S Corporation- Definition

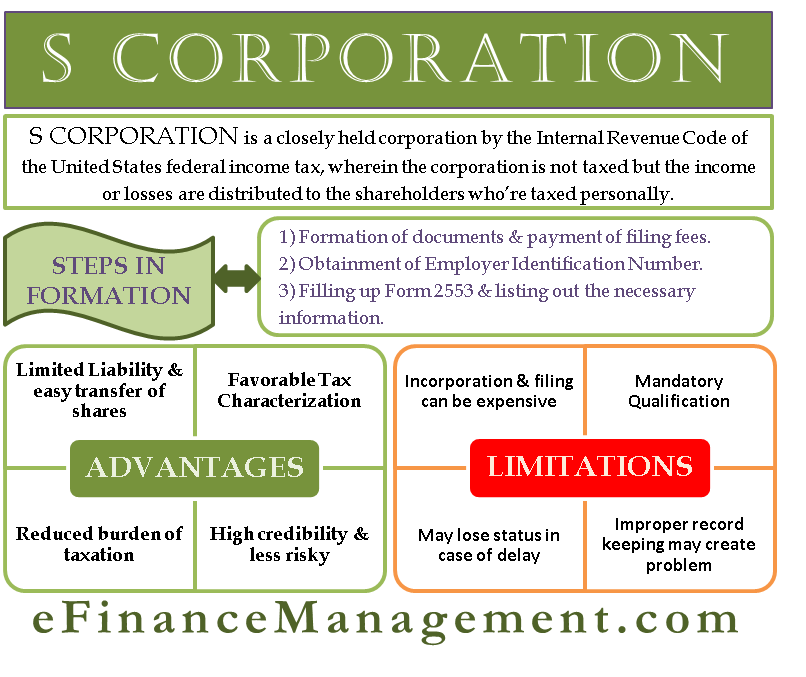

S Corporation is a closely held corporation by the Internal Revenue Code of the United States federal income tax, wherein the corporation is not taxed, but the income or losses are distributed to the shareholders. The individuals then report this income or losses in their personal returns and pay taxes individually. They are taxed at their personal income tax rates.

Features / Characteristics of S Corporation

- Limited liability of the members. This means one cannot use the shareholders’ personal assets to discharge the corporation’s liability.

- The corporation need not pay federal taxes at the corporate level. The income or losses are disbursed to the shareholders who will pay their personal income tax returns. Hence, the business losses can be set off against the income of any other shareholder. This might be really helpful for taxation purposes.

- Avoidance of double taxation.

- S Corp has perpetual existence. It doesn’t affect by any owner’s death or dismissal.

How to Incorporate?

Step 1: Formation

Filing the appropriate formation documents and paying the filing fees with the state.

Step 2: Obtainment of EIN

Need to obtain EIN (Employer Identification Number) by filing Form SS-4 with IRS (Internal Revenue Service). One can apply online, by mail, or through phone (for international applicants).

Step 3: Filing of Form 2553

Filing of Form 2553 with the IRS and listing out the following information:

- Company Name and Address,

- EIN Number,

- State and Date of incorporation,

- Shareholders’ or members’ information,

- The effective date of the election,

- Fiscal Tax year information.

Once one complies with the above-mentioned formalities, it will take approximately 60 days to receive an acceptance letter from IRS. After the receipt of the acceptance letter, one can officially operate as an S Corporation.

Qualification for S Corporation

- Has to be a Domestic Corporation.

- Not more than 100 shareholders.

- Shareholders allowed are individuals, certain estates, and trusts. Not allowed shareholders are non-resident aliens, partnerships, and corporations.

- Only one class of stock.

- Ineligible Corporations are not allowed.

- Shareholders need to of U.S citizens or residents only. Also, they need to be natural persons only.

Management Structure Of S Corporation

S Corporation, incorporated with only one shareholder, does not require any other designated head to hold the position in management. He can be the director, CEO, and president and can hold other titles. But, in the case where there is more than one shareholder, it is required to appoint management heads like directors, CEO, and CFO. The shareholders appoint the Board of Directors. Furthermore, the Board of Directors appoints corporate officers like the CEO, CFO, COO, etc.

Also Read: C Corporation

Accounting of S Corporation

Although there are some differences between S Corporation and C Corporation, both have similar accounting. But, due to the difference in the tax treatment of both types, there could also be a little difference in their accounting. Accounting needs to be accurate as it is required for analyzing performance and other factors. Basic accounting requires maintaining different ledgers, income statements, and balance sheets.

Advantages of S Corporation

- There is limited liability of the managers and the shareholders unless otherwise stated to any. Their assets remain protected. Creditors cannot claim on the shareholder’s house, property, or bank accounts for their payments.

- Favorable tax characterization.

- The shareholders can draw a salary as employees. They can also receive dividends and distributions tax-free to some extent in their investments. The owner-operator relationship will reduce the burden of tax liability. This helps incur more business expenditures like wages payment which can be a business expenditure allowable as a deduction.

- One can transfer the easily by the sale of stock. The corporation need not make any entries or comply with any accounting regulations for transferring the ownership.

- Since the individuals are taxed on their personal tax returns, their tax rates might be lower than that of corporates.

- Shareholders are not subject to self-employment taxes.

- This business structure gets more credibility than a sole proprietorship or a general partnership.

- Generally, there is less risk of audit.

Disadvantages of S Corporation

- Payment of incorporation fees can be a slight expensive.

- It has to be a U.S. corporation only. Hence, this is a major con.

- One has to qualify as per the requirements. Such requirements are not there in C Corporation.

- Comparatively more difficult to set up, in case of filings, record keeping, board meetings, etc.

- S Corporation may lose its status if there is no proper recordation and filing of the same in time.

Frequently Asked Questions (FAQs)

A maximum of 100 shareholders are allowed in an S Corporation.

S Corporation can be in the form of an LLC, general partnership, or corporation.

The incomes of S Corporation are taxed in the hands of shareholders in the form of dividends. There is no tax on the incomes and losses of S Corporation.

Both S Corporation and C Corporation shareholders’ have limited liability.

Very simple and well explained information.

Thank you for you help!