What is Working Capital Cycle (WCC)?

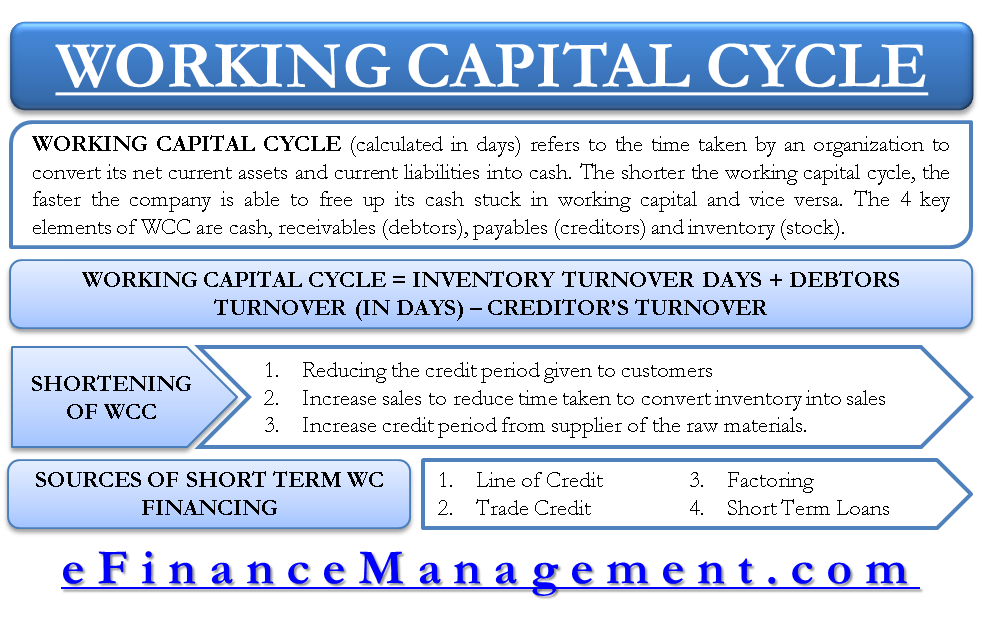

Working Capital Cycle (WCC) refers to the time taken by an organization to convert its net current assets and current liabilities into cash. It reflects the ability and efficiency of the organization to manage its short-term liquidity position. In other words, the working capital cycle (calculated in days) is the time duration between buying goods to manufacturing products and the generation of cash revenue on selling the products. The shorter the working capital cycle, the faster the company can free up its cash stuck in working capital. Too long working capital cycle blocks the capital in the operational cycle. This capital does not even fetch any return. Therefore, a business tries to shorten the working capital cycles to improve the short-term liquidity condition. And increase its business efficiency.

The WCC focuses on the management of 4 key elements, viz. cash, receivables (debtors), payables (creditors), and inventory (stock). A business needs to have complete control over these four items to have a fairly controlled and efficient working capital cycle. Let us look at an example to better understand the concept of the working capital cycle.

Working Capital Cycle Example

Let us assume the following details for a company that is in the manufacturing sector.

- A company takes raw materials on credit and has to pay back to its creditors in a few days (say 30 days in our example). We also call these 30 days the average payables period (AP Period). The calculation of the AP Period is as follows:

Average payable period = average creditors / credit purchases X 365.

This means that the company enjoys a credit period of 30 days on the purchase of raw materials used to produce the final good.

- The company takes “x” number of days to sell off its inventory; the “x” here is nothing but an inventory turnover ratio converted into a number of days instead of the number of times. Assuming an average inventory of $ 5000 and average sales of $ 18000. The inventory turnover ratio amounts to $ 5000 / $ 18000 X 365 = 102 days approximately.

- It takes some time for the company to convert its credit sales into cash due to the credit management policy incorporated by the company in terms of the credit period extended to customers. Assuming outstanding debtors of $ 9000. And a total credit sale amounting to $ 60,000, the average collection period can be calculated as

Average collection period = average debtors/ Total Credit Sales X 365

= $ 9000 / $ 60000 X 365

= 55 days, approximately

Based on the above information, we infer that

- The company has to pay back its creditors within 30 days.

- For inventory to convert to sales, it takes roughly 102 days

- Conversion of receivables (debtors) to cash, on an average, takes 55 days

Working Capital Cycle Calculation

The calculation for the WCC of a company is as follows:

Working Capital Cycle = Inventory turnover in days + debtors turnover in days– creditors turnover

= 102 + 55 -30

= 127 days

This implies that the company has its cash locked in for a period of 127 days. And would need funding from some source to let the operations continue as creditors need to be paid off in 30 days. Assuming the company had to make all cash payments for its raw material requirement, there wouldn’t be any creditors. And then the working capital cycle would be 102 + 55 = 157 days.

Every company would like to keep its cash conversion cycle as short as possible. The finance executives need to focus on individual aspects of the WCC to achieve this. Let us see how this works:

Also Read: Objectives of Working Capital Management

How to Shorten Working Capital Cycle?

A company can aim to shorten its WCC by:

- Reducing the credit period given to its customers reduces the average collection period. Offering cash discounts can also help improve the debtor’s turnover ratio or average collection period amid various other ways.

- The company can try to improve/streamline its manufacturing process and focus on various ways to increase sales to reduce the time taken for inventory to convert to sales. The earlier the stock clearance, the better the working capital cycle.

- A better negotiation to increase the credit period from suppliers of raw materials and goods required for production can also reduce the working capital cycle.

While the average collection period and credit period from suppliers aid in shortening the WCC, the initial prime focus of the business should be to reduce the time taken for inventory to convert to sales. If the time taken is very long, it could imply that the business cannot generate sales for the goods produced, and more and more capital gets locked in inventory. Either the business should try and reduce the time or should reduce the amount of inventory. Thereby reducing the amount locked in working capital. In other words, if the business cannot reduce its WCC and has higher inventory levels, it should aim to reduce inventory levels and reduce the amount locked in the working capital keeping the cycle time length the same.

With accounts payable financing alone, most businesses cannot finance the operating cycle (average collection period + inventory turnover in days). The business can manage this shortfall either out of profits accumulated over time, borrowed funds, or by both. Let us look at the sources of funding used to manage the gaps in a working capital cycle.

Sources of Short-Term Working Capital Financing

Lines of Credit

The company can borrow from banks for a short-term (usually 30 – 60 days) against a line of credit given by the bank. With cash inflow from the sales proceeds, the company can pay this off.

Trade Credit

Often good relations with creditors can be used for extending the credit period as one of the cases in case of a large order and enable financing at a lower cost.

Factoring

Factoring or discounting receivables can shorten the working capital cycle and generate cash. However, this is usually at a higher cost.

Short Term Loans

Companies that may not be able to get a line of credit may look for a short-term working capital loan from a bank.

Having brief knowledge of the sources of working capital financing, let us understand the nature of the working capital cycle:

The nature or the length of the working capital cycle differs from business to business and varies among sectors. As seen above in the example, the WCC in a manufacturing company is usually positive. As there is a time lag between the goods produced and goods sold (time is taken for inventory to convert to sales). However, there is a possibility of a negative working capital cycle in specific businesses.

Negative Working Capital Cycle

Let us look at the business model of a supermarket or hypermarket chain. The customers who come to purchase pay by cash, and hence there aren’t any debtors, or the collection period is 0 days. The business is a supermarket, and hence, all items in the store are taken from vendors and have a credit period availability to be paid. So usually, such businesses enjoy huge cash and even may make interest earning on the cash till they make payment to the suppliers. Therefore, these companies have a negative working capital cycle.

Conclusion

Given that the working capital cycle can range from negative to large positive. One needs to answer the question as to what is the optimum level of the working capital cycle. One cannot arrive at thumb rules as the working capital cycle varies from sector to sector.

Comparison with peers in a similar industry is more meaningful when analyzing companies and their operating efficiency. Moreover, the working capital cycle may fluctuate depending upon its product manufacturing, seasonality, and shelf life, among other factors. Sometimes poor forecasting, change in government policies, and unexpected events may change the working capital cycles and add up to working capital financing problems.

Usually, companies use a ratio of working capital to sales to see if the business is moving in line with the industry performance/benchmark. The level may also depend on future plans, sales forecasts, product diversification, etc.

Very informative article. Keep them coming.

very good. very informative.

I also think that factoring is definitely one of the great and way to finance a business. I think that we can definitely get instant cash with the help of factoring. Thanks for sharing this article.

Thank you I have learned

Hi, can you please explain what is the working capital cycle of a manpower supply business.

Thanks