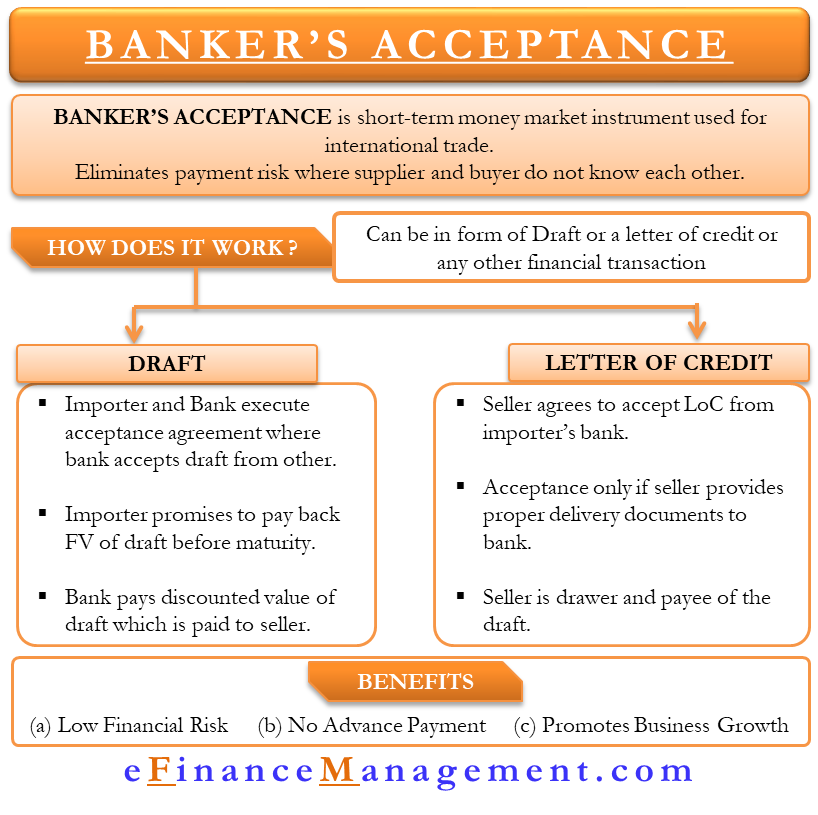

Bankers Acceptance (BA) is a short-term money market instrument that comes in handy in international trade. It helps to eliminate the payment risk in the case; the supplier and buyer do not know each other and belong to different countries.

Basically, it is a time draft that a business can get from the bank as an extra cover against counterparty risk. Here bank promises to pay the exporting firm a definite amount on a specific date after it recovers its money by debiting the importer’s account. In simple words, you can understand BA as a post-dated check from a bank.

Bankers Acceptance History

Bankers acceptance is not a new concept and dates back to the 12th century. During the 18th and 19th century, Sterling bankers acceptance were very active in London. In 1913, the United States Federal Reserve was formed, and one of its objectives was to encourage domestic bankers acceptance market to take on London’s market.

Fed aimed to boost United States trades and make the US banks more competitive. At the time, National banks were given the authority to accept time drafts, while the Fed had the authority to take over some eligible bankers acceptances.

Also Read: Time Draft

The eligibility criteria included bankers acceptance of finance self-liquidating transactions with a maturity under six months. Fed, however, no more buys BA. Still, the eligibility requirement holds significance as there are no reserve requirements if a bank sells an eligible acceptance.

How BA Works?

Bankers acceptance could be in the form of drafts, letters of credit, or any other financial transactions. Thus, it works in various ways.

For instance, an importing company looks to buy goods from an exporter and approaches the bank because the seller is not granting credit. The importer and the bank execute an acceptance agreement, under which the bank will accept a draft from the importer or buyer, who promises to pay back the face value of all the drafts before their maturity to the bank.

Importer, thus, draws a time draft, listing itself as the payee, and the bank accepts the draft, thereby paying the importer the discounted value of the draft. The buyer then uses the funds to pay the seller.

Another way BA works is the seller agreeing to accept a letter of credit (LoC) from the importer’s bank. The LoC will specify that the bank would accept time drafts from the seller only if they (seller) provide proper delivery documentation. In this case, the seller is the drawer and payee of the draft.

Also Read: Trade Acceptance

It must be noted that the importer’s bank usually transacts with the seller’s bank and not with the seller directly. The seller may realize the money from BA in a few ways, such as discounting it, selling it, or holding it until maturity.

Obtaining a Bankers Acceptance

A business that wants to get BA should approach a bank with which they maintain a good credit rating and relationship. You should be able to offer collateral (or prove you can do so) against the ability to repay the bank at a future date. However, not every bank gives the facility of bankers acceptance. The business has to go through credit checks and maybe an underwriting process as well. The bank charges a percentage of the total acceptance amount as fees.

Benefits of Bankers Acceptance

Low Financial Risk

Sellers will be more interested in dealing with buyers who are backed by a known and reputed bank. A buyer with BA is usually less risky than the one without it. Also, the interest rates on BA are low when compared to the benefits that a buyer can garner from it.

No Advance Payment

Since the buyer has a good relationship with the bank, they do not have to worry about making advance payments. And as both buyer and seller do business, they build trust, and over time, they don’t need any BA. Thus, we can say, BA helps to build trust between the parties.

Promotes Business Growth

A new buyer with BA will always attract more sellers than the buyer who does not have any guarantee from the bank.

Talking of disadvantages, it has one major one. Not all banks deal in BA, and even the ones that do will evaluate you fully before agreeing to anything. In some cases, banks may even ask you to give collateral as well.

BA as Investment Option

It is important to understand that bankers acceptance is deemed as an obligation on the accepting bank. Thus, a payee can sell the bankers acceptance depending. Selling BA means selling the time draft, but it will sell at a discount. The discount will depend on the time period left for the maturity and reputation of the bank.

Because of this, BA is tradable in the money market and is an effective short-term instrument. There is a big and liquid secondary market for such instruments. These instruments are usually sold at prices slightly less than London Interbank Offer Rate (LIBOR) in the secondary market.

A point to note is that BA does not trade on an exchange. These money market instruments trade through large banks and securities dealers. Therefore, there is no formal bid and ask prices; instead, investors negotiate the prices. As said above, the negotiations majorly depend on the size and goodwill of the paying back. For instance, a BA from a bank with a strong credit rating usually sells for a lower yield since the chances of default are less.

What if Bank Fails?

Bankers Acceptance is a safe and secure money market instrument, and banks are primarily responsible for making the payment. However, if a bank somehow fails to honor a BA, what happens to the investor or seller?

A point to note is that other related parties are also responsible to the investor along with the bank. So, if a bank fails, the onus lies on the importer to make the payment. Truly speaking, any party that has purchased or sold the BA has an obligation.

Final Words

Bankers Acceptance is not only a useful tool for international trade; it is also a good investment option. Investors can add it to their portfolio to compensate for the high-risk securities, while businesses can use this to eliminate risk.