What is Cost Driver?

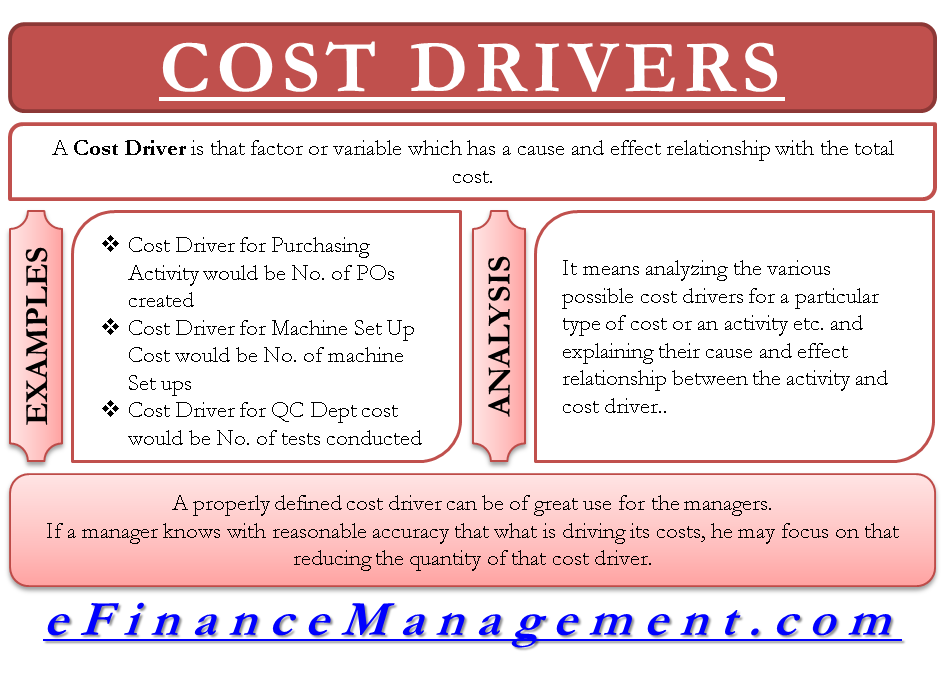

A cost driver is a basic costing term. Let’s first look at its technical definition. A cost driver is that factor or variable which has a cause and effect relationship with the total cost. The cost driver is the’ cause,’ and the ‘total cost incurred’ is its effect. If we take an example of the fuel cost of running a car, the cost driver (cause) would be ‘No. of Kms Run’, and the total cost (effect) would be ‘total fuel cost.’ The relationship is clear, the higher the no. of km run, the higher the total cost of fuel.

In simple terms, the literal definition of cost driver could be ‘the driver of cost.’ I want to state a simile here. Like a driver drives the car, a cost driver drives the cost. Let me give a simple example to clarify the point at the outset. Let’s assume labor hired for finishing a product at $5 per hour. If he works for 8 hours a day, the total cost would be $40 ($5*8). In this example, labor hours, i.e., 8, is the cost driver which was multiplied to the rate of $5 to reach a total labor cost of $40.

Most importantly, a cost driver without a cost object is vague. A cost driver is always associated with something. In our example, labor hours are the cost driver of total labor cost. Or, no. of km run is the cost driver of total fuel cost.

What is Cost Driver Rate? Calculate with Formula

Cost driver rate is the rate at which the cost driver drives the cost. Let’s continue the same example and include some additional information. Now, for finding out the total cost incurred on finishing an activity in a day, we will use the following formula:

Cost Driver Rate = Total Cost of Finishing Activity in a Day / Cost Driver Units = 40 Total Cost / 8 Hours a day = $5.

Cost Drivers and Relevant Range

Fixed costs like the yearly rent of a factory can’t have a cost driver simply because the factory rent would not increase with an increase in production, especially in the short run like a year or 2. But, if we consider a long term of 10 years, we may find some co-relation with production. In the long run, we can assume the quantity of production as a cost driver for factory rent. Here, the concept of the relevant range comes into play. Fixed costs remain fixed until a range of activity, and then they shoot up to a different level. For example, this business may increase the area of the factory to 1.5 times, and rent increases from $100,000 to $150,000. There is a possibility that for some time, a part of the factory remains unutilized.

Activity Cost Driver and ABC Costing

Cost driver has great relevance in Activity Based Costing. ABC Costing is a method of costing, which is famous for more scientifically absorbing the overheads / indirect costs. For this, the whole process of manufacturing is divided into activities. Cost accumulates into these activity cost pools. Each activity cost pool is then assigned an Activity Cost Driver. With the help of these drivers, the cost is allocated to products. Cost driver analysis is the key to utilizing the concept of ABC Costing to its full potential. Correct activity cost driver determination is vital for effective product costing. There are a lot of management decisions that rely on product costing.

Examples of Types of Cost Drivers

There cannot be an exhaustive list of cost drivers and activities. Some of the common examples of cost drivers are as follows:

| Department / Cost Centre / Cost Pool / Activity | Cost Drivers |

| Purchase department or Purchasing Activity | No. of Purchase Orders created. |

| Set Up Cost for Machine | No. of Machine Set-Ups |

| Repairs and Maintenance of Machines | No. of Machine Hours Run |

| Quality Check Department or Cost | No. of Tests conducted |

Cost Driver Analysis

Cost driver analysis means analyzing the various possible cost drivers for a particular type of cost or activity etc. and explaining their cause and effect relationship between the activity and cost driver. It is advisable to use the most correlated cost driver for making any decisions relating to apportionment of cost, reduction of costs, etc. But, one should note that correlation is just a way to prove the relationship. Ultimately, the cause and effect relationship is a must. Just for example, usually, material cost and labor cost will correlate. This does not mean labor costs can be a cost driver for material costs.

Advantages of Cost Drivers

A properly defined cost driver can be of great use for managers. The precondition is the establishment of the cause and effect relationship between cost drivers and their respective activity or cost center. Suppose a manager knows with reasonable accuracy that what is driving its costs; he may focus on reducing the quantity of that cost driver. In our previous example, the manager can work on techniques to improve labor efficiency. That would enable him a direct saving in the total cost of labor.

Suppose driver for labor cost is wrongly defined as material cost. To reduce the high cost of labor, the manager would focus on reducing the material cost where there is no cause and effect relationship. Even after successfully reducing material costs, he would find no impact on labor costs. On the other hand, if the labor cost driver is ‘product design’, which seems logical. Complex product design may require higher manual labor while a simple design, a machine can also operate. As a result, the efforts to simplify the design would show him a reduction in labor costs.

Value Driver and Cost Drivers

Many people confuse between the two terms that look similar – Value Driver and Cost Driver. A value driver is entirely a different concept and has no direct connection between the two. Value drivers are those additions to a product that increases the product’s value for its customers. Additions could be anything from an additional part to an additional feature or a free service.

Good content.. if a question is like this

Question 2

If cost is to be managed effectively, attention has to be paid to key cost drivers. Explain this statement in the context of the cost drivers in question. (20 marks)

How do you tacle it?