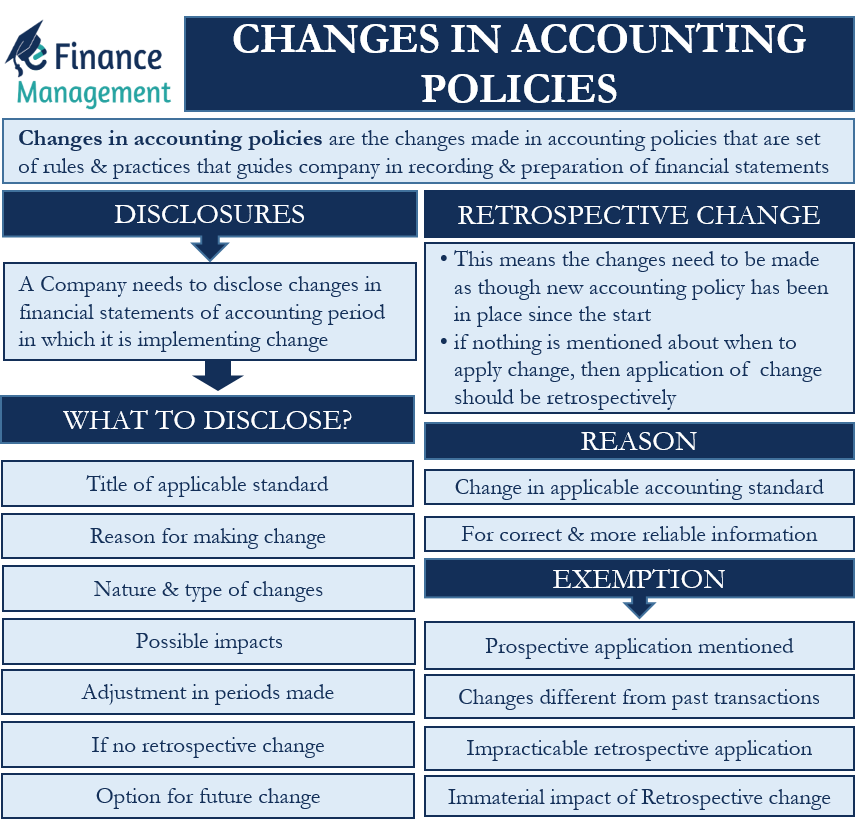

Changes in Accounting Policies

Every organization needs to follow the accounting rules and frame its own accounting policies. These policies are nothing but a well-thought-out set of rules and practices that guides the company in recording and preparation of its financial statements. And of course, all these policies must be framed keeping in mind the requirements of the accounting standard prescribed by IFRS or GAAP. An important accounting principle is the consistency of practices. Hence, generally, a company should not make changes to its accounting policies. But sometimes under some circumstances, it becomes the need and requirement to make a change. Like when there is a change in the applicable accounting framework.

Accounting policies mainly guide companies when dealing with complex items. These complex items are depreciation, goodwill, inventory valuation, R&D expenses, and more. The primary objective of accounting policies is to give out an accurate position of a company’s financial performance. So, if making changes in accounting policies would lead to more reliable and relevant information, then a company must make changes to its accounting policies. However, the company must make a disclosure leading to circumstances prompting for the change and justification thereof.

Reasons for Changes in Accounting Policies

Following are the reasons when an entity needs to make changes to its accounting policies:

- When the need for a change is due to a change in the applicable accounting standard.

- When the changes become important for preparing correct statements and giving out more reliable and relevant information.

What is Retrospective Change?

In case the applicable accounting standard requires an entity to change its accounting policy from the new period, then the change needs to be made under the transitional requirements, or from that point in time. However, if it mentioned nothing about when to apply the change, then the company needs to apply the change retrospectively.

This means the changes need to be made as though the new accounting policy has been in place since the start. So, the change needs to be made to every affected account and for all periods. Of course, re-writing the whole past set of accounting records is a daunting task. Besides, it consumes a lot of time and effort. Sometimes there are scenarios when it is not possible to make changes retrospectively.

In such a case, the company must make relevant changes to the affected accounts starting from the earliest period that the new policy can be applied. And, in case a company can not determine the policy change impact for any period, then it needs to make the change at an earlier date whenever it is possible for it to apply the new changes.

Whenever a company carries out such policy changes, it must also make necessary adjustments to all related notes accompanying the financial statements.

Disclosures of Changes in Accounting Policies

When there is a change in policies, a company needs to disclose it in the financial statements of the accounting period in which it is implementing the change. A company needs to make the following disclosures when it makes changes to its accounting policies:

- Title of the applicable IFRS or GAAP standard.

- The reason for making the change.

- The nature and type of changes it is making to the policies.

- All possible impacts of the new changes.

- Adjustments in the current and earlier period due to the change.

- If the retrospective adjustments were not possible, then reasons for not making such changes.

- Detailing provisions of all necessary options for the changes in the future.

Exemption from Retrospective Application

Under the following scenarios, an entity may get an exemption from the accounting standard for the retrospective application of a change in accounting policies.

- If the transitional provisions mention about the prospective application of the changes in the accounting policy. In such a case, an entity must follow the transitional guidance of the applicable standard.

- If the changes to the accounting policy are related to transactions that are significantly different from the past transactions.

- When the retrospective application impact is immaterial, then also an entity may get an exemption.

- Also, if the retrospective application is not possible or impracticable, then an entity may get an exemption. For instance, if a company does not have sufficient data to determine the impact of the change, then it would be unfeasible or impractical to go for the retrospective application.

How it is Different from Change in Accounting Estimate?

Usually, a company needs to readjust the amount of its assets or liability. Such an adjustment helps an entity to better estimate the future benefits and obligations connected with that asset or liability. We call such an adjustment the change in accounting estimate. This change in the estimate could affect the present period of the change or both present and future periods simultaneously.

Talking about how it is different from changes in accounting policy, an entity makes changes in accounting estimates prospectively. But changes in accounting policy are usually retrospectively.

Also Read: Accounting Principles

Example

Company A bought a machine for $100,000 in January 2017. The company decides to charge depreciation on the basis of SLM (straight-line method). In January 2019, however, the company decides to switch to WDV (written down value) method retrospectively at the rate of 10%. The useful life of the machine is 10 years.

Depreciation amount for 2017 and 2018 on the basis SLM method will be $20,000 (($100,000/10)*2).

Since this is a retrospective change, we need to calculate the depreciation on the basis of the WDV method from 2017.

Depreciation for 2017 using WDV method = $10,000 ($100,000 * 10%)

WDV value = $90,000 ($100,000 less $10,000)

Depreciation for 2018 using WDV method = $9,000 ($90,000 * 10%)

WDV value = $81,000 ($90,000 less $9,000)

Total depreciation as per WDV = $10,000 plus $9,000 = $19,000

Total depreciation as per SLM= $20,000

Difference = $20,000 less $19,000 = $1,000

Adjusting entry will be:

| Date | Particulars | Dr. Amount | Cr. Amount |

|---|---|---|---|

| 2019 January | Profit and Loss A/C | $1,000 | |

| To Depreciation A/C | $1,000 | ||

| (To record adjusting entry for a change) |

Final Words

Accounting policies should be such that they do not require frequent changes. But, if it becomes mandatory to make changes, then an entity must follow all the disclosure guidelines to ensure the benefit of all the stakeholders. Moreover, the entity must make all efforts to apply the changes retrospectively.

RELATED POSTS

- Adjusting Entries – Meaning, Types, Importance And More

- Accounting Information

- Presentation of Financial Statements

- Fundamentals of Accounting: Meaning, Principles, Categories, and Statements

- All 10 GAAP Principles – Meaning, Importance And More

- Difference between Financial and Management Accounting