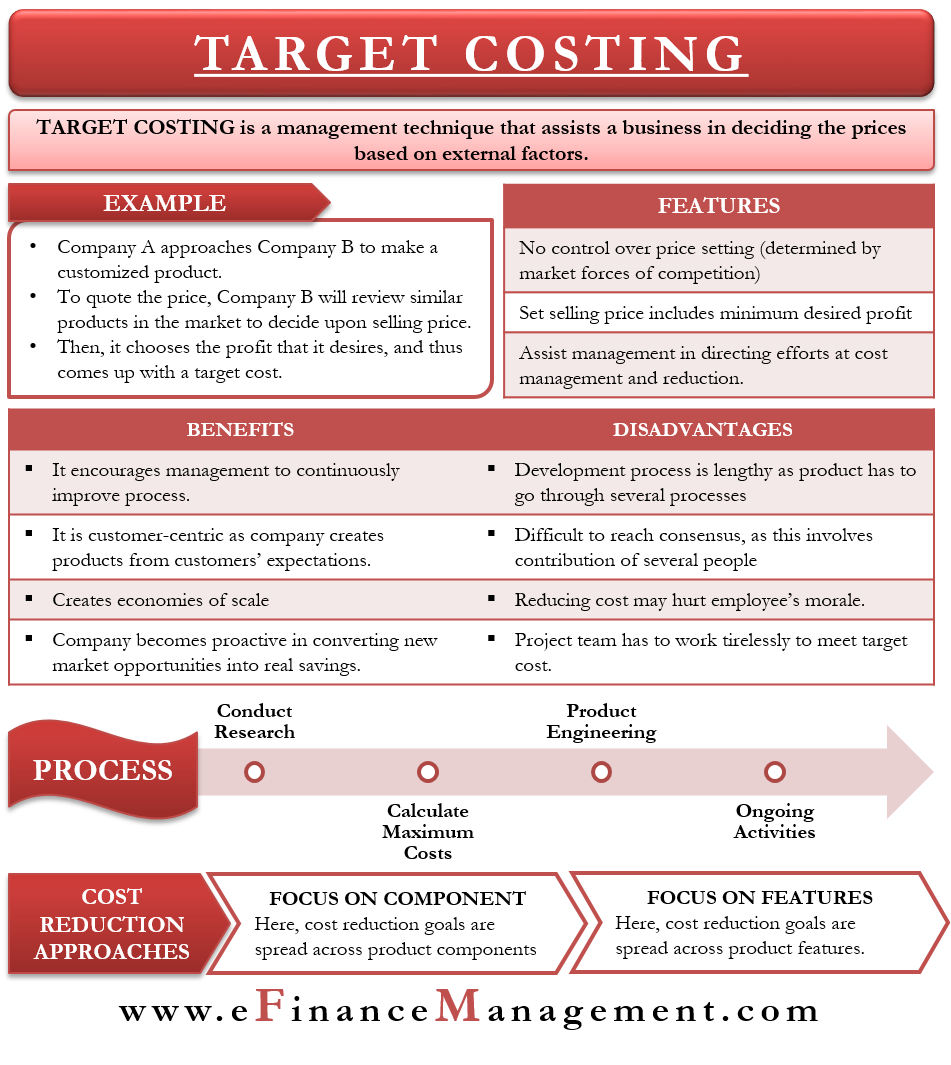

Target Costing is a management technique that assists a business in deciding the prices based on external factors. These factors include competition, the presence of switching costs for the customer, similar products, and more. The presence of such factors leaves management with little or no control over the selling price.

Thus, management has to control its costs to boost its profit margin. So, we can say that target costing includes cost planning at the product designing stage and continues throughout the lifecycle of a product (research, engineering, production, and marketing).

In simple words, the target costing is estimating the cost of a product by subtracting a profit margin that the company wants from the competitive market price of the product. Or, target costing determines the cost that is necessary to produce a product of a specific quality to ensure or attain a particular profit margin.

For example, Company A approaches Company B to make a customized product. Company B has the specifications and needs to quote a price to Company A. Company B will review similar products in the market to decide how much should be the selling price. Then, it chooses the profit that it desires and thus comes up with a target cost.

As this approach takes into account competition, it is customer-focused and is a crucial part of new product development.

Target Costing – Importance

In several industries, there is so much competition that the supply and demand factors dictate the selling prices. Producers in such industries have little or no control over the selling price. Hence, their only option is to reduce their cost to maintain their profit margin. It is where target costing comes into play. It allows the management to proactively use cost planning, cost management, and cost reduction measures. Such measures assist the management in planning and calculating the product life cycle cost early, i.e., at the time of product design and development, rather than at later stages, i.e., product development and production.

Features

Following are the key features of target costing:

- The company has no control over the price-setting; instead, the market conditions determine it.

- The selling price includes the minimum profit margin that the company desires. Also, the price consists of customer expectations, specifications, and product design.

- Assist the management in directing efforts at cost management and reduction. The gap between the target cost and the current cost is the universe for cost reduction. Here the management has to direct their efforts to bring the actual cost as close as possible to the target cost.

- The primary focus of management is to reduce costs throughout the life cycle of the product.

Benefits

Following are the benefits of target costing:

- It encourages the management to continually improve processes and innovate to gain a competitive cost advantage.

- This cost approach is more customer-centric as the company creates the products from the customers’ expectations. This expectation could be from a price or feature perspective or both. Thus, the value of the product is more to the customers.

- Such an approach helps in creating economies of scale.

- The company automatically becomes proactive in converting new market opportunities into real savings. It assists the company in delivering the best value for money to the stakeholders.

Drawbacks

Following are the drawbacks of target costing:

- Often the development process is very lengthy because the product has to go through several alterations to meet the target cost.

- Reducing costs may sometime hurt employees’ morale.

- Since the approach involves the contribution of several people, it often gets difficult to reach a consensus.

- The project team has to work tirelessly to meet the target cost.

- Sometimes the team may decide to go forward with an inferior product to meet the target costing.

Process

Following is the process to effectively implement target costing:

Conduct Research

A company must review the market in which it plans to sell the product. The review should focus on the features that customers want in a product and how much they are willing to pay for those features. Also, the company must try to determine the importance of those features in the eyes of the customers. It will help the company to decide whether or not it could drop that feature to meet the target cost.

Calculate Maximum Cost

Now that the company is aware of the features, it comes up with an estimate of the selling price for the product based on market factors. The management informs the product team about the profit margin they want. The product team subtracts the profit margin from the price to get the target cost. Management will only give a green signal to the product if the product can achieve this level of cost.

Engineering the Product

The engineers and procurement personnel now take over the project, and their responsibility is to create the product within the targetted cost. The procurement manager negotiates with the suppliers to get the best terms that align with the quality and the target cost. Further, the engineering teams ensure that the product meets the requirements and the standards set, as well as the target cost.

Also Read: Product Costing

Ongoing Activities

Once the procurement and engineering team finalize the suppliers and design of the product, the company forms a new group. This team will continuously make efforts to reduce the cost through the life cycle of the product. For instance, the team may find better suppliers or some innovation to reduce costs. It allows the company to increase its profit margin.

Approaches to Cost Reduction

There are mainly two approaches to cost reduction available to the design team:

Focus on Components

Companies use such an approach when they are refreshing or redesigning an existing product. Under this approach, the team spreads the cost reduction goal among different product components. It results in incremental cost reductions on the same ingredients which the existing product uses. A point to note is that the cost savings under this approach are comparatively lower.

Focus on Features

Under this approach, the team spreads the cost reduction goal among the product features. The team may eliminate the function if the customer doesn’t need it any longer. Such an approach results in more significant cost savings but is more time-consuming as well. This approach is most suitable if a company is looking for completely redesign an existing product.

What if Company Fails to Meet Target Cost?

In a rare case, if a team is unable to meet the target cost, then the correct thing to do will be to stop the project. The team must not go ahead with the project if it fails to get the desired profit margin.

Generally, it may take months or a year to design a product. It does not mean that the management terminates the project after the final design. Instead, to save time and costs, the company must set milestones. Then, the company must assign a certain percentage of the cost to each milestone.

Once a milestone is complete or nearing completion, the company determines if it is meeting the set target cost. If not, then it would be logical to re-work or to terminate the project at that very point and focus efforts on another project.

Terminating the project does not mean scrapping the project permanently. Instead, the management, from time to time, must review the old plans to check if there is a change in some factors that could make the projects viable again.

Final Words

Target costing is a handy approach to improving the profitability of a product. However, it is not suitable for all companies, especially the ones that offer legacy products that do not require frequent updates. Also, the profitability for such companies depends more on market penetration, like soft drinks. Also, this approach is not suitable for services or for products where labor cost is the primary cost. On the other hand, this system is beneficial for companies that regularly upgrade products, such as consumer goods.