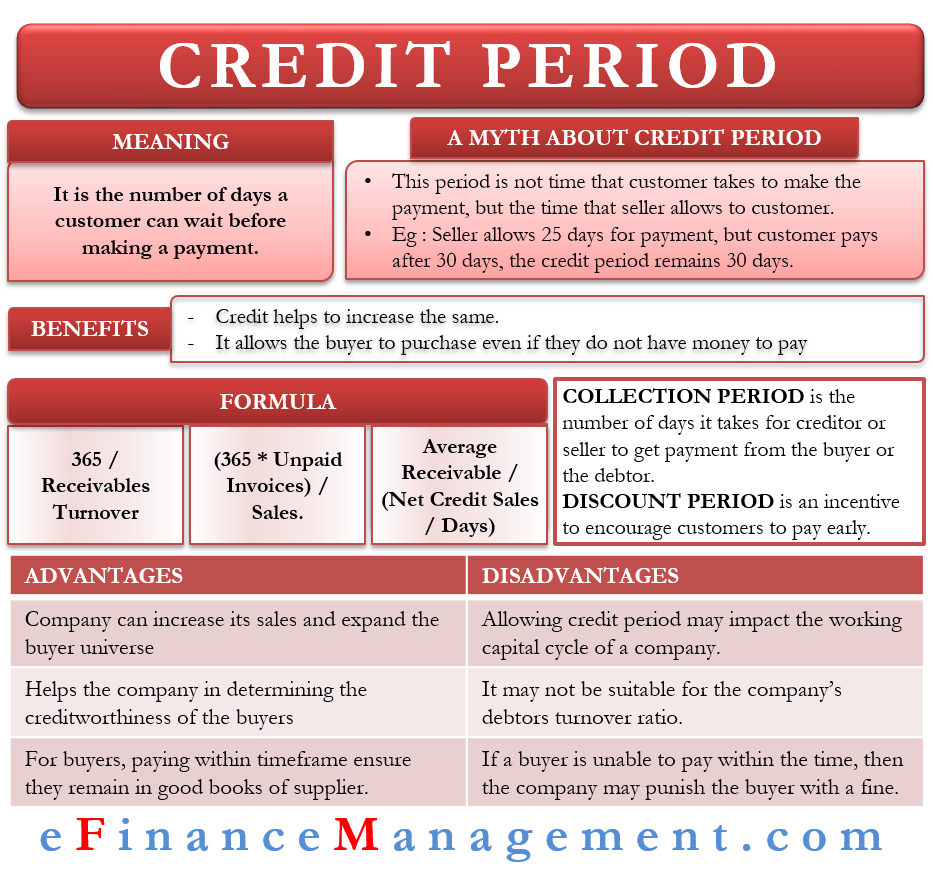

The credit period is the timeframe when a person purchases goods or services and when they pay for them. Or, we can say it is the number of days a customer can wait before making a payment. Or it is the length of time a company grants credit to its customers.

Note that this period is not the time that a customer takes to make the payment. Instead, it is the timeframe or period that the seller grants the buyer to pay for the invoice. For example, if a seller allows the buyer to make a payment after 25 days. But the buyer pays after 30 days. The credit period there will be 25 days.

More About Credit Period

As said above, allowing customers to buy goods on credit helps to increase sales. It is so because credit allows the buyer to purchase the products or services even if they don’t have the money to pay for them.

However, a company must set clear credit terms before making the sale. A standard across the industries is 1/6 N/30 or 1/6 net 30. It means that if a customer pays back within six days, then they get a 1% cash discount.

Also Read: Operating and Cash Operating Cycle

If a customer is unable to take a discount, then they must make the payment within 30 days from the purchase date. This 30-day period is the credit period.

Also, the seller may have a credit policy where they allow multiple payments over time. Here, the credit period is the timeframe from the date of purchase to the time when the buyer is to make the last payment. For example, a company has a policy to allow buyers to make payments in three monthly installments, where the final installment is due in 50 days. The credit period in such a case is 50 days.

Formula

The formula to calculate the credit period is – 365 / Receivables Turnover

The numerator is the number of days in a period, which is usually a year or 365 days. The denominator is the receivables turnover for the same period. Receivables turnover is the ratio of total sales to the number of unpaid invoices or sales / unpaid invoices.

We can also write the formula as (365 * Unpaid Invoices) / Sales.

To calculate the credit period using this formula, we must know the number of unpaid invoices, the amount involved in those invoices, and the total sales.

Let us understand the calculation with the help of an example. Assume Company ABC has sales of $300,000 and unpaid invoices of $24,700 for the full year. Now, putting the values in the formula, we get a receivables turnover of 12.1457 ($300,000/$24,700). The credit period is 30.05 days or 30 days approx (365/12.1457).

There is one more formula, and it is – Average Accounts Receivable / (Net Credit Sales / Days)

Here, Average Accounts Receivable is the sum of the opening and closing balance of accounts receivable and divide it by 2.

As the name suggests, Net Credit Sales are the total credit sales of a company.

Days is the number of days in the period under consideration. For instance, if we are considering a year, then the number of days would be 365 days.

Let’s understand the calculation with the help of an example. Company ABC has net credit sales of $240,0000 for the year 2019. The opening and closing balances of the accounts receivable are $800,000 and $880,000, respectively.

Average Accounts Receivable will be $840,000 (($800,000 + $880,000) / 2). The number of days would be 365 as we are considering the full year.

Putting the values in the formula, we get a credit period of 127.75 or 128 days ($840,000 / ($240,0000 / 365))

Advantages

The following are the advantages:

- By extending the credit period to the buyers for their purchases, the company can increase its sales and expand the buyer universe, which will help it achieve its sales targets.

- Credit Period helps the company determine the buyers’ creditworthiness and apply filtering for future business.

- For the buyers, paying within the timeframe ensure they remain in the good books of the supplier.

Disadvantages

The following are the disadvantages:

- Allowing too much time to make the payment could impact the working capital cycle of a company. If a company is unable to collect the dues in time, it may face issues in meeting its working capital needs.

- Giving too much time or an extended credit period may not be suitable for the company’s debtors turnover ratio.

- If a buyer is unable to pay within the time, then the company may punish the buyer with a fine. The company may lose this buyer if they do not agree with the company’s credit policies.

Collection Period and Discount Period

A collection period is also a similar concept. We may call it a by-product of the credit period. It is the number of days it takes for the creditor or seller to get a payment from the buyer or the debtor. Depending on when a customer makes the payment, a collection period could be less or more than the credit period. If a company has cash-on-delivery terms, then both credit and collection periods are zero.

The discount period is an incentive to encourage customers to pay early. Under this, a company gives customers a specific discount if they make the payment within a few days after the purchase. Such business terms allow a company to recover the payment from the debtors quickly.

For example, a company with a credit policy of 30 days also plans to give a 2% discount if a customer makes payment within ten days of making the purchase. In business terms, such a policy is expressed as 2/14, net 30.

Final Words

A credit period is significant for a business in two ways. First, allowing customers to pay later helps increase the sales of a company. Second, it helps to maintain the working capital cycle of a company. So, in the absence of any credit period, a company may get complacent in collecting dues from the debtors leading to a working capital crisis.

Also, a company must regularly evaluate its credit period. It must not solely depend on the formula for the credit period. Instead, it should also compare it with others in the same industry. Only after comparing it with others, a company should decide on the credit period.

RELATED POSTS

- Trade Credit

- Payable Deferral Period – Meaning, Formula, Importance, and More

- Invoice or Bill Discounting or Purchasing Bills

- Advantages and Disadvantages of Invoice Discounting

- How to Analyze and Improve Debtors Turnover Ratio / Collection Period?

- Allowance for Doubtful Accounts – Meaning, Accounting, Methods And More