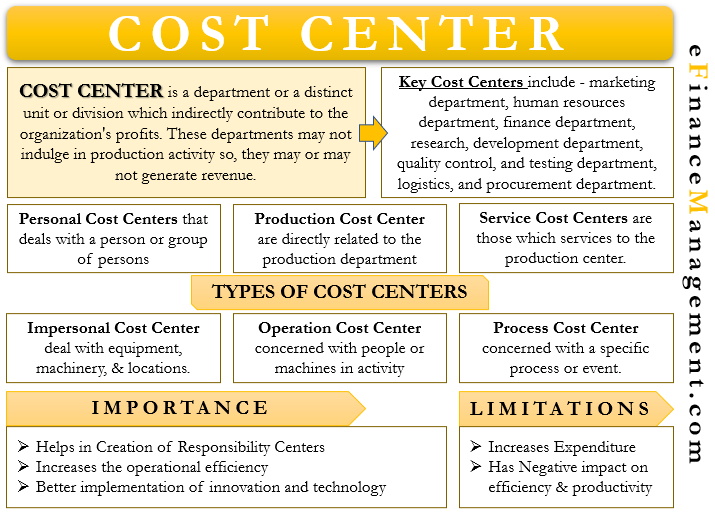

A cost center is a business unit that does not generate any revenue but does incur costs. Such business units are usually administrative departments or service centers. A company can’t eliminate such departments as they are very crucial for the smooth functioning of the company.

As the word suggests, it is a costing term that refers to the cost that drives the total or major cost of a cost object. Or, we can say it is an item that can drastically change the cost of an item. For example, the most important parameter to measure the cost of electricity is the number of units consumed. So, in this case, the number of units consumed is the cost driver. More examples of cost drivers are direct labor house, machine hours, etc.

A relevant range refers to a range within which the company’s fixed cost will not change irrespective of the change in the volume of activity. For example, Company A designs a budget with a maximum relevant sales range of $10 million. It implies that if the sales of the company exceed $10 million, then the company would have to find a new manufacturing facility.

Cost pool refers to the pooling of individual costs, such as by department. Then the company allocates the cost from that cost pool. Such cost pools come very handily when allocating factory overheads to units of production. For example, in the case of a maintenance department, a company usually accumulates its cost in a cost pool and then allocates those costs to the department that use the services of the maintenance department.

Cost estimation is a very basic costing term which means the process of forecasting and estimating costs, as well as other resources that a company needs to finish a project. Such a process helps to fix the selling price of the final product, as well as draw inventory reports. There are several methods to estimate costs, such as the expert judgment method, analogous estimating method, parametric estimating method, bottom-up estimating method, and more.

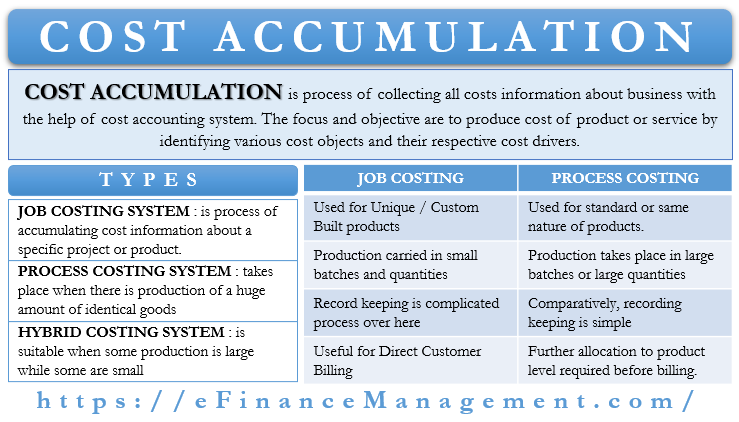

The cost accumulation process involves identifying, accumulating, and assigning costs to different cost objects. So, first, we need to identify the cost object and then identify the costs associated with that cost object. Then we need to allocate those costs to the cost object based on set criteria.

It refers to how a change in a business activity impacts the cost. Or, it means how a cost will change if there is any change in some business activity. In order to make the right business decisions, any manager needs to understand the cost behavior. Generally, there are three types of cost behavior – variable costs, fixed costs, and mixed costs behavior.

It means categorizing the cost based on activity levels. Cost hierarchy is primarily of use in ABC (activity-based costing) system. The categorization is based on how easily one can trace the activity to a product. Primarily, there are four cost hierarchy levels. These are unit level, batch level, product level, and facility level.

It refers to the proportion of fixed and variable costs that an entity needs to incur. The type of cost structure of a company directly relates to the nature of the activity. This means almost every business could have a different cost structure. For instance, some businesses will have more fixed costs; some require more working capital and more.

Cost accumulation is the process of using the cost accounting system to gather all cost information of an entity. Or, we can also say it involves collecting data of all costs that an entity incurs at every stage of production. Collecting the cost data assists management in making better business decisions.

A Price ceiling is a control mechanism that prevents the cost of a good or service from going above a certain level. And price floor refers to a mechanism to prevent the cost of a good or service from dropping below a certain level. The idea is to minimize the cost without compromising the quality of the product or service.

Pre-determined overhead rate is a pre-set rate that an entity uses to allocate estimated costs to a cost object. Such a rate helps management in quickly completing the costing job. Also, it helps to avoid preparing actual manufacturing overhead costs. Still, the company must adjust the difference between the actual and estimated allocation of overheads at the end of the fiscal year.

It is a process of developing a plan of estimated receipt and expenditures. Creating a budget allows a business to get an idea of the overall business transactions for a future period. Budgeting helps to coordinate the business activities, as well as plan the actual business operations. It also helps to motivate managers to achieve the budgeted goals.

It is the method of converting raw materials or inputs into finished goods or products. Or, we can also say that it is the method that takes and uses input to generate an output that is fit for consumption. The output is a good or product that holds value for the end-user. (Also, read Manufacturing vs. Production for more details).

Inventory means the stock held by the company for production and sales. There are various types of inventories and techniques to manage inventories.

The list of these costing terms or cost concepts is non-exhaustive.